Trump Media surges after SPAC merger

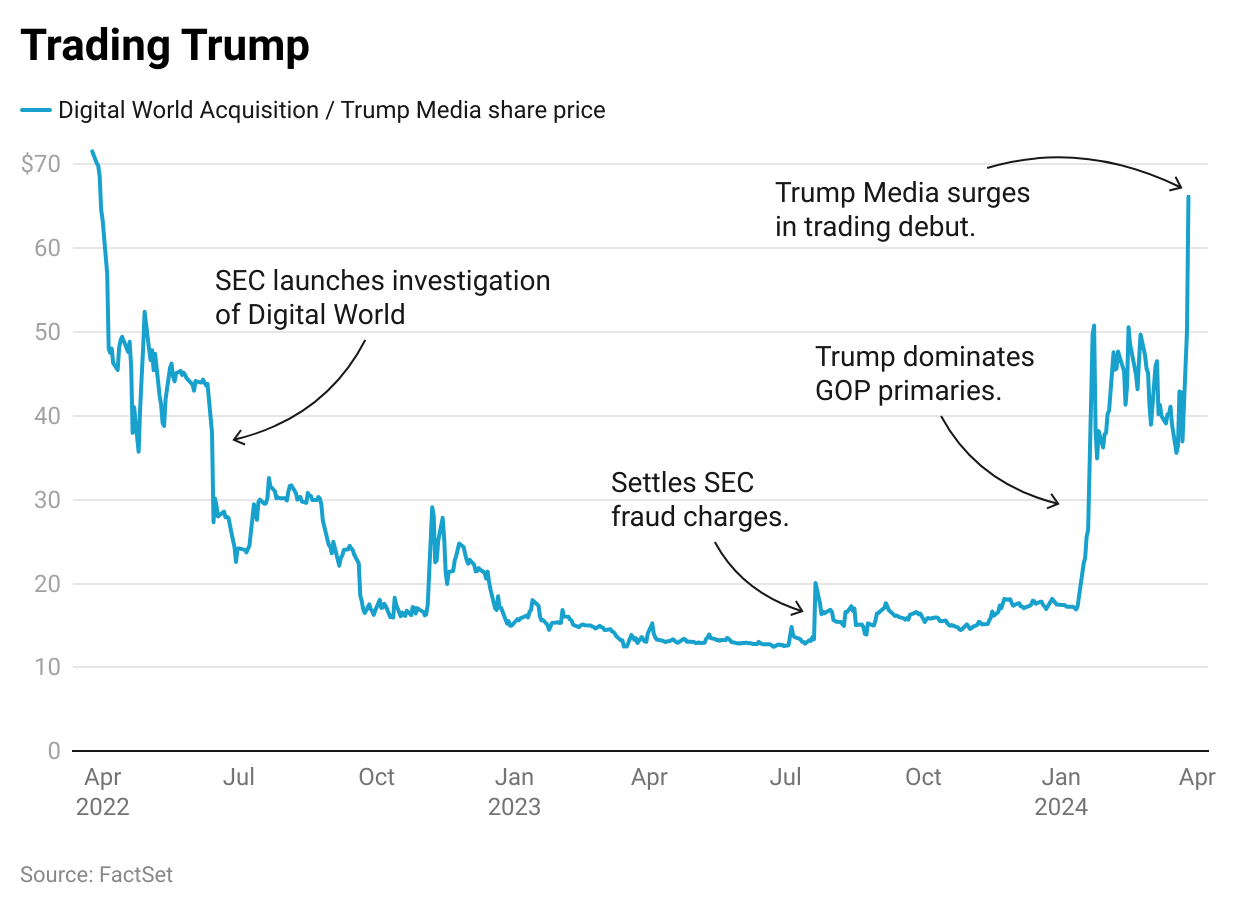

The SPAC-related saga of Truth Social’s parent company culminated Tuesday, with the debut of Trump Media & Technology Group as a publicly traded stock.

Its appearance on the public markets comes after the money-losing company — it lost $49 million in the first three quarters of 2023, according to SEC filings — was merged with a publicly traded, cash-rich shell company, Digital World Acquisition Corporation, on Monday. Former President Donald Trump owns nearly 60% of the shares in the company, which was valued at $5.8 billion before trading began.

The shares surged more than 40% in their first day of trading, which would make the former president’s stake worth more than $5 billion. That’s a welcome windfall for Trump, whose finances came under strain after he was found liable of committing business fraud in New York state and ordered to pay a $454 million judgement, which Trump is appealing.