Papa John’s is trying to slice out a niche as the value pizza option

Domino’s is crushing Papa John’s in the sales department.

Papa’s got a brand-new bag… which seems to revolve around presenting itself as the cheaper option for hungry pizza seekers.

Lower crust

In the press release that accompanied its Q4 and full-year results, Papa John’s CEO Todd Penegor, who took the helm in August last year, said he’s been pleased with the early progress the brand has made in improving its “value perception,” despite overall revenues slumping 3.6% in 2024.

The pizza chain pointed to Super Bowl Sunday, which was a key impetus for revolutionizing its dough-making methods back in 2020, as its highest sales day, while heart-shaped pies on Valentine’s Day were another highlight.

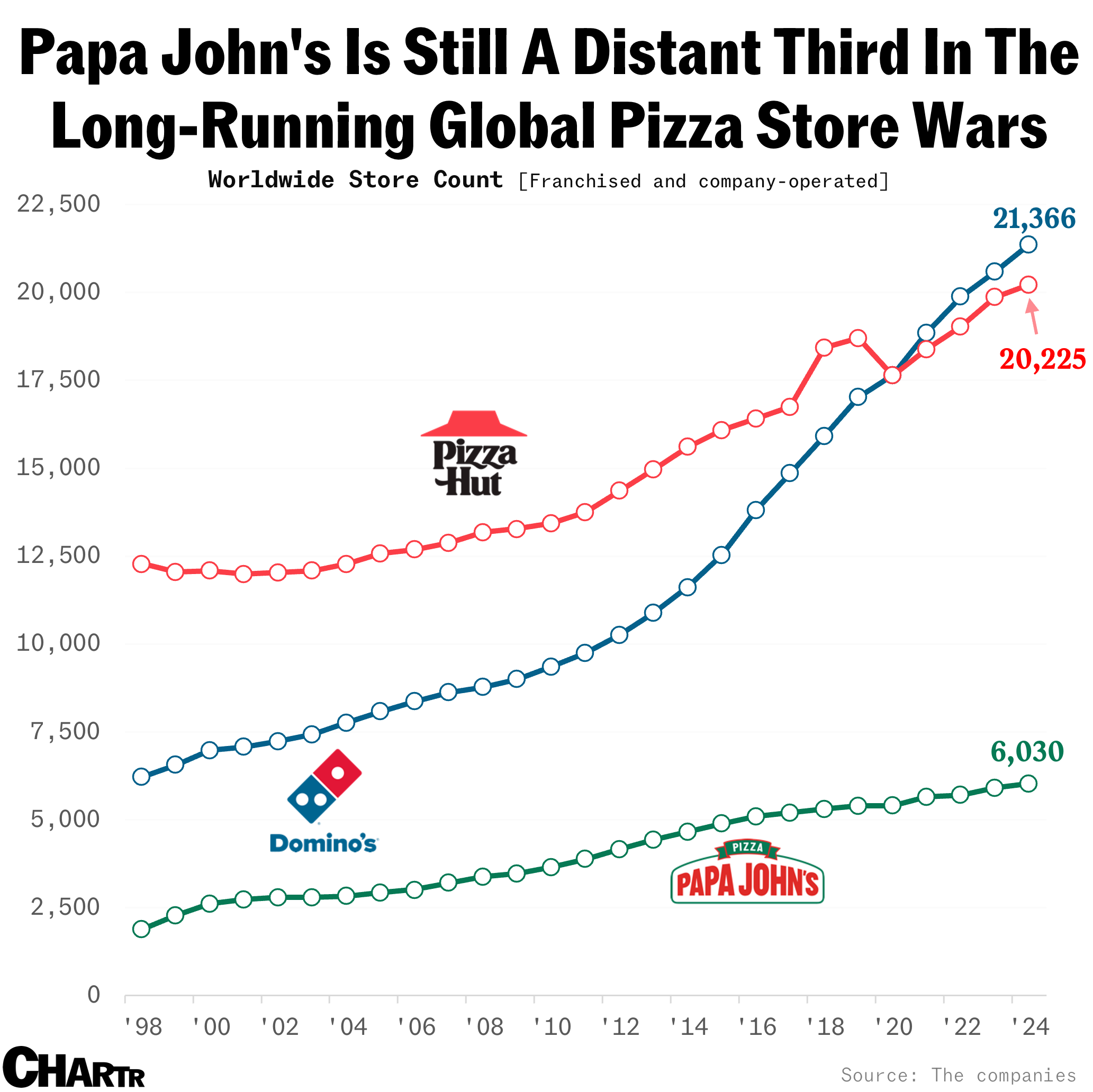

Though red letter days are a fun marketing tool, the reality is that Papa John’s is getting outpaced by its pizza rivals. Last year, Papa John’s comparable sales in North America were down 4% from 2023 — and rival Domino’s notched US same-store sales growth of 3.2% for fiscal 2024.

The company’s ~6,000 franchised and company-operated stores, nearly 60% of which were in North America, translated to $2.06 billion in sales for the 40-year-old chain.

Though same-store sales numbers at both Pizza Hut and Domino’s have softened recently, the pair are still at the top of the pizza game. Pizza Hut, one of Yum! Brands’ biggest names alongside KFC and Taco Bell, netted $13.1 billion in sales from 20,225 stores in 2024, while Domino’s made a whopping $19.1 billion from 21,366 stores as it cements its position as the only company that can out-pizza the hut.