Lending the UK government a few quid hasn’t been this lucrative for decades

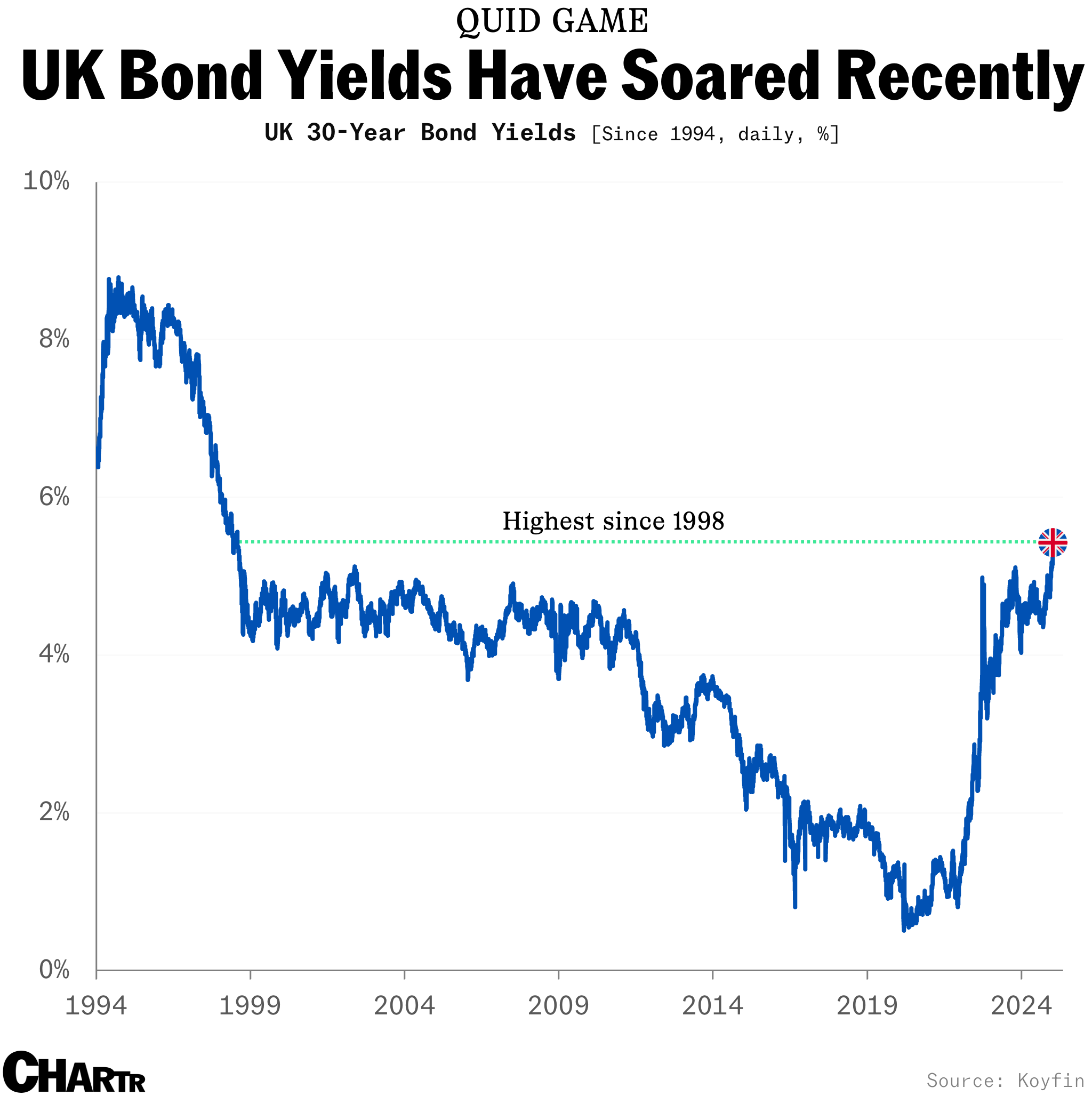

UK bond yields are soaring as investors demand higher returns to lend to the UK government.

Buying bonds is usually seen as a safe, boring bet; somewhere to securely stick cash that isn’t earmarked for a more exciting or higher-risk investment — and buying government bonds is especially so. Returns for buying German bonds, for example, hovered near zero percent for the best part of a decade.

But investors lending money to the UK government for 30 years can now earn as much as 5.35% a year — a record-high yield not seen since 1998 — while the yield for buying a 10-year gilt (what the UK calls its government bonds) has also hit its highest level since 2008 this morning.

While soaring yields may seem like a win for investors, they’re rather a warning sign, as sovereign yields offer some signal on investors’ confidence in that country’s economy. In France, for example, recent budget turmoil pushed yields higher than those of corporate giants like LVMH and L’Oréal, which, though an imperfect comparison, made lending to the French government look riskier than backing its luxury handbags and cosmetics makers.

Gilty of oversupply?

The UK’s rising yields reflect concerns about the nation’s budget: there are simply too many bonds and not enough people who want to buy them, with Tuesday’s sale of £2.25 billion in new 30-year gilts by the UK’s Debt Management Office at a record 5.2% yield. That offering was part of the government’s staggering £297 billion bond-issuance plan for this year — the second-largest on record, which is set to fund public investments by the new Labour government.

However, the market appears hesitant to absorb such a flood of gilts. Investors are wary of the country’s debt pile as growth stagnates (or stops altogether) and inflation stubbornly stays above the Bank of England’s 2% target, dampening hopes for any near-term rate cuts.

Across the pond, US yields have also risen over the last three months, with the US 10Y trading at 4.71% this morning.