Hot DRAM! Micron up on memory price spike

Micron is riding a year-end wave of price target hikes and ratings hikes, as prices for its core DRAM memory products spike.

Memory and storage chip maker Micron has had a healthy run, with shares doubling 85% over the last three months, thanks in part to spiking prices for its core DRAM product amid the AI investment boom.

In a note Wednesday, Citi analysts upped their target for the shares to $300 from $275, saying they predict good things from the company’s December 17 earnings report.

“We expect the company to post results/guidance significantly above consensus, driven by unprecedented increases in DRAM pricing, as DRAM pricing should increase 50% QoQ in 4Q25,” they wrote.

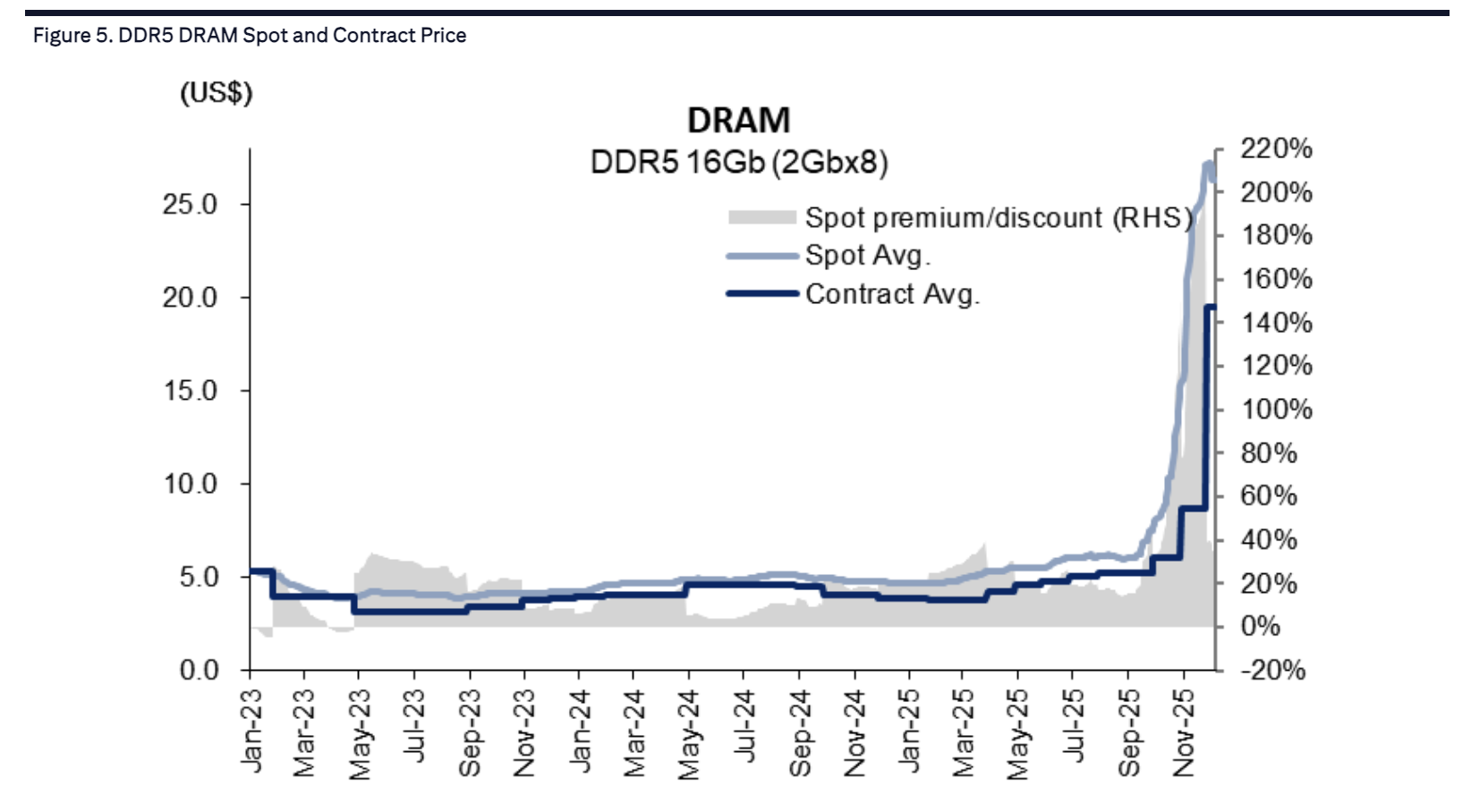

As the chart above shows, this is a pretty remarkable move in prices for Dynamic Random Access Memory, or DRAM. Citi analysts estimate that DRAM sales account for roughly 79% of Micron revenues.

The ubiquitous short-term data storage chips used in computers and phones have long been considered something of a low-priced commodity product. (In fact, at times in the past, DRAM, which acts as a sort of high-speed, short-term memory for tasks computers are actively working on, has been called the “crude oil of the information age” because of its widespread use.)

Citi’s note is the latest in a number of favorable analyst missives on the stock this month, most lifting price targets. Yesterday, HSBC initiated coverage of Micron with a “buy” rating.

The shares have more than tripled this year, and are the fourth-best performers in the S&P 500.