This earnings season isn’t about corporate results. It’s about tariffs.

Implied correlations are climbing into the reporting period, a signal that macro fears outweigh any company-specific nuances.

On the eve of JPMorgan’s earnings release, the unofficial kickoff to earnings season, one of the most tried-and-true stock market rules for the reporting period has been completely torn asunder by the trade war.

Typically, the implied correlation of S&P 500 stocks over the next month — that is, how much the members of the index are priced to move independently or in unison — tumbles as we approach the start of earnings.

The reasoning here is simple: different things matter for different companies. So, during a time when we’re getting a lot of company-specific news, stocks are expected to march to the beat of their own drummers.

It’s tough to do that this earnings season because everyone and their mother is squarely focused on one common factor: how much do tariffs change a company’s outlook. So far, a common answer is to say, “I’m not sure.” That’s what Walmart did in pulling its Q1 operating income guidance, what Delta Air Lines’s management said when yanking its full-year outlook, and what CarMax signaled in removing time frames for its financial goals.

The result is that implied correlations are doing the opposite of what they usually do in this window. The chart below shows the one-month change in S&P 500 implied correlations, with vertical lines marking days when JPMorgan reports. The market is saying that macro fears mean we can’t be too nuanced about how individual companies are doing.

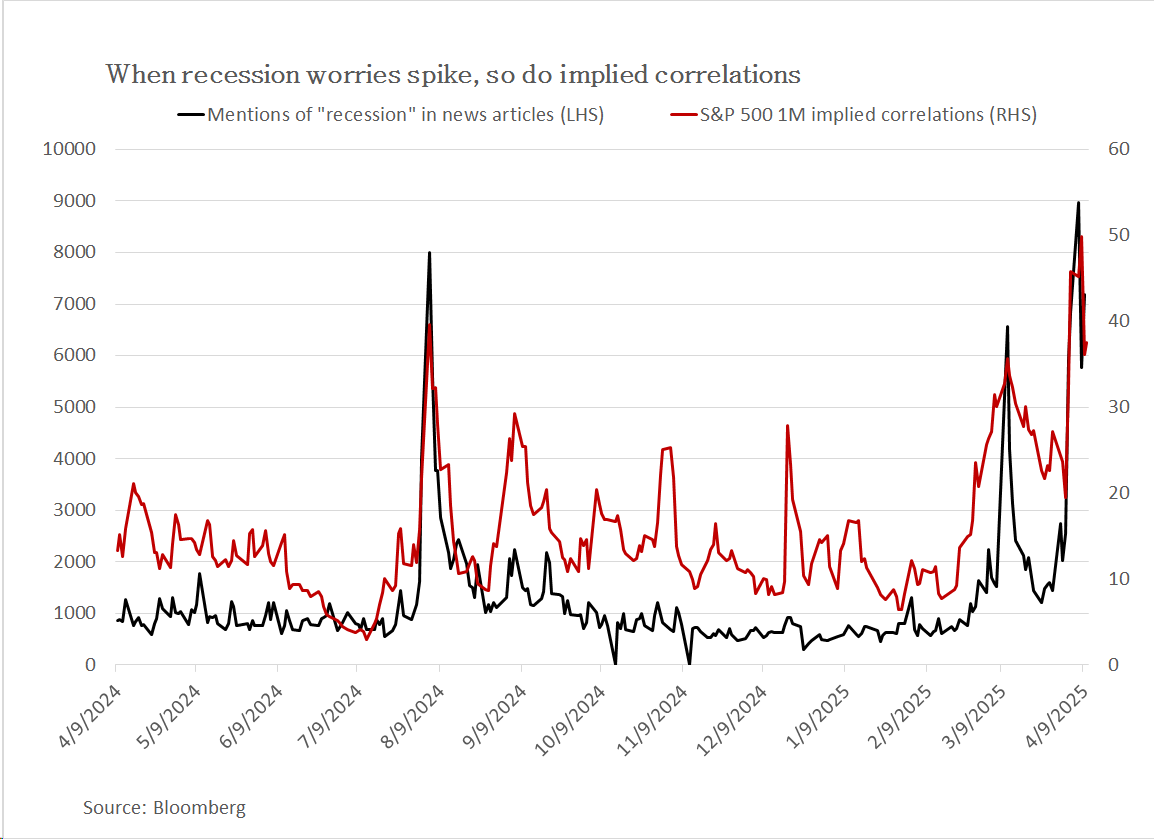

As the old adage goes, in a crisis, all correlations go to one. And a recession, for both markets and humans, is a crisis, because as much as you might hate to hear it, the stock market is the economy. There’s a strong correlation between crescendoes in fear about the economy, as judged by mentions of “recession” in news articles, and the one-month implied correlation for the S&P 500.

That being said, traders are somewhat expecting a reduction in the intensity of the high-volume, everyone-in-or-out-of-the-pool environment we’ve been in during earnings season. That is to say, implied correlations are running below what the strong trading relationship between members of the S&P 500 has been over the past month.