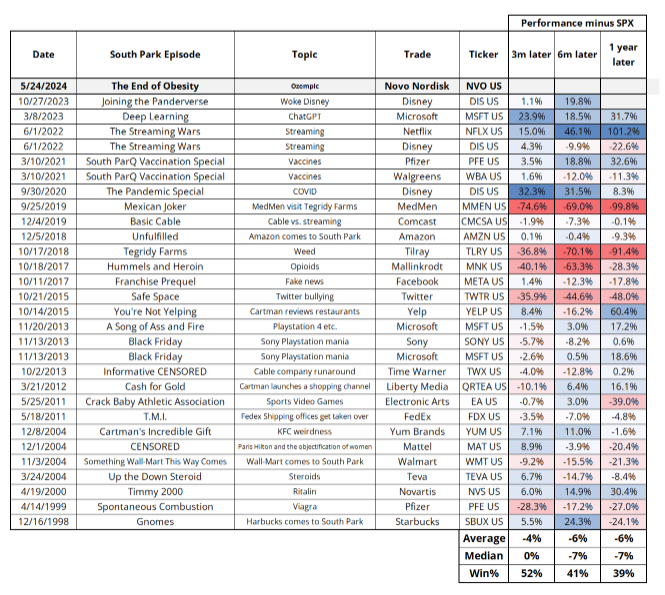

Did South Park mark the top for weight-loss stocks?

Once a company or product is featured on the show, things tend to go badly.

South Park doesn’t just kill Kenny. It may also kill stock market trends.

In the May 24 television special “End of Obesity,” writer Trey Parker directly name-checks Ozempic, the weight-loss drug made by Novo Nordisk, as well as Eli Lilly’s Mounjaro.

Brent Donnelly, president of Spectra Markets, did the leg work and found that once a company or its product is featured prominently on an episode of the animated comedy series, its stock tends to underperform the S&P 500 by 7 percent over the following 12 months.

The rationale behind South Park as a contrarian indicator: if the subject matter is accessible enough that we can laugh at the absurdity of its high place in society, well, it probably can’t command much more mind-share or wallet-share going forward.

“South Park has a 20+-year history of capturing the cultural zeitgeist and it’s impossible to argue that anything that is lampooned on South Park is not priced in,” he wrote in a note to clients.

Or, as James van Geelen, CEO of Citrini Research, puts it:

it’s every momentum investors dream to go long when something is a niche and ride it until it’s a south park episode https://t.co/TMruypVtyu

— Citrini (@Citrini7) May 18, 2024

Here are the stats:

Granted, there’s extremely large variance: Netflix went on to beat the S&P 500 by more than 100% over the following 12 months; cannabis company MedMen, which filed for bankruptcy in late April, underperformed by almost 100%.

Separately, Donnelly noted that new themed exchange-traded fund launches can also serve as a contrarian indicator that strength in a popular pocket of the market is getting long in the tooth. To that end, two firms, Roundhill Investments and Amplify ETFs, recently launched two new products (OZEM and THNR, respectively) that provide exposure to companies offering GLP-1 treatments.

Donnelly’s conclusion: “Not a bad time to lighten up on the GLP-1 basket. It’s all priced in.”