What happens when EVs are just Vs?

The EV revolution happened. It’s time to admit that electric car companies are, in fact, just car companies.

On April 5, 2024, Tesla’s stock was reeling.

On the heels of an alarming report that showed an 8.5% annual decline in Q1 deliveries, Reuters reported that Tesla was canceling plans to produce its long-promised inexpensive car that was supposed to help the EV maker reach a broader consumer base. 49 minutes after markets closed, Musk tweeted “Tesla Robotaxi unveil on 8/8,” causing shares to rally after hours, erasing the week’s losses.

This has been the story of Tesla, the car company determined to convince investors that it’s a technology company.

When Tesla surpassed a $1T market capitalization in 2021, it was worth more than the next 10 largest automobile companies combined. Investors justified Tesla’s valuation for two reasons: first, they believed that electric vehicle adoption would grow exponentially until it overtook the consumer vehicle market. Second, they believed that electric vehicles were inherently more valuable than their internal combustion engine (ICE) counterparts.

For a while, adoption was on track.

In 2012, Tesla, which was essentially the entire US electric vehicle market (excluding hybrids), delivered 2,600 vehicles, and EVs (including hybrids) were 0.41% of total vehicle sales. Tesla’s deliveries number nearly 10x’d to 22,400 in 2013, hit 50,000 in 2015, 499,550 in 2020, and rose to 1,313,851 in 2022, with EVs accounting for 7.7% of total vehicle sales nationwide.

Panicked incumbents who had ignored the EV revolution pledged billions to EV manufacturing and development in an attempt to catch the market leader. In 2021, Ford announced that it was investing $11.6B to build two massive EV battery plants in Kentucky and Tennessee to power its new EV fleet, touting it as the largest ever US investment in EVs. One week later, they pledged to spend up to $30B on EVs through 2025 to hit an ambitious target of making 40% of their production EVs by 2030. In March 2022, they again raised their investment, this time to $50B through 2026.

General Motors, not to be left behind, said in January 2021 that by 2035, they planned to end production of all gas and diesel powered vehicles, and in June, they announced that they would be increasing EV investments to $35B through 2035.

Even Hertz, the formerly bankrupt rental-car company-turned meme stock, announced in October 2021 that it was ordering 100,000 Teslas to frontrun consumer trends in the rental market.

A slew of startups, sensing investor appetite for electric vehicles, filed to go public, with Lordstown Motors, Fisker, Canoo, Nikola, and Lucid announcing merger deals with SPACs, while Rivian opted for a traditional IPO.

In June 2020, Nikola, an electric/hydrogen powered semi-truck manufacturer that had yet to sell any trucks, was worth more than Ford. Meanwhile, when Rivian IPO’d in November 2021, Ford’s own stake in the EV company was briefly worth $18.24B, or roughly 23% of its own market cap, despite Rivian delivering 920 vehicles to Ford’s 1.9M vehicles that year.

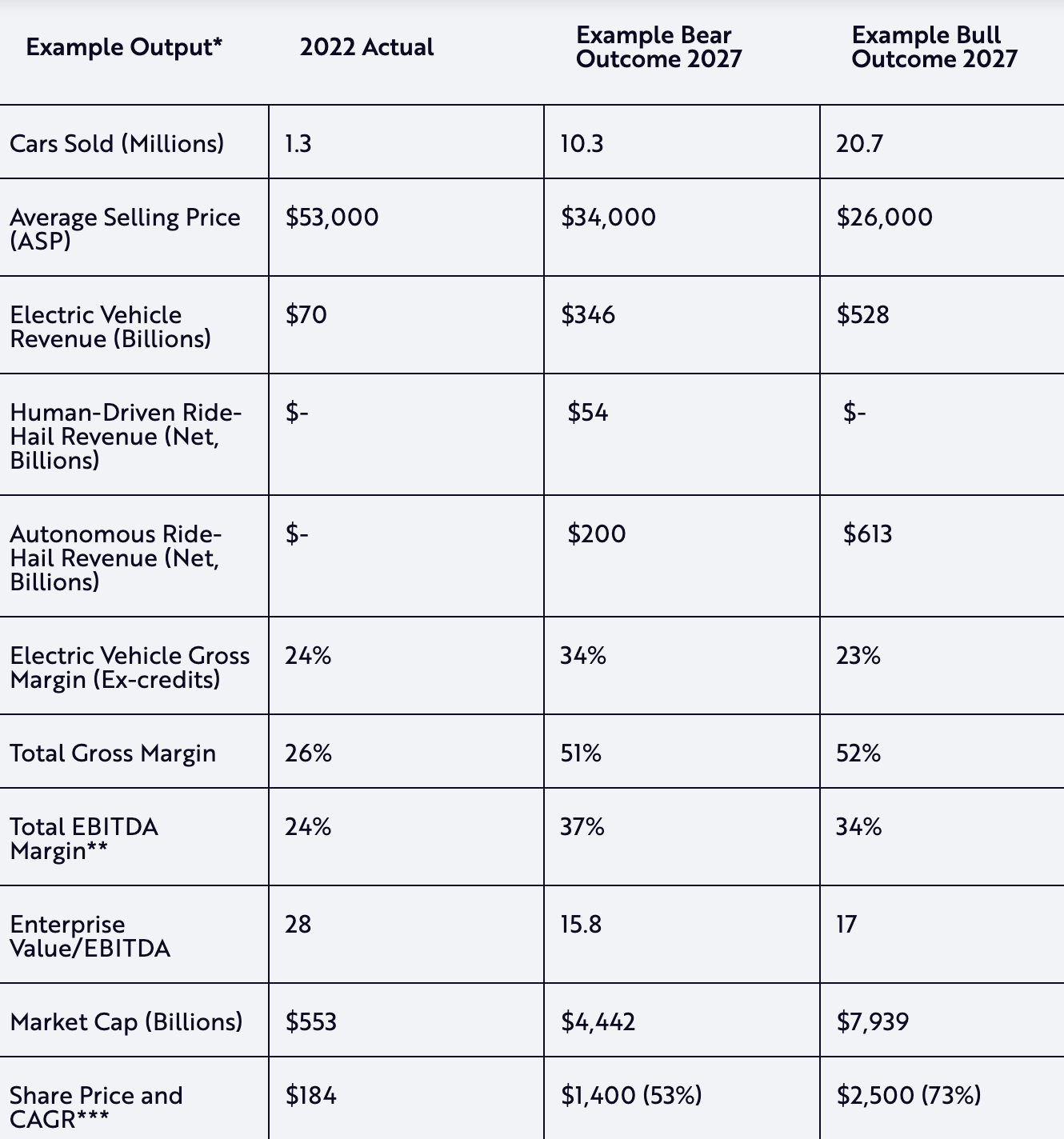

Cathie Wood’s Ark Invest published a research report on Tesla, giving bear and bull case market caps of $4.4T and $7.9T respectively, largely depending on the success of Tesla’s autonomous ride-hail revenue — a revenue stream that does not, as of April 2024, exist. (For those curious, Wood’s bearish model assumes $200B in revenue in 2026 for that segment.)

In 2021, the entire auto sector was pricing in dreams of an electrified future. Three years later, the auto sector is snapping back to reality.

Nikola Motors’ founder was sentenced to four years in prison for misleading investors about his company’s tech, with antics that included pushing a truck down a hill and claiming it was battery powered. On February 16, 2024, Fisker received a non-compliance notice from the New York Stock Exchange as its stock closed below $1 on average for 30 days, and one day later, popular YouTuber and tech influencer Marques Brownlee called Fisker’s Ocean “the worst car I’ve ever tested” a review that now has more than 5 million views. Fisker’s stock is now $0.02. Canoo’s founder spent more company funds on “aircraft reimbursements” than his company generated in revenue, and even Lucid and Rivian, the most promising two out of the bunch, have seen their stock prices drop by more than 90% as they have struggled to hit their delivery targets.

Incumbents’ EV efforts have struggled as well. Ford lost $4.7B in 2023 alone on its EV business and postponed spending $12B on EV factories due to lackluster customer demand. GM abandoned a self-imposed target to build 400,000 electric vehicles by 2023 and delayed its plan to open an EV truck factory in Detroit. At the same time, Tesla’s delivery numbers experienced a surprising decline.

It turns out that making cars is hard, and maintaining consumer demand is harder. When Tesla first started producing electric vehicles, they had two demand tailwinds:

Millions of environmentally conscious drivers wanted an electric car

Millions of drivers wanted to be early adopters of new technology

At the time, the only mass market option was the aesthetically unappealing Nissan Leaf. Tesla couldn’t produce enough cars to meet the demand.

However, with 8% of car sales now EVs, and with Ford, GM, Tesla, Toyota, and other manufacturers offering a variety of models, those initial demands have been satiated, and the rest of America doesn’t care as much about the tech or their environmental footprint. They want something affordable and efficient. EVs are still roughly $10,000 more expensive than their traditional counterparts, and the average consumer doesn’t want to pay a premium for a car they worry they might not be able to charge on the road.

Hertz ignored the preference for convenience to their own peril: business travelers didn’t want to deal with the hassle of an electric car on the road, and many customers turned to Avis instead if Hertz’ only remaining models were Teslas.

Yes, EVs had an exponential adoption curve, but that curve didn’t continue until EVs took over the entire auto market. It lasted until EVs took over the market of consumers who prioritized EVs, which turned out to be much smaller.

Now, there is a glut of electric vehicles. Last summer, Axios reported that there was a 92-day supply of EVs on parking lots, vs a 54-day supply of gas powered cars. EVs weren’t selling, and the resale value for Teslas has tanked as inventory continues to tick up.

With EV adoption slowing, investors are beginning to reconsider whether or not EVs still deserve a valuation premium. A decade ago, when Tesla was doubling its deliveries year over year, you could justify paying up for shares of the car company. But is it still a growth story when deliveries declined by 8.5%? Musk has also done his best to brand Tesla as a tech company, not a car company, promising that full-self driving is imminent over, and over, and over, and over, and over again, including the most recent note about the August 8 debut, and investors tend to pay a premium for tech companies due to their strong margins.

One way to determine if Tesla is a tech company might be to compare its gross margins (revenue - costs of goods sold) to those of other companies. Here are the 2023 gross margins of a few companies:

You can layer all of the technology on top of your product that you want, but at the end of the day, Tesla builds cars, and Tesla sells cars, and the margins on electric cars aren’t much better than the margins on ICE cars.

Yes, Tesla is a very good car company that revolutionized an entire industry. But now that electric vehicles are widely available, and consumers can drive what they wish, it’s time to accept that electric vehicles are just vehicles, and electric car companies are just car companies.