Fund managers with $500 billion are piling into the same “Trump trades” that mostly fizzled out last time

I guess there’s a reason that they call them “Trump trades,” not “Trump investments.”

The knee-jerk market reaction to Donald Trump’s victory in the presidential election — US equities and the dollar outperforming their peers — has been a case of déjà vu all over again.

And fund managers with $565 billion in assets are diving into so-called “Trump trades” in earnest: the same things that everyone bought the last time.

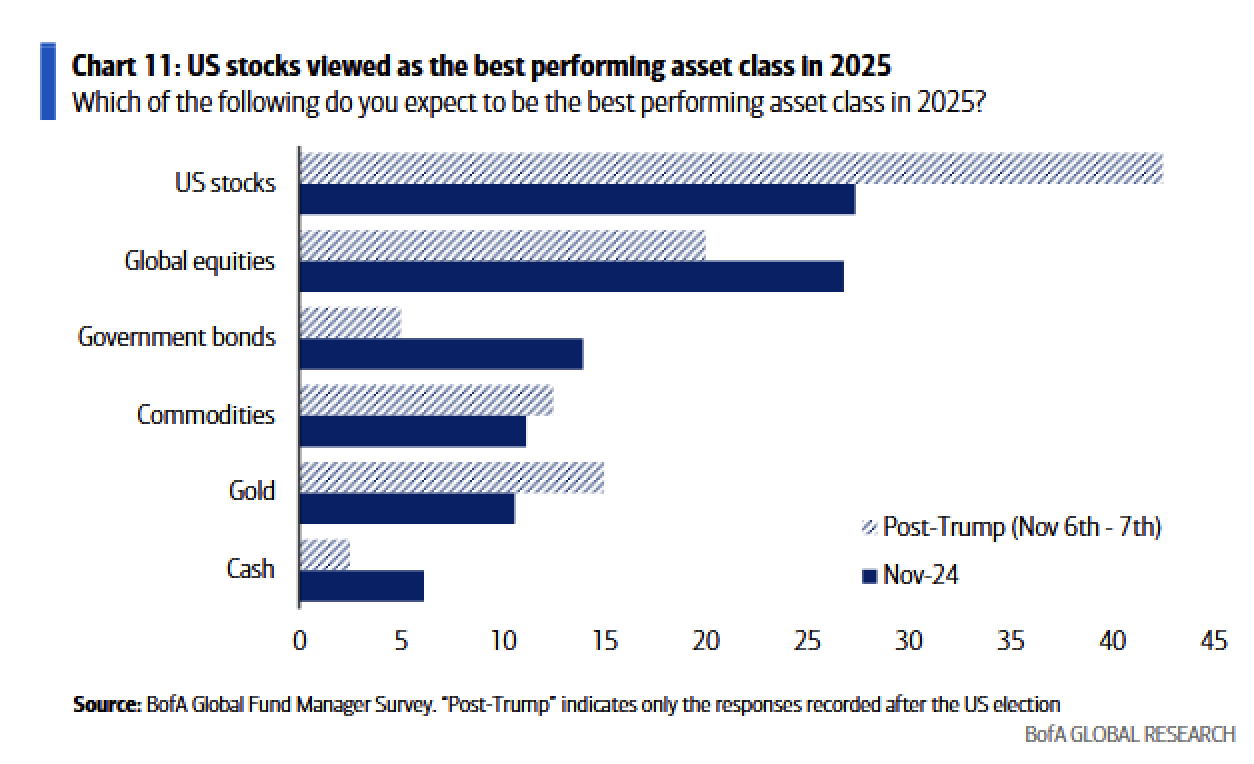

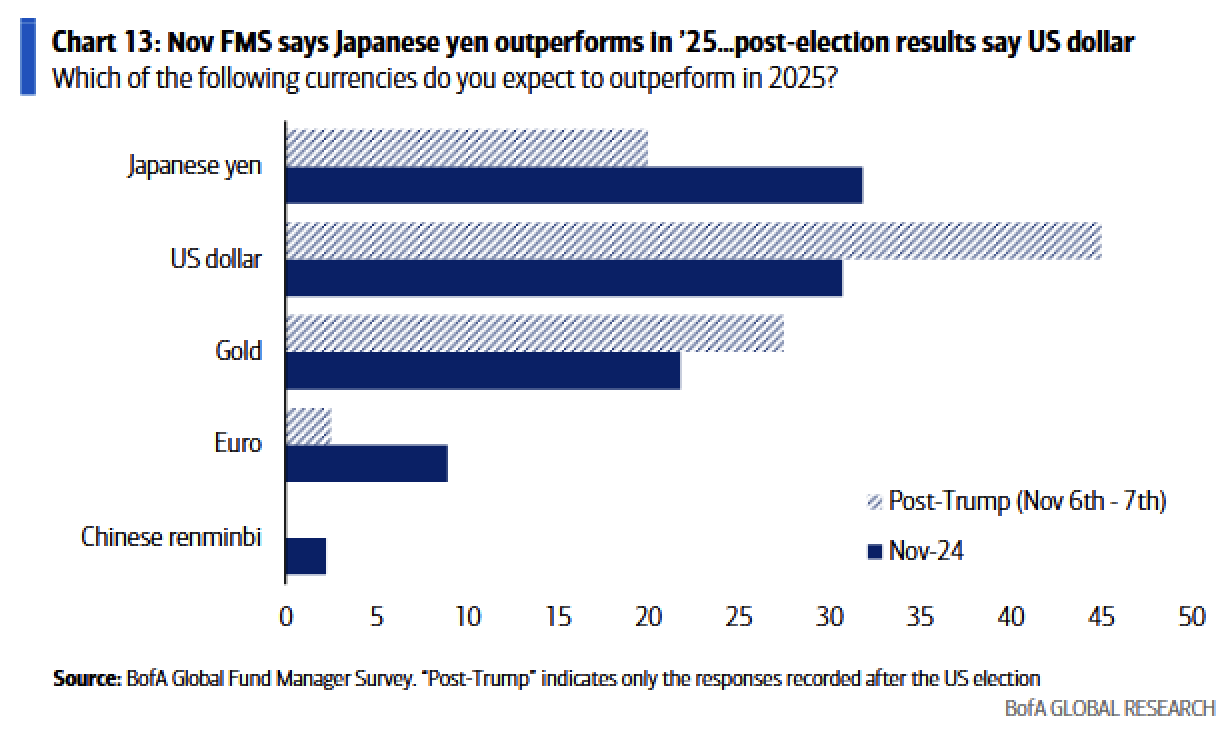

Bank of America’s closely watched global fund-manager survey had an interesting wrinkle this month: with responses received between November 1 and 7, they were able to isolate how much investors’ views changed immediately following the US vote.

The common theme from these respondents, who collectively manage $565 billion, was as pro-US as a bald eagle eating apple pie.

Those surveyed before the election thought US and global stocks would be about neck-and-neck in 2025; now, American equities are decisively the preferred option.

The US dollar? The top pick to outperform in the world of foreign exchange.

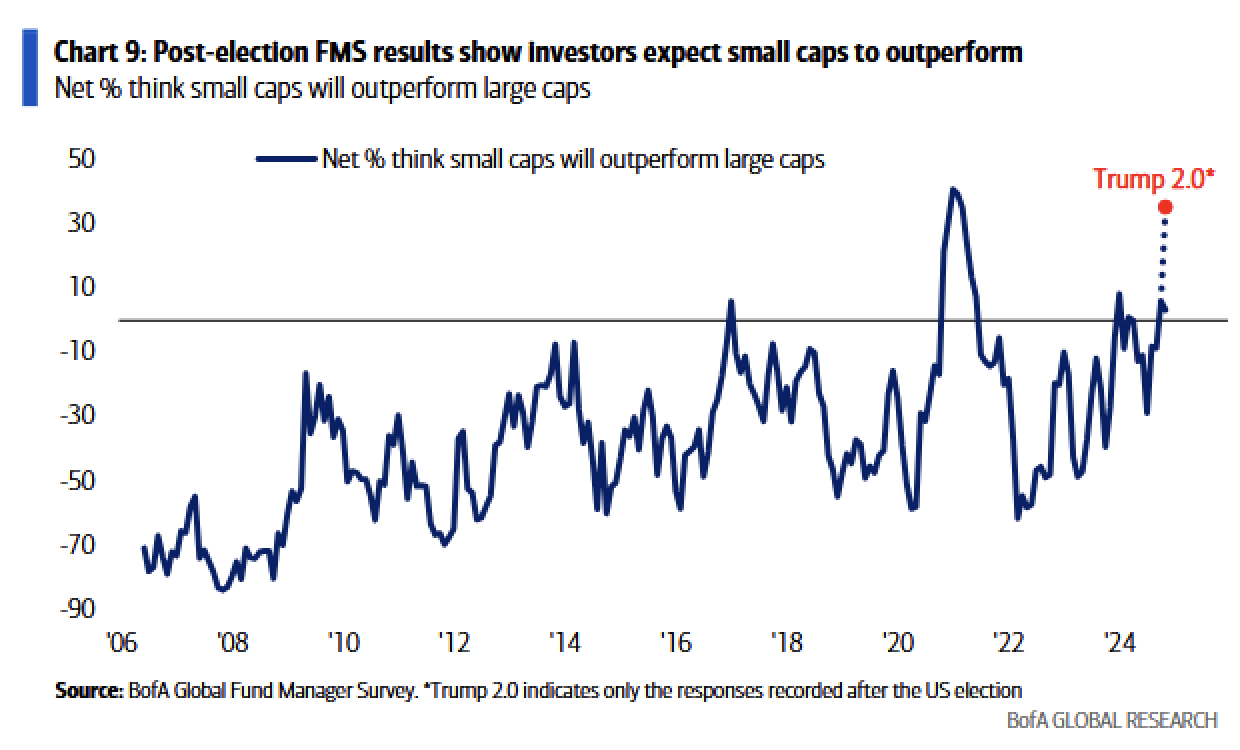

And it’s now conventional wisdom within this group that small caps, which are more sensitive to domestic growth and tax changes, will outperform the S&P 500.

Let’s evaluate how all of these trades fared through Trump 1.0.

Small caps proceeded to underperform large caps by more than 20% from Election Day 2016 through Election Day 2020, even after getting off to a 10% lead within a month of Trump’s surprising 2016 victory. Heck, US small caps barely outperformed developed-market small caps as a whole over this period despite superior US economic growth and the Tax Cuts and Jobs Act, a specific catalyst that benefited this cohort relative to their international peers!

The Dollar Spot Index, which tracks the value of the greenback versus other major developed market currencies? Down between the 2016 and 2020 presidential elections. Oh, what about the Bloomberg Dollar Spot Index, which also includes emerging-market currencies like the Mexican peso and Chinese offshore yuan, which got smacked on the 2016 results? Also down from November 8, 2016, through November 3, 2020.

Then there are US stocks. Yes, these outperformed the MSCI World between Trump’s election win and Biden’s, as they did between Trump’s win and Biden’s after that, and during both of Obama’s terms. You have to go back to George Bush’s win over John Kerry to find a time when US stocks underperformed their global counterparts from one presidential race through the next.

US stocks over their global peers isn’t a really Trump trade; it’s a tech trade.

The S&P 500 has outperformed for a long time primarily due to the outsize earnings power of established and emergent tech giants.

While that profitability was boosted by tax cuts, Big Tech was not one of the key beneficiaries of the TCJA. The yawning gap between the growth in forward-earnings estimates for Nasdaq 100 (which is even more tech-heavy than the S&P 500) compared to the MSCI ACWI between the 2016 and 2020 elections is a story of operational excellence and global footprints.

Fiscal policy, trade policy, regulatory policy, all of that certainly matters for markets. But sometimes (dare I say, oftentimes), there are bigger forces at play, or markets are simply unable to trade the same thematic catalyst for years on end — unless it’s a major factor underpinning incremental increases in profitability.

So-called “Trump trades” are much more a “reaction-to-Trump-winning trades” than they have been durable, investable themes. I guess there’s a reason why they call them “Trump trades” and not “Trump investments.”