Are Google and Reddit becoming frenemies?

Google’s short- and long-term potential headaches may be neatly encapsulated by its evolving relationship with Reddit.

A brief overview of the relationship between Alphabet and Reddit:

Google pays Reddit for access to its data so it can train its AI models; Reddit receives access to Google’s Vertex AI to help improve its search results.

This partnership resulted in Reddit results getting severely curtailed on other search engines.

Increasingly, when people are searching on Google, they append the word “reddit” to the end of their query.

Reddit launched “Reddit Answers” (an AI-powered, on-platform search tool) in late 2024.

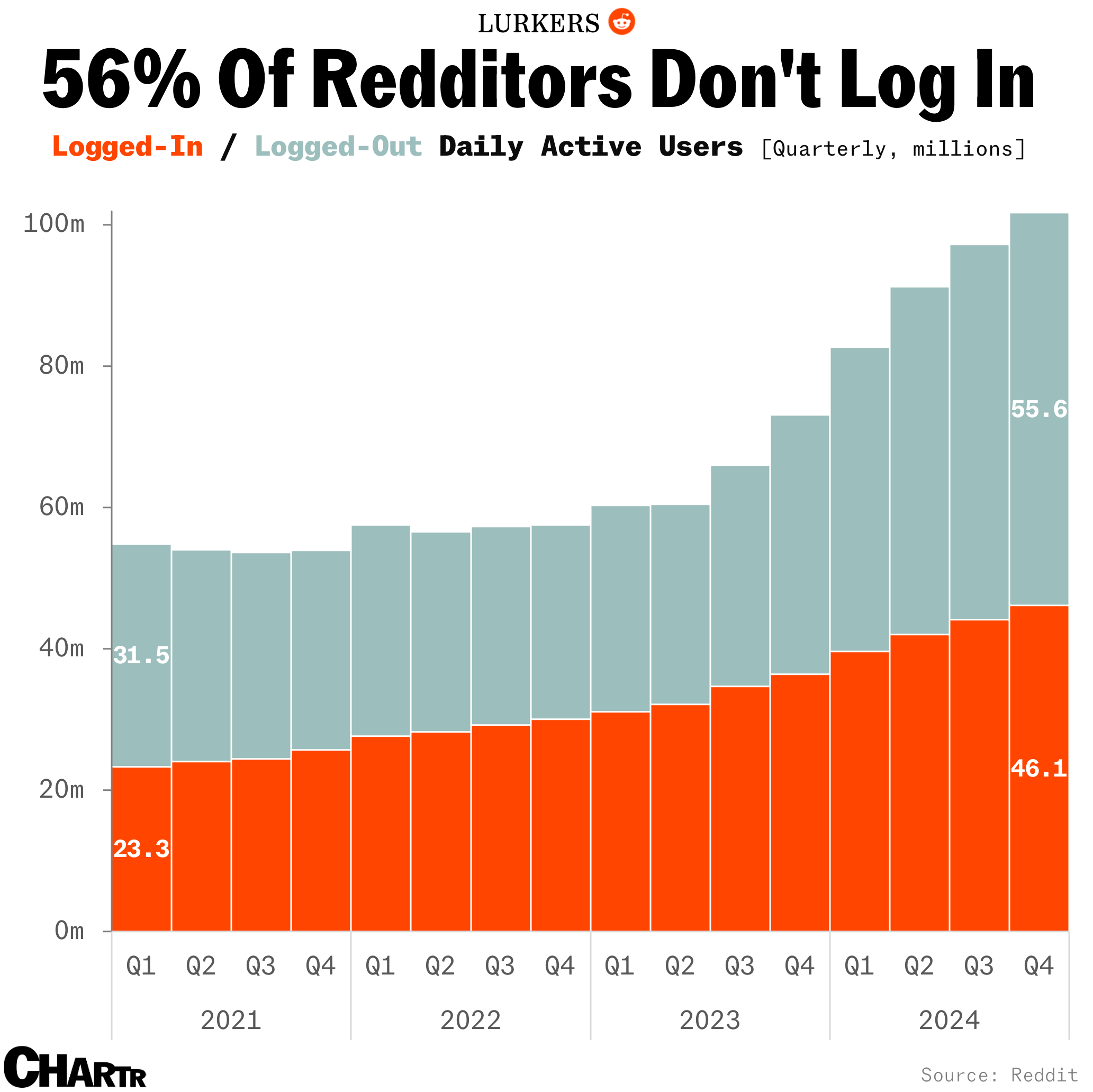

Reddit blamed a tweak to Google’s search algorithm for its disappointing growth in daily active users when it reported fourth-quarter results on Wednesday, sparking a slide in its shares.

Many industries have been blindsided and humbled by algorithm tweaks from the likes of Google and Facebook. Ask any journalist and they’ll tell you, after visibly wincing.

It may be that this change, and its impact on Reddit, was unintentional and proves fleeting.

“We do not believe this was a major change or change targeted at RDDT, but more of the standard algorithmic changes that GOOGL makes multiple times a year (this also coincided with a bug on RDDT’s side that caused RDDT to serve comment pages to GOOGL with comments collapsed, meaning GOOGL couldn’t see the content),” write Morgan Stanley analysts led by Brian Nowak, who deem the sell-off to be a buying opportunity.

However, Reddit’s rise as an ultimate destination in search, at the same time as it’s enhancing its internal search capabilities, threatens to undermine the case for starting your search with Google to begin with. That’s a short-term (and potential long-term) headache.

On the other hand, Google expects to spend $75 billion on capex this year to build out its AI capabilities. Ponying up for Reddit data, along with those billions upon billions in outlays, points to the need for healthy activity on that platform as part of the plan to continue to improve its models, and, in turn, maintain its primacy in search.

As such, there’s seemingly a bit of tension between Google’s short- and longer-term aims (both dominating search, the latter with the aid of AI) that may be revealed in the evolution of its relationship with and actions regarding Reddit.

There are no points for guessing who the big fish and little fish are in this situation: Google still has a decent moat when it comes to search, despite the rise of AI chatbots and even though a decent chunk of those searching end up going immediately to Reddit. Alphabet is a multitrillion-dollar company by market cap; Reddit is not.

It’s a sign of who holds the cards here that Reddit CEO Steve Huffman faced a plethora of questions on Google during the company’s conference call with analysts to discuss its quarterly results, and called the relationship between the two companies “symbiotic.”

Huffman noted that the algo tweak “primarily affects logged-out users in the US” and that the team “adapted nice” and has since seen a recovery in the first quarter.

But this line of questioning from LightShed Partners’ Rich Greenfield was the most direct, and the answers not very revealing.

“What exactly did Google change in the algorithm? I think there’s been a lot of view that sort of Google loves Reddit and was sort of prioritizing Reddit. So what exactly changed? And I guess, Steve, how do you get comfort or confidence that future changes are not going to be more problematic than this one?”

Some excerpts from Huffman’s reply:

“What did Google change? I have my suspicions, but it’s not my place to say, but I’m not worried about it...

We collaborate in a number of ways, including how they can continue to follow us better. So there’s zero concern from us in this department.”

Traders clearly don’t share Huffman’s “zero concern,” judging by the post-earnings plunge in shares of Reddit. And this ongoing relationship bears close monitoring as a flashpoint for how Google may be attempting to balance the competing concerns of dominating search now and ensuring that this dominance endures well into the future.