Wedbush’s Dan Ives warns Trump’s new focus on household electricity bills risks “slowing down the data center buildouts” at a “crucial time”

Hyperscalers’ margins look well positioned to absorb some higher costs, but some have better trends than others.

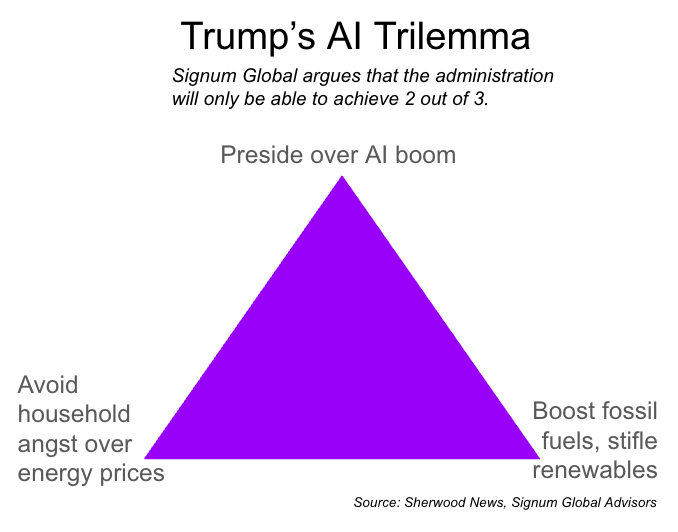

Call it SophAI’s choice.

President Donald Trump is aiming to shield American households from one of the negative side effects of the AI boom — higher electricity prices — by calling on tech giants to “pay their own way.”

This call was quickly answered by Microsoft, which unveiled a “community-first AI infrastructure plan” that will see the company aim to privatize the financial impacts of its electricity demands on the grid, among other measures.

Wedbush Securities’ global head of technology research, Dan Ives, expects similar plans from other tech giants to “follow soon,” he said in a note to clients on Tuesday.

And that’s not necessarily good news to the analyst, who wrote:

“While this initiative alleviates a major headache from the Trump administration, this will create a larger bottleneck with big tech organizations looking to build out large data center footprints as quickly as possible without impacting the bottom-line with this potentially slowing down the data center buildouts with the US entering a crucial time of the AI Revolution with the US facing significant energy shortages/issues to fuel data center buildouts.”

In November, Nvidia CEO Jensen Huang said “China is going to win the AI race” because it has a more favorable regulatory environment and cheaper access to power.

Ives echoed these concerns amid this high-wire, highly wired balancing act by the US government and its leading tech companies.

“With China spending incrementally more across new and existing power technologies into 2030 putting greater pressure on the US to fuel its lofty AI ambitions, we believe this will be a continuous back and forth battle between Big Tech players and the Trump administration with data center buildouts an important aspect of fueling the AI Revolution over the coming years,” he wrote.

My colleague Rani Molla noted that Meta may be more negatively impacted by progress on any presidential ambitions to nudge tech companies to shoulder more of these energy costs. The social media company doesn’t have a cloud business, so its AI costs need to generate revenues that are a little more downstream (in advertising) than its high-spending peers.

Despite escalating depreciation charges, hyperscalers have largely seen their estimated profit margins continue to creep higher. These firms — or in particular, their cloud divisions — are much more profitable than the S&P 500 at large. But there’s one company that is bucking this trend: Meta, the only one of the cohort to see its projected profit margin fall since the end of 2024.

We once again present this trilemma, inspired by Signum Global Advisors’ George Pollack, for your consideration: