The US labor market showed signs of cooling in April, and investors are rejoicing.

Job growth of 175,000 came in well below the consensus estimate of 240,000. The unemployment rate unexpectedly ticked up to 3.9%, and average hourly earnings rose just 0.2% month-on-month, a tick below expectations.

It’s the first time all of those metrics came in below economists’ estimates since the October 2023 non-farm payrolls report.

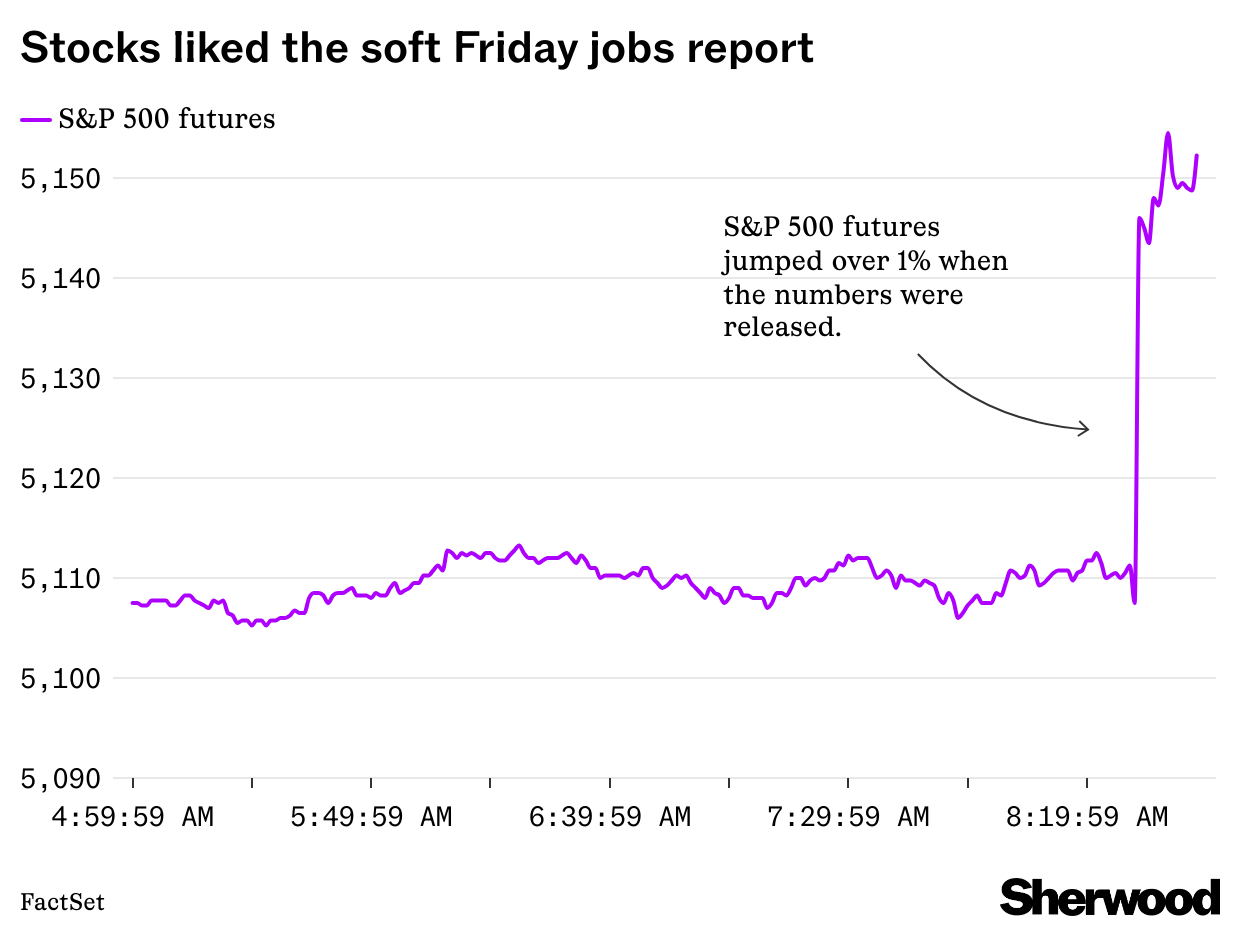

S&P 500 futures extended gains to +1% in the minutes following the release, while 2-year US Treasury yields slumped by as much as 16 basis points.

A 25 basis point cut from the Federal Reserve is now fully priced in by September; prior to the report, traders hadn’t expected that until November.

However, even in a report that missed expectations, there are still signs the labor market remains solid. Of note: the prime-age employment to population ratio (the share of 25 to 54 year olds with a job) inched up to 80.8%.

Investor angst in recent weeks had been centered around the idea that the Fed would be unable to cut rates this year, or might even be forced to raise them further in light of stubbornly hot inflation and continued economic strength.

These jobs data and Fed Chair Jerome Powell’s press conference this week are seemingly assuaging those concerns for now.