American Eagle spikes after Donald Trump says its Sydney Sweeney ad is the “HOTTEST” out there

Making products political is among the last thing management teams want (see: “Republicans buy sneakers too”), but American Eagle’s latest campaign has entered the public discourse in a major way since launch, leading the apparel maker to pull one of the ads from its social media channels.

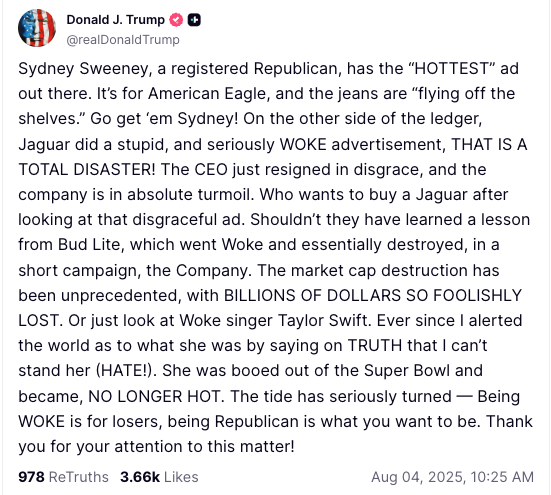

Even so, I doubt American Eagle executives are bothered by their ad campaign with Sydney Sweeney receiving full-throated praise from none other than US President Donald Trump.

The stock surged following the launch of the retailer’s campaign featuring Sweeney amid a wave of retail buying, and conservative media outlets subsequently hit back at criticism of the ad campaign.

Now, the president looks to have spurred another buying spree. Shares are up nearly 16% as of 10:55 a.m. ET on volumes already 70% higher than their full-day average over the past month. Call volumes have topped 58,000 versus a full-day average of less than 18,000 over the past 20 sessions.

While attention may have focused on other areas, this ad campaign certainly seems to have legs.