Oracle’s insane cloud infrastructure forecast is giving shades of Nvidia’s data center business

But it’s just a forecast, of course.

Yesterday, Oracle posted arguably the most remarkable quarter of any tech giant this year, sending the stock up as much as 30% in after-hours trading. Actually, the quarter itself was unremarkable — it was the forecast for what’s to come that completely blew analysts away.

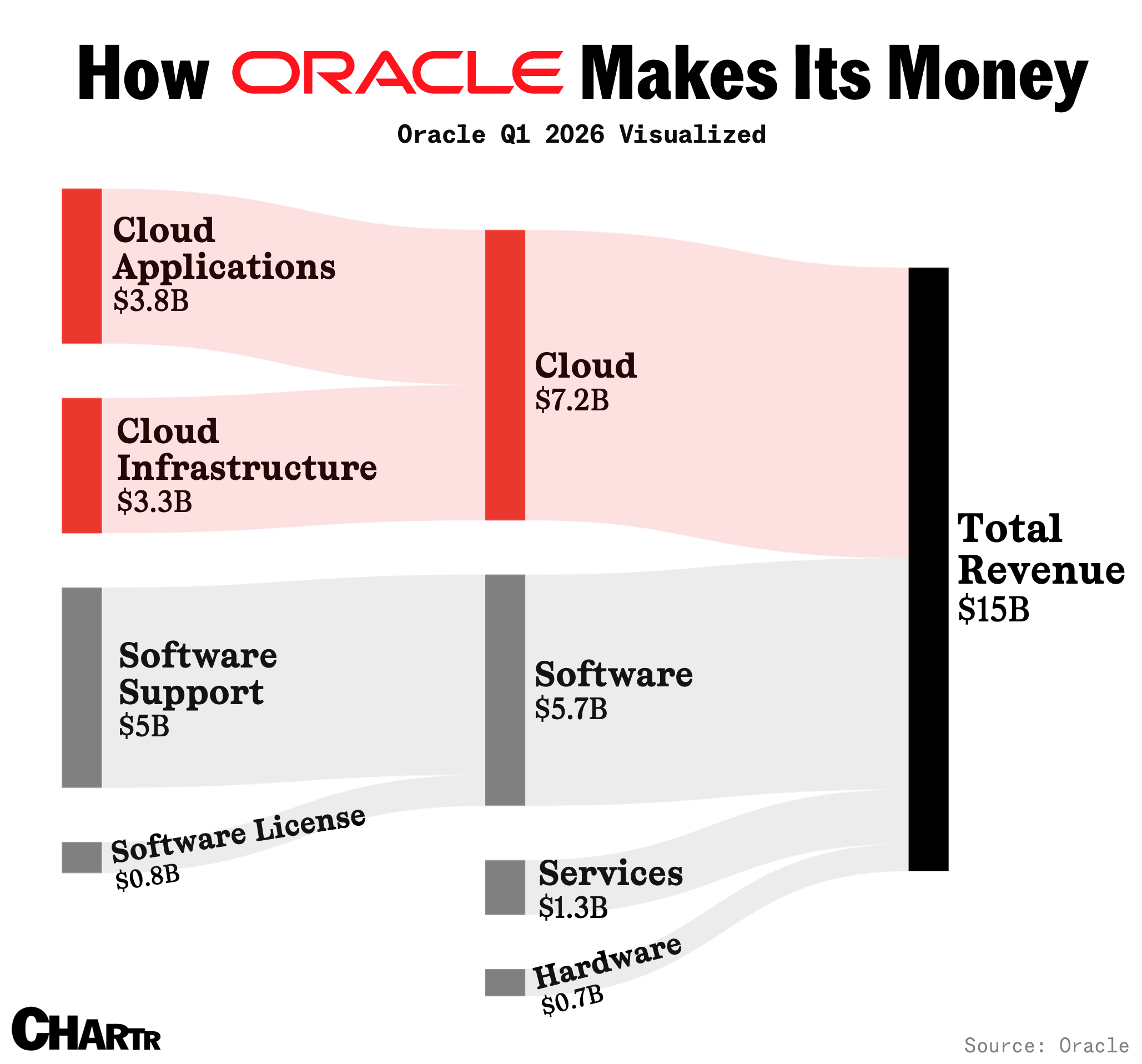

Not a household name like Google, Apple, or Amazon, Oracle has a swath of different specialties, providing software, servers, and cloud services to global businesses.

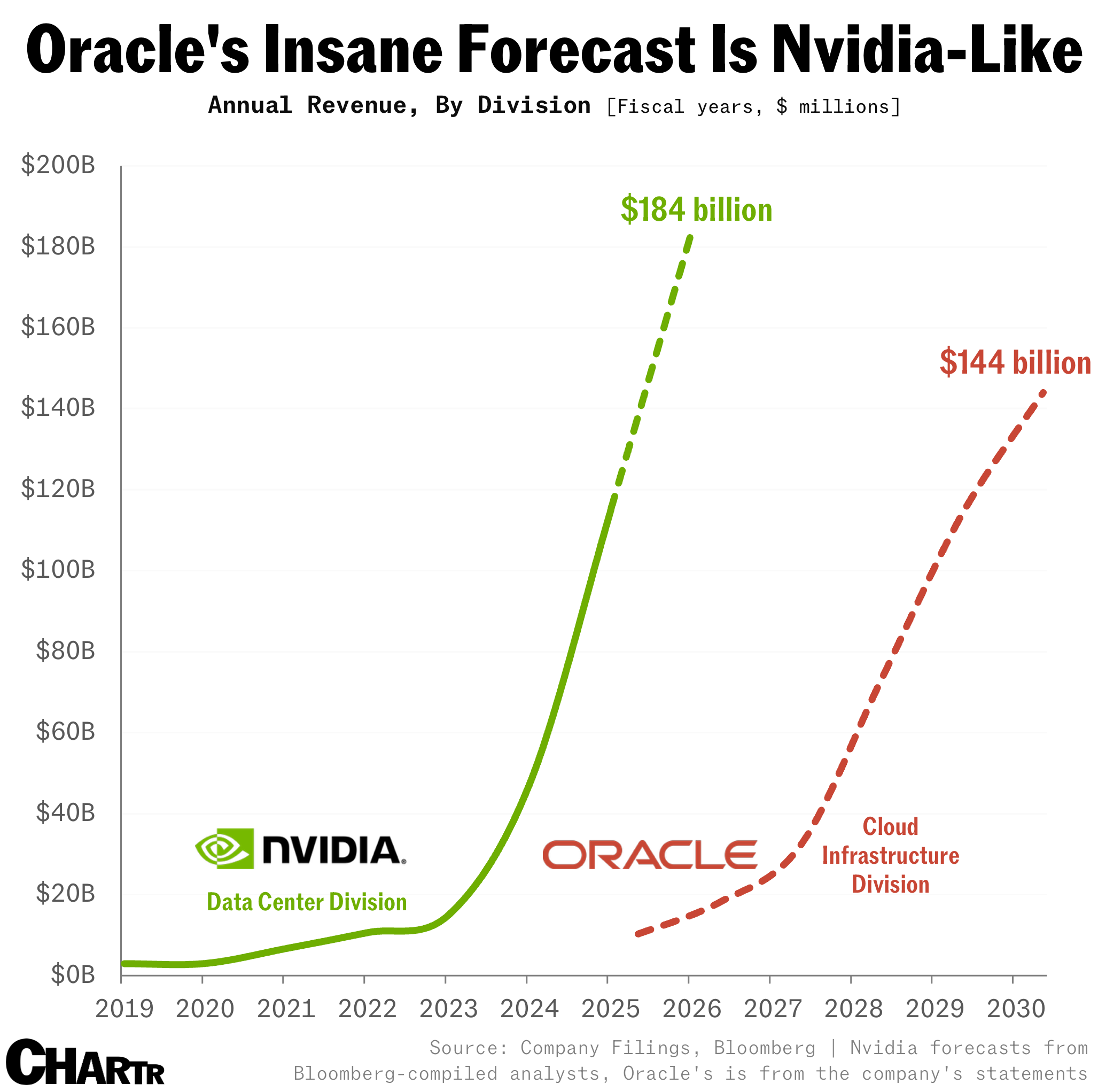

That cloud portion — historically not a major driver of the company’s bottom line — is where Oracle is seeing growth explode, with the company expecting its “Cloud Infrastructure” revenue to rise to an eye-watering $144 billion in its fiscal year 2030. That’s up more than 14x on last year’s ~$10 billion haul.

As hockey-stick revenue projections go, that’s about as bold as they come in terms of sheer scale. If — and it is an if — the company hits that forecast, it will give shades of another AI enabler’s meteoric rise: Nvidia’s data center business, which saw its revenue increase from $6.7 billion in FY 2021 to $115 billion in FY 2025, with analysts anticipating more than $184 billion in data center revenue this fiscal year.

For now, the insane revenue backlog that Oracle revealed, which was up 359% to $455 billion, is enough to be lifting the entire AI space.

At the time of writing, Oracle’s shares are 32% higher in premarket trading, putting the company’s market cap just shy of $900 billion. That’s making Larry Ellison, Oracle’s cofounder, worth an extra $70 billion or so — putting him within spitting distance of unseating Elon Musk as the world’s richest person.