More bank executives going tieless have Morgan Stanley thinking the bull market is back

A fun observation from Morgan Stanley analyst Betsy Graseck: bank executives are ditching their ties again in what could be a positive signal about the market backdrop.

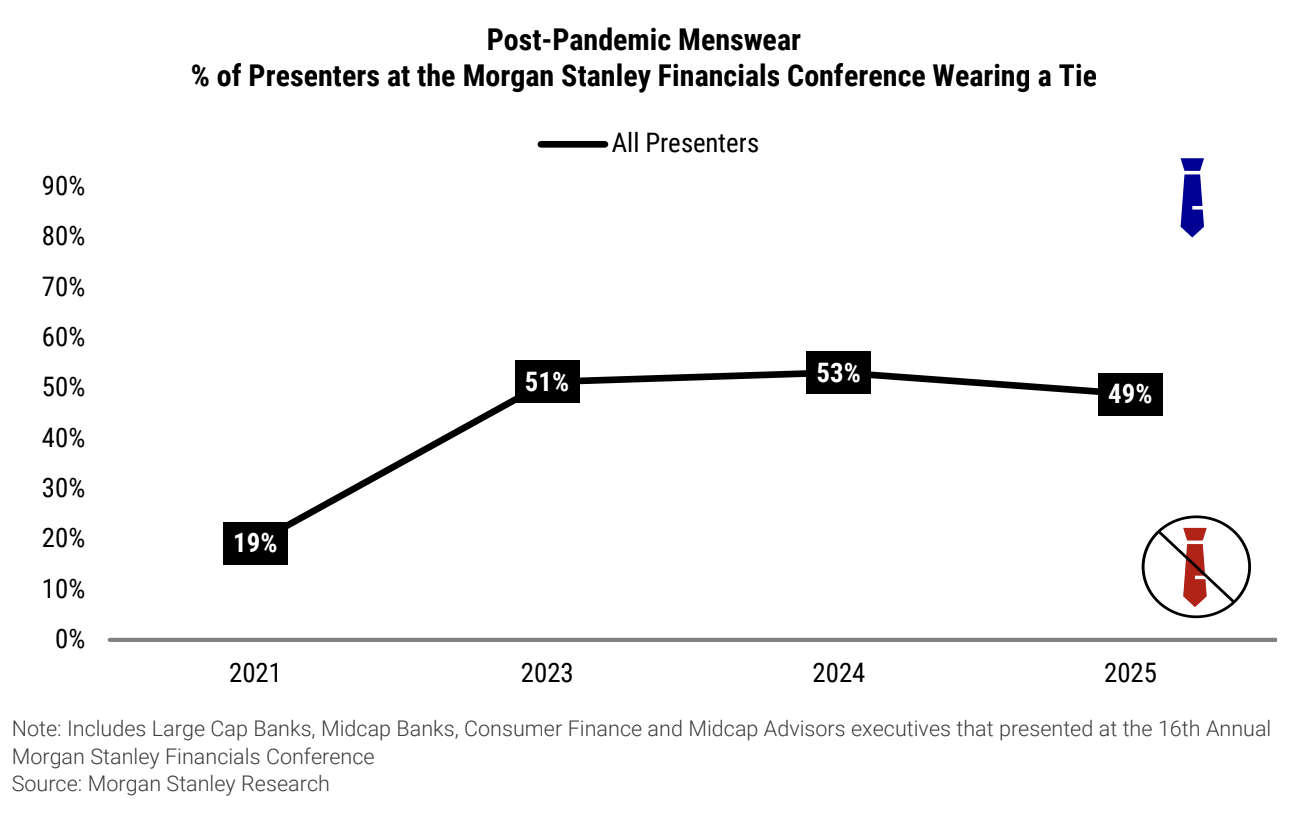

From a note to clients:

“Ever since Covid brought a more relaxed dress code to the financial industry, we have been tracking the return of the tie at our conference. For the first time since we began tracking in 2021, slightly fewer executives as a % of total wore a tie y/y... a bull market indicator? 49% of executives presenting at our 2025 conference wore a tie (menswear only), a decrease from peak of 53% in 2024. CEOs saw the sharpest decline with 67% wearing a tie this year, down from 83% in 2024. CFOs decreased to only 37% wearing a tie, down from 44% in 2024. Other executives were stable at 50% wearing a tie, flat y/y.”

Things like the hemline index (length of women’s skirts) or the thickness of former Fed Chair Alan Greenspan’s briefcase have been trotted out as offbeat ways to track sentiment or price action. Let’s add the necktie indicator to that list.

Wall Street dress codes became more lax in the aftermath of the pandemic. At the extreme, I can remember a day at UBS when summer interns even had a wear-your-pajamas-to-work day.

JPMorgan, the largest US private financial institution, was ahead of the curve in this regard, having relaxed its dress code back in 2016. CEO Jamie Dimon would later don polos in television interviews.

But things apparently got a little tighter under the collar, literally, after 2021 until this year.

In any event, this is great news for those of us who would sooner tie one on than wear a necktie.

Separately, Morgan Stanley’s head of US equity strategy, Michael Wilson, offered a different reason to expect strength in equity prices: it’s the earnings, stupid.

“Key gauges we follow are pointing to a stronger earnings backdrop than many expect over the next 6-12 months, based on our conversations,” he wrote. “First, our main earnings model is showing high-single-digit EPS growth over the next year. Second, earnings revisions breadth is inflecting higher — it bottomed at -25% in mid-April and is now at -9%.”

But who needs earnings when you don’t have neckties?