Housing IS the business cycle

Monetary policy famously works with “long and variable lags.” It turns out these lags can be so long that, in the case of this cycle, policy tightening delivered in 2022 and 2023 threatens to weigh on employment in a key cyclical sector in 2025, even though the central bank flipped from raising interest rates to lowering them in the meantime.

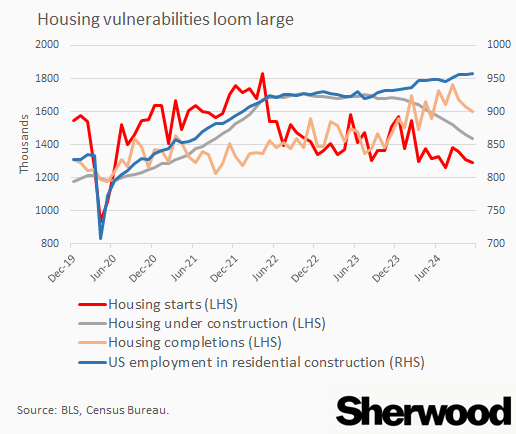

Employment in residential construction stands at its highest level since the run-up to the global financial crisis. Meanwhile, housing starts have been in retreat in tandem with the number of units under construction. That does not bode well for future output from the sector.

In a world where prospective new buyers are deterred by high long-term interest rates, homebuilders are facing pressure on margins thanks in part to trying to subsidize some of this rate sticker shock, and with management of these firms warning of lower-than-expected deliveries in the first quarter of 2025, employment in residential construction stands out as a clear vulnerability for the US job market.

Given the old maxim “housing is the business cycle,” popularized by a well-timed 2007 paper by Ed Leamer of the same name, that means it’s an important flashpoint for the US economy and financial markets as well.

Homebuilders’ shares have not been holding up well lately, with the iShares US Home Construction ETF down 20% from its mid-October peak to its December trough.