The vibes approach to valuing Trump Media

Trump Media's fans don't care about market "fundamentals."

One common reason to invest in a stock might be because you think the company is undervalued, and/or you think that the company’s prospects for increasing in value in the future are favorable.

Another reason to invest in a stock might be “vibes.”

Trump Media and Technology Group went public through a reverse merger with Digital World Acquisition Corp, a SPAC, on Tuesday, and The Financial Times’ Alphaville Research published a research report that included the following quote (emphasis ours):

We believe that a vibes approach to valuing Trump Media is most appropriate. We highlight that the stock has idiosyncratic qualities, in particular around legacy legal exposures. But if November goes as everyone expects, do you really want to be stuck holding anything else? We initiate coverage of Trump Media and Technology Group with a “buy” recommendation and 52 wk target price of $94.

If you are a rational investor, you likely think, “This is a terrible way to value a stock. ‘Vibes?’ Seriously? How about revenue? Profit? Active users?” And then you look at its financials and see that the company earned $3.4 million in revenue with a $49 million net loss, and its declining user base currently sits around 5 million daily active users (X boasts 238 million monetizable daily active users, for comparison). And yet, the company has a $9.34 billion market cap, and its stock price does seem to respond to… vibes.

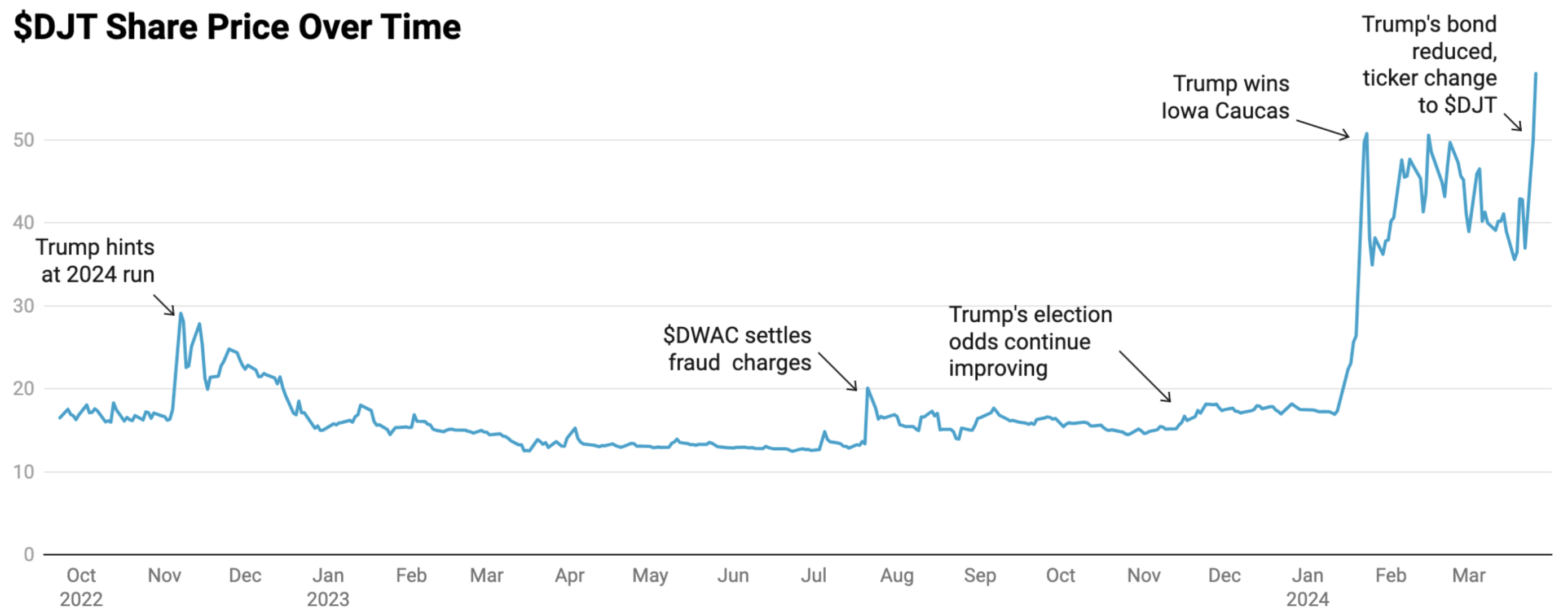

Before the merger closed, shares of the SPAC, Digital World Acquisition Corp, were publicly traded, and its share price moved in conjunction with Trump’s election odds, spiking in January when Trump won the Iowa Caucus.

And earlier this week, we had another vibe check, per CNBC:

Shares of Digital World Acquisition Corp. soared 35% on Monday after an appeals court substantially reduced the bond former President Donald Trump has to post in a civil fraud case, and the company announced it will start trading as DJT on Tuesday.

An irrational investor who supports Donald Trump’s politics might think, “This is Donald Trump’s company, therefore I want to invest in this company to own the libs. Every time Trump has good news, his stock will go up.”

And this is precisely what has happened so far: Trump wins a primary? Stock climbs. Trump effectively locks in the GOP nomination? Stock soars. Trump’s bond for his nine-figure fraud case gets reduced from $455 million to $175 million? Must be great for the stock!

The reverse is true as well. If Trump were to miss his bond payment, or if he were to lose in the November election, the stock price would be vulnerable to negative vibes from 'Trump haters.' More from Alphaville Research:

Additionally, a percentage of the stock is shorted by parties colloquially known as ‘Trump haters’. While these parties represent a risk to the sentiment-based investment case they may become much less vocal after November 5.

The effectiveness of using traditional methods to value a stock depends on other investors also using somewhat traditional methods to value a stock. If you’re valuing a stock based on its financials, and the average shareholder is valuing a stock based on “Donald Trump’s bond got reduced,” it might be useful to incorporate a “vibes” coefficient to your model.

This stock behavior is no different from the collective “meme stock” craze that we have seen since the pandemic began in 2020. Retail investors can be, collectively, a powerful market force, and the speed of information dissemination is near-instantaneous with social media. The combination of these two factors are a recipe for erratic market fluctuations.

“Buy $DJT because Trump might get elected” doesn’t really make sense, from a fundamentals standpoint, but it doesn’t really matter, assuming that enough people are willing to buy for non-fundamental reasons. It’s just the newest rendition of “Buy $GME to fight back against the evil hedge funds!” Was the present value of GameStop’s future cash flows worth $50 billion? Probably not! But the stock went up anyway.

A rational investor, therefore, might think, “Millions of irrational investors are probably thinking, “This is Donald Trump’s company, therefore I want to invest in this company to own the libs. Everytime Trump has good news, his stock will go up.’ Therefore, I should buy this stock because I know his fanbase will buy his stock.”

So if checking fundamentals doesn’t make sense, what are investors left with other than the vibe check?