CoreWeave guidance disappoints as delays weigh on data center ramp despite blowout top and bottom line beats

CoreWeave reported a strong sales beat in Q3, with bottom-line results to match.

Revenue: $1.36 billion (compared to analyst estimates of $1.23 billion and guidance for $1.26 billion to $1.30 billion)

Adjusted operating income: $217.15 million (estimate: $177.2 million, guidance: $160 million to $190 million)

Those figures exceeded every estimate among analysts polled by Bloomberg.

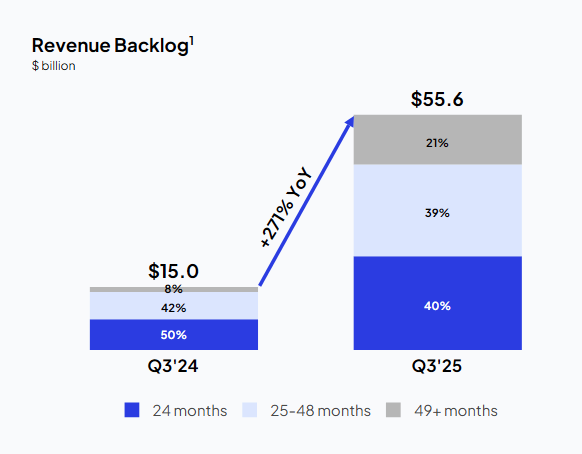

More strong sales seem to be in the pipeline: CoreWeave’s revenue backlog swelled to $55.6 billion at the end of the quarter, nearly double the $30.1 billion at the end of Q2.

But they’re not imminent: in fact, despite this revenue beat, CoreWeave reduced its 2025 annual sales forecast to a range of $5.05 billion to $5.15 billion from its prior outlook for $5.15 billion to $5.35 billion.

That cut to its guidance has shares deep in the red on Tuesday morning during premarket trading.

CoreWeave seems to be having a little trouble getting as much compute up and running as Wall Street had hoped for, with active power of 590 megawatts at the end of the quarter, where analysts had anticipated nearly 625 megawatts.

On the earnings call, the company’s executives discussed a delay to one of their data centers in more detail, a problem which is weighing on its Q4 and FY25 guidance. To be clear, CoreWeave isn’t flagging access to power in particular as a critical bottleneck right now (unlike Microsoft’s and Nvidia’s leaders). Rather, it’s the other physical infrastructure supporting the data center that’s the issue.

Michael Intrator, CoreWeave’s CEO, said:

So you're going to be hearing this theme repeated again and again as you talk to not just CoreWeave, but across the space. And it is a real challenge at the powered shell level. It's not a challenge for power, right? There's plenty of power right now, and we believe that there will be ample power for the next couple of years. But really where the challenge is, is the powered shell.

Accordingly, CoreWeave’s guidance for over 850 megawatts of active power at year end would entail the company falls well short of the current consensus estimates for nearly 900 megawatts.

It’s going to take a lot of supply chain unfurling to realize its revenue backlog on schedule.

The neocloud company had a busy quarter, reaching a $14 billion pact with Meta for AI compute, expanding its agreement with OpenAI, and signing a $6.3 billion deal with Nvidia for any unused cloud computing capacity, among others. CoreWeave’s recent attempt at vertical integration failed, as Core Scientific shareholders voted overwhelmingly against its proposed acquisition on October 30.

However, there’s a little less drama around this quarter’s results than there was for the last one. That’s because its lock-up period expired shortly after CoreWeave’s impressive Q2 results, catalyzing a wave of profit taking in the AI darling.