The job market is tough for new graduates — even if you dropped $200,000 on an elite MBA

Top MBAs are struggling to land jobs; some are trying their hand at entrepreneurship instead.

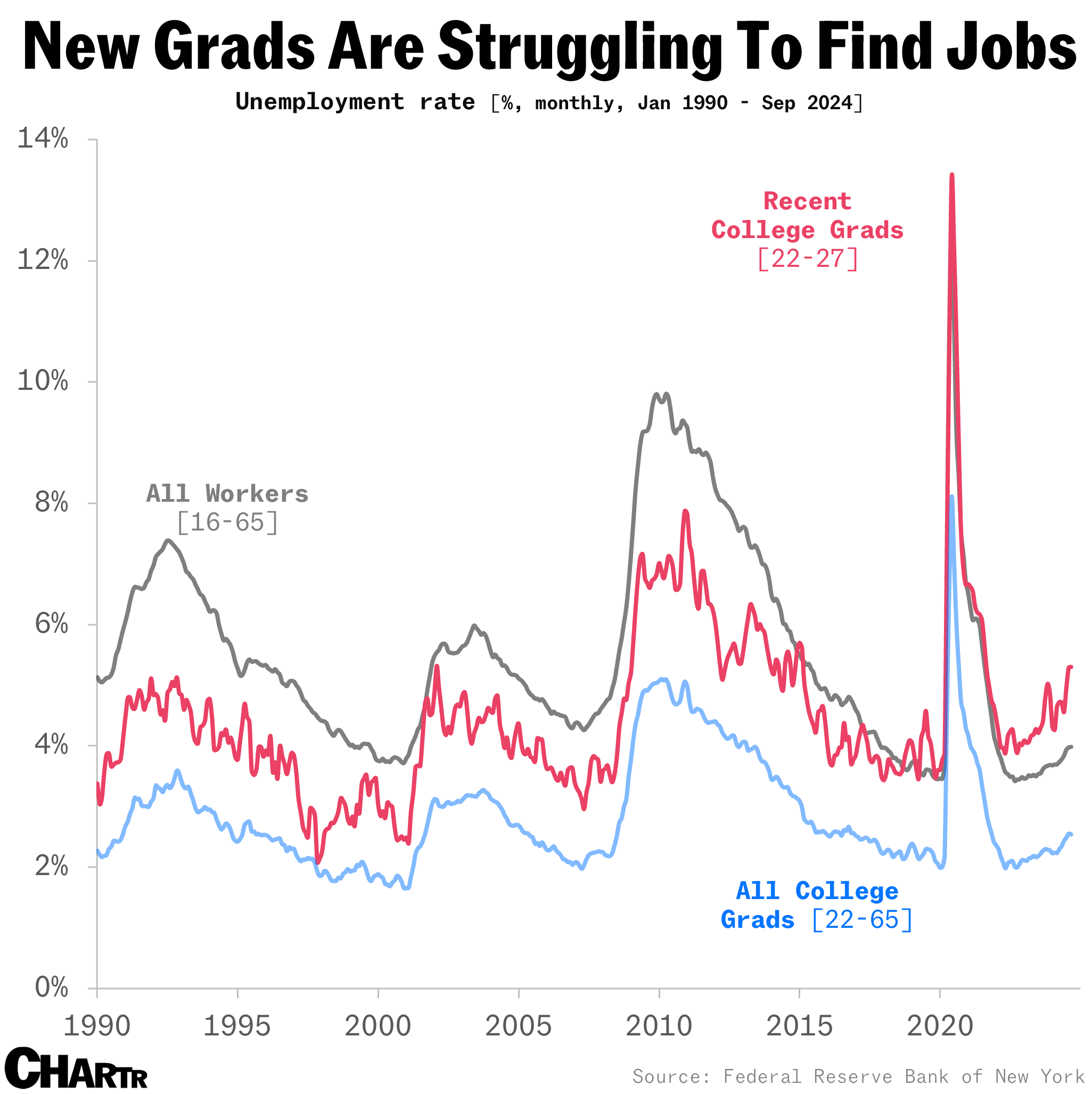

The US labor market is in decent shape: layoffs have been pretty limited, job growth has been solid, and unemployment remains near record lows. But that optimism doesn’t extend to fresh college grads, who are increasingly scrambling to break into the professional world.

According to the latest data from the New York Fed, the unemployment rate for recent college graduates (ages 22-27 with a bachelor’s degree or higher) has reached its highest level in two years. It’s also now higher than the overall workforce, breaking a multidecade trend where recent grads typically had lower unemployment rates.

Now, that strain is spilling over to those who spent over $200,000 on an elite MBA program. Once a predictable path to a lucrative job with a corner office — nearly half of Fortune 500 and S&P 500 CEOs have an MBA, mostly from top schools like Harvard or Wharton — the MBA has lost some of its shine, with even top-tier MBAs finding it hard to land jobs in 2024.

This year, 84% of job-seeking graduates from the top 15 US business schools secured jobs within three months of graduation, down from 92% in 2019, according to The Economist. Even at the so-called M7 schools — Harvard, Stanford, Columbia, UPenn Wharton, Chicago Booth, Northwestern Kellogg, and MIT Sloan — all but Columbia saw drops in job acceptance rates, per school employment reports, first reported by The Wall Street Journal.

So, what’s behind the slowdown?

Put simply, traditional powerpoint- and analysis-obsessed employers, consulting and tech, have significantly pulled back on hiring. Big Tech hires fell by over half at Chicago, Columbia, MIT Sloan, and NYU Stern last year, compared to the 2018-22 average, The Economist’s analysis found, while placements at the Big Three consultancies also dropped by a quarter.

These declines come after the tech and consulting pandemic hiring boom of 2021, a time when 91% of corporate recruiters planned to hire MBAs, up from 80% of actual hires in 2020, according to data from the Graduate Management Admission Council.

In short, they seem to have hired everyone they needed. Some employers even went the other way, with firms like Meta entering their “year of efficiency” — eliminating tens of thousands of jobs in the process.

Degrees of risk

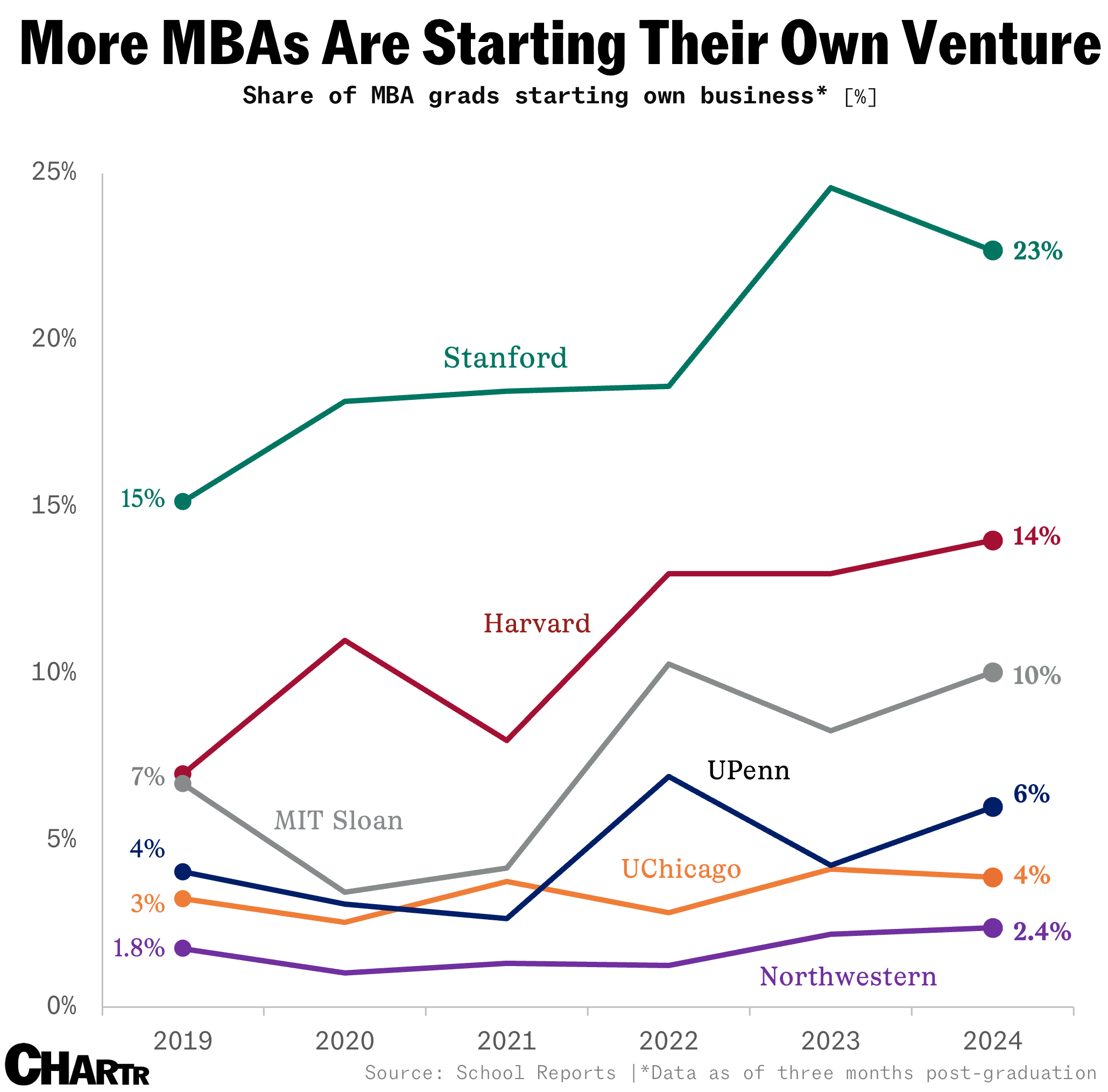

As corporate heavyweights hit the recruitment brakes, MBA grads are now turning to a previously underexplored path: entrepreneurship.

The share of students starting their own businesses has increased since 2019 at the M7 schools — except for Columbia, where data wasn’t available — with Stanford, already known for churning out ambitious young founders like Evan Spiegel (Snapchat) and Phil Knight (Nike), reaching an all-time high in 2023.

In particular, a growing number of these grads are exploring search funds, where they raise money to acquire and run already established businesses. According to Stanford’s research, a record 94 search funds were launched in 2023 in the US and Canada, up from ~60 the year before and fewer than 10 at the turn of the century.

So, what’s the appeal of a search fund for a top MBA grad?

In a world where landing a corporate gig is tougher than ever, no matter how shiny or expensive your diploma is, search funds give the opportunity to be a CEO from day 1. They also unlock the potential for big profits and offer something of a middle ground for aspiring founders — buying a company that’s already operating might scratch the entrepreneurial itch, while not requiring you come up with a new “zero-to-one” business venture.