The market is listening to the media

The odds of a 50 basis point rate cut at this week's Fed meeting continue to creep higher.

The pen is mightier than the trading floor’d.

Articles published by prominent journalists who cover the Federal Reserve last week, most notably the Wall Street Journal’s Nick Timiraos, are continuing to prompt a significant re-evaluation of how much the US central bank will cut interest rates this week.

After a so-so monthly increase in the core consumer price index for August, the odds of a 50 basis point rate reduction this week went below 15%. On Monday morning, the likelihood of a cut that large is approaching 70%.

“The Committee is certainly cognizant of the market’s expectations and in the event that a 50 basis point cut is more than 80% priced in, such a move might be the Fed’s decision to prevent a sharp selloff in risk assets,” writes BMO Capital Markets head of US rates strategy Ian Lyngen.

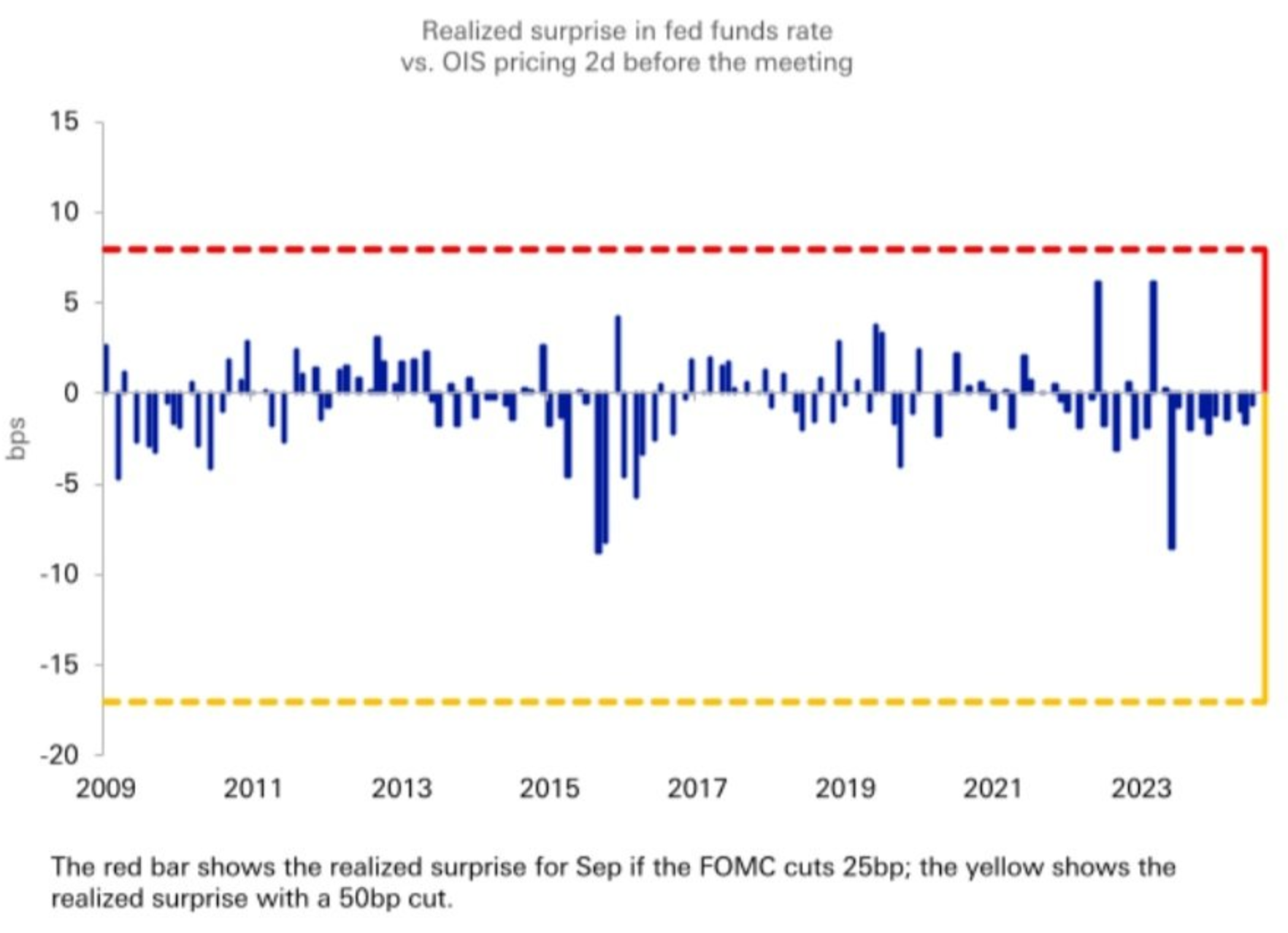

This Deutsche Bank chart from a note published Friday shows just how unusual it is for a Federal Reserve meeting to have this much uncertainty this close to the event. Except now on Monday morning, the state of affairs is flipped – it would be more surprising if the central bank cut by only 25 basis points.

The central bank using a high-profile media contact (often at the Wall Street Journal) to guide the market in a certain direction during the “blackout period” in which US monetary policymakers are unable to speak to the public would not be a new phenomenon. The June 13, 2022 article from Nick Timiraos (“Fed likely to consider 0.75-percentage-point rate rise this week”) stands out. Market pricing implied traders thought there was less than a 30% chance of that outcome before that was published; by the end of the next trading day, the odds of a 75 basis point hike were priced at 90%.

In a separate report, Deutsche Bank economists even turned to their proprietary artificial intelligence tool to analyze the language used in last week’s article compared to Timiraos’ pointed message from June 2022.

The AI results suggested that the June 2022 article’s tone was “urgent and decisive,” suggesting high conviction in the result being prophesied. The more recent post, on the other hand, was “balanced and analytical” with “moderate to low” conviction.

“While there were echoes of that earlier period in this week’s reporting, we also felt that the level of conviction was greater in the June 2022 articles,” write Deutsche Bank economists led by Matthew Luzzetti. “While we know AI results can be inaccurate or subject to criticism, the sentiment analysis from DB’s tool matches our own perception of the conviction level of each article.”

Of course, while media missives appear to be playing the dominant role, there may be more to the massive repricing. After the producer price index and import data that were released following August’s CPI report, inflation forecasters generally expect that the Federal Reserve’s preferred gauge of inflation (released near the end of the month) will have gone up at a very modest pace last month.