Bank of America warns that a $1 trillion source of support for stocks may be fading

Valuations, interest rates... and just the hidden cost of the AI boom are weighing on buybacks.

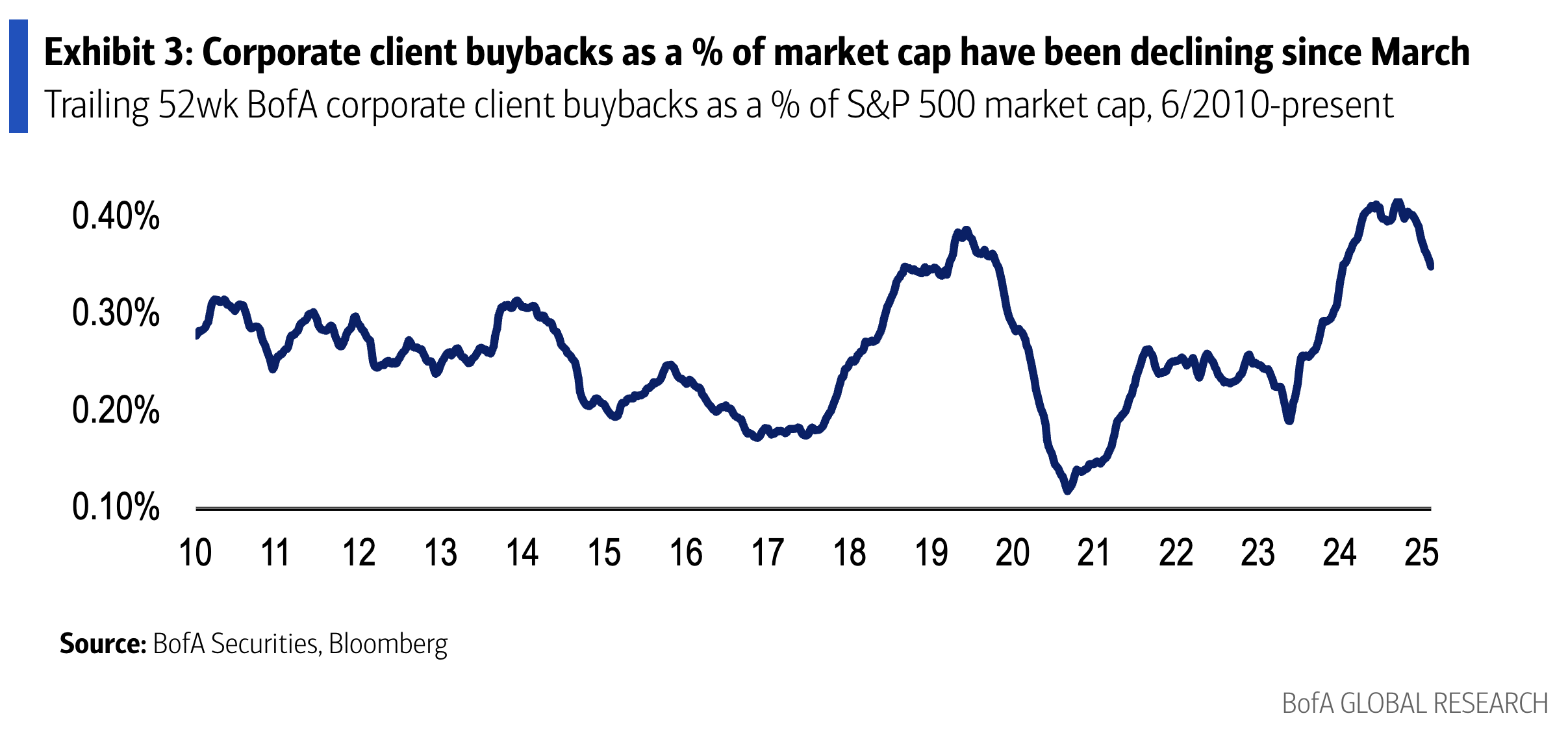

A near $1 trillion source of support for the stock market is starting to dim.

Last year, S&P 500 companies spent a record $942.5 billion buying back their own stock. Now, Bank of America strategists led by Jill Carey Hall are wondering, “Have buybacks finally peaked?”

She wrote:

“Corporate client buybacks slowed and were below typical seasonal levels for the 4th week. While the late start to 2Q results (given timing of July 4th) may be one factor in why buybacks haven’t picked up as much as usual so far, we have actually seen a deceleration in buybacks as a % of market cap since early March, suggesting elevated rates/valuations may finally be having some impact.”

As my colleague Matt Phillips has often written, valuations are high. Corporates are a lot more willing to buy back stock during weaker markets or when valuations are lower — that increases the odds that this capital is being used efficiently.

Right now, some of the biggest US companies already have a very well-publicized use for their capital: on the AI boom, where the risk, in the eyes of the market, is seemingly spending too little rather than too much. Implicit in the rallies in the likes of Meta, Microsoft, Alphabet, and Oracle as they invest hundreds of billions is the idea that these expenditures will lead to even higher shareholder returns down the road.

But in the meantime, the AI capex binge has entailed that buybacks among this cohort as a share of market cap have been dwindling.