Wheredidallthestocksgo?

The number of public companies has fallen fast

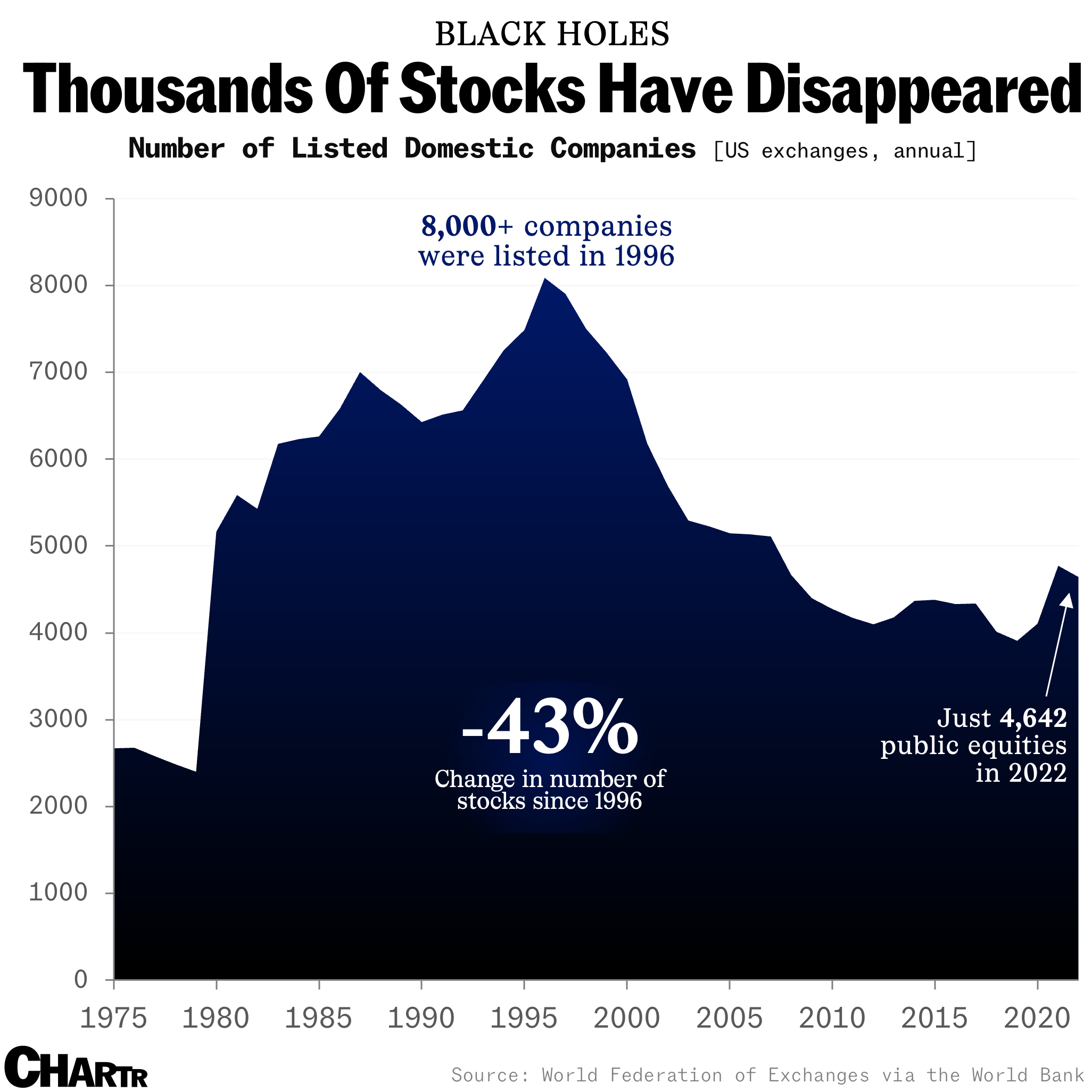

Since the late 1990s, the number of US publicly traded companies has plunged from just over 8K in 1996 to about 4.6K in 2022. (It’s bounced back a bit more recently.)

How come?

There’s no shortage of theories about why this has occurred. A favorite, among American executives, is that new regulations that followed fraud and accounting scandals of the early 2000s — best embodied by the Sarbanes-Oxley Act of 2002 — simply made going public too costly, especially for smaller companies. The self-serving conclusion that such inconveniences ought to be done away with is heavily implied.

This doesn’t make much sense, as the number of public companies had been tumbling for years before those new rules came into existence, much less went into force.

Another popular explanation is the rise of private equity and venture capital. Such massive investment funds that have become more important across the economy since a loosening of securities regulations in 1996. A 2018 estimate suggested that five times as much equity financing was provided to US companies by private investors than public markets.

That is certainly a factor, at least recently. In fact, the term “unicorn” — coined in 2013 to represent what was at the time the rarest of things, a private startup worth more than a billion dollars — has already lost some of its meaning.

In the last few years, unicorns have become almost commonplace: Pitchbook data has tracked the “birth” of more than 1,300 new unicorns just since 2020 — with North American startups accounting for the majority of them. Some of the largest and most influential companies in the world, including TikTok owner ByteDance, SpaceX, and OpenAI, to name but a few, are private companies.

Waiting game

The existence of giant pools of capital outside the public markets is likely playing some role, as it allows entrepreneurs to stay private longer. That slows the conveyor belt of new companies to public markets.

But it’s not the whole story. After all, private investors need to make money, too, and their patience isn’t endless.

An increasingly substantial market for secondary shares — giving founders, early employees, and investors liquidity without the need to cozy up to an investment bank, disclose a tome of information, and run an entire IPO roadshow — has certainly helped some companies such as Stripe stay private. But the longer companies stay private, and the bigger they get, the more likely it becomes that they have to eventually cash out by listing publicly.

Public markets are among the only institutions big enough to write the size of checks they demand. In other words, private equity and venture capital aren’t permanently devouring young companies; they’re just delaying the emergence of these companies as publicly traded stocks.

So where have the missing companies gone? A 2023 paper by a trio of academics suggests a fairly straightforward answer: the Magnificent Seven ate them. Or at least a lot of them.

Davids vs. Goliath(s)

After analyzing the effects of mergers, private-equity investment, and regulatory costs, the paper suggests that M&A is the main culprit. (Though they do theorize that higher costs associated with regulation could be a less important contributing factor.)

“Mergers seem to be the biggest driver of this trend,” Ali Sanati told Sherwood. Sanati is a finance professor at the American University in Washington, DC, and a coauthor of the 2023 paper.

The authors categorized mergers according to various financial metrics, noting that mergers motivated around financing and innovation “are the ones that effectively reduce the number of U.S. listings.”

This stands to reason, for anyone paying a bit of attention.

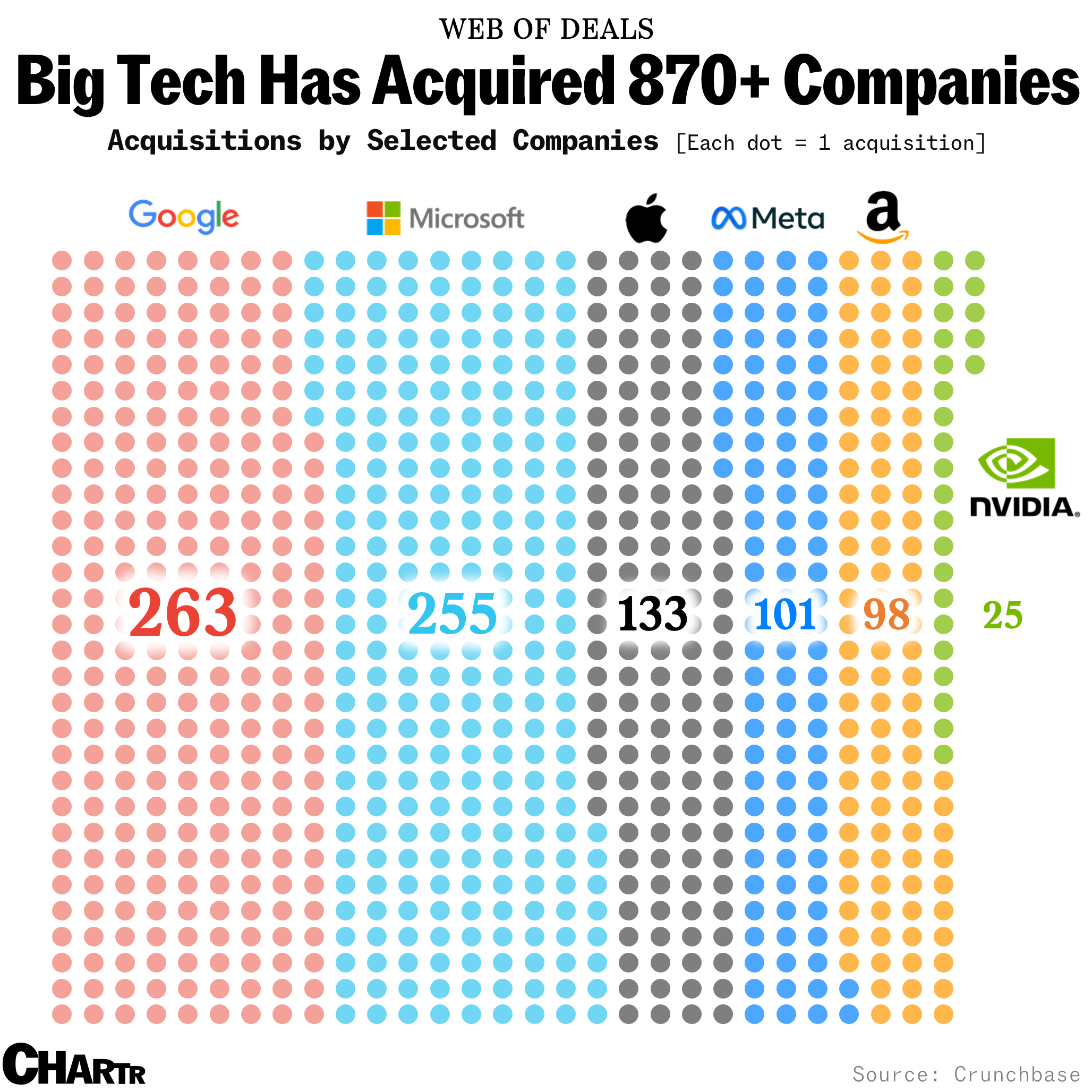

Just a handful of giant, financially powerful technology companies have snapped up literally hundreds of smaller firms since the late '90s. Data from Crunchbase shows that Google, Microsoft, Apple, Meta, Amazon, and Nvidia have together acquired an eye-watering 875 companies.

Google, under its parent, Alphabet, has been the most acquisitive. Alphabet gobbled up 263 companies, 8 more than cloud rival Microsoft, which has done 255 deals. Apple, Meta, and Amazon have all had similarly sized appetites, while Nvidia — the newest member of the "Mag 7" — has done relatively few deals, acquiring just 25 companies. Tesla (not shown) has done just 10.

Of those 800+ deals, lots were acquisitions of small companies… but many of them were not.

YouTube. LinkedIn. Instagram. Fitbit. Whole Foods. DoubleClick. Skype. Audible. GitHub. Beats Electronics. Zappos. Absent their acquisitions by the aforementioned tech behemoths, they would almost certainly all be tradable stocks today, or at least knocking on the doors of the public markets.

It’s not impossible to imagine that some — YouTube and Instagram especially — could have posed a major competitive threat to their current parent firm, if they were operating independently. It stands to reason that such competitive dynamics are a big part of the reason these companies get purchased in the first place, even if execs don’t characterize their thinking quite that explicitly. Mark Zuckerberg, for example, even went out of his way on an email chain to distance himself from any implication that they were buying Instagram “to prevent them from competing with us in any way.”

The broader question is whether the culling of the public markets is a good thing or a bad thing. And of course it really depends on where you stand.

If you’re a shareholder in Meta, it’s undoubtedly a good thing that it bought Instagram. If you’re a company looking to place your digital advertisement, you probably would've been better off with an independent Instagram as an option outside the Zuckerverse. If you’re a consumer, you still have access to both, though it’s likely there are some innovations an independent Instagram and slightly threatened Facebook would've been incentivized to come up with that you’re missing out on.

As for the economy as a whole, Sanati recently coauthored a research paper looking at the potential effects of the drop in publicly traded stocks, suggesting that public companies are better than private-equity firms at turning investment into higher revenues and innovations, quantified via patent filings. It suggests the shrinking universe of publicly traded stocks might be a problem.

"The growth rates in the economy," Sanati said, "kind of depend on the existence of healthy public markets."