Fund managers are worried about AI overinvestment. Bank of America is worried about fund managers overinvesting.

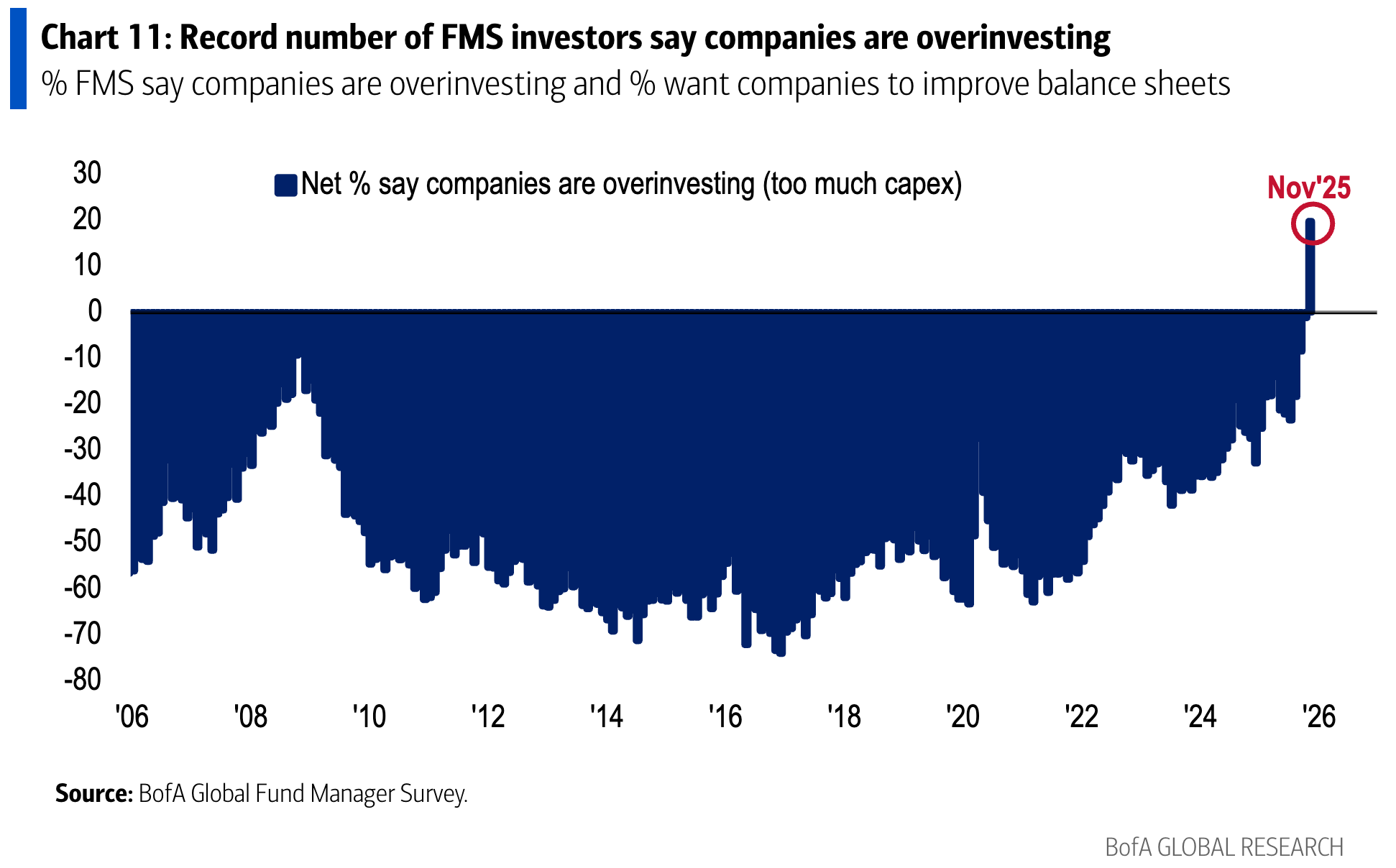

For the first time ever, fund managers surveyed by Bank of America think companies are investing too much.

For the first time ever, fund managers surveyed by Bank of America think companies are investing too much.

“Bad news…1st time in 20 years investors say companies ‘overinvesting’ (read ‘slow down, hyperscalers’),” Chief Investment Strategist Michael Hartnett wrote, commenting on the results of BofA’s monthly fund manager survey. “Asked about the biggest ‘tail risk’ for the economy and the markets, 45% of FMS investors said ‘AI bubble’ (up from 33% last month).”

Now, what this really shows, as Hartnett alludes to, is a very concentrated industry-specific concern around the aggressiveness of the AI build-out. Over on Bluesky, Bespoke analyst George Pearkes flagged that net private investment as a share of US GDP has effectively been a flat line for years.

“Just shows how tech-centric investors are. AI of course might be over-investing but the non-tech economy is stagnating or in recession and definitely isn’t overinvesting,” added Conor Sen, founder of Peachtree Creek Investments. “Office construction is weak, residential construction is weak, the freight industry is in recession, autos are pulling back on some EV spending.”

Fund managers would prefer that companies improve their balance sheets or return more cash to shareholders rather than boost business investment. That would certainly be a shift in what’s been rewarded in the stock market.

Year to date, a basket of the most capex-intensive stocks in the S&P 500 compiled by Goldman Sachs is up over 21%, outperforming baskets of companies with strong balance sheets and high shareholder returns by about 14 and 5 percentage points, respectively. Firms with high levels of investments have also bested these other cohorts over the past one and three months.

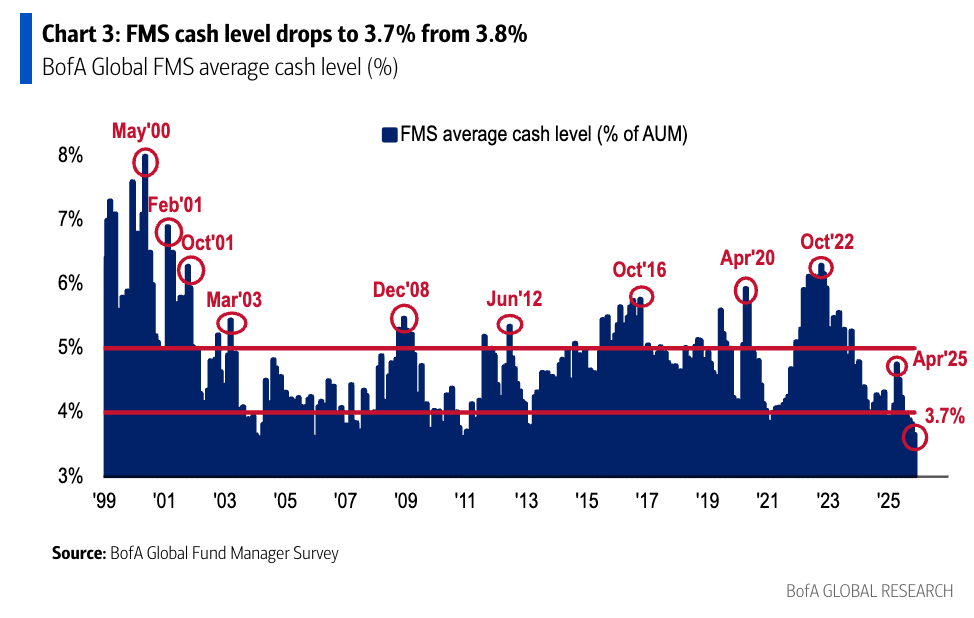

The irony about this survey is that while it says fund managers purport to be worried about overinvestment, if anything, BofA suggests that the overinvestment they should be worried about is their own: average cash levels among those surveyed dipped to 3.7% from 3.8%.

“Note cash levels of 3.7% or lower has occurred 20 times since 2002, and on every occasion stocks fell and Treasuries outperformed in the following 1-3 months,” says Hartnett, who called this low level of dry powder a “sell signal.”