Why is Calpers doubling down on private equity investments?

Calpers likes private equity. Is that a disaster in the making?

As things stand, public pension funds are not on track to be able to fully pay pensioners when they retire. And they need to do something about it.

Since 2001, the actuarial funded ratio for state and local pensions, which measures the value of a pension’s assets against its projected benefit obligations (PBO), or the present value of future pension liabilities, has declined from 100%+ to ~78%.

In layman’s terms, public pensions don’t have enough assets to cover their expected liabilities.

So, what do you do if your pension is under-funded, such is the case with the California Public Employees’ Retirement System (Calpers)?

Well, option 1 is that you could just increase your discount rate to lower the present value of future liabilities. For an incredibly simple example of how this would work, imagine that you have $80B in assets right now, your calculations show that you’ll owe $400B in 30 years, and your discount rate for these liabilities is a conservative 4.5%, which matches the 10 year treasury yield (it would make sense for pension discount rates to be conservative, but they rarely are!). The current value of those liabilities is $106.8B, and your funding ratio would be 0.75. If expected market conditions were to change in your favor (this happens all the time, actuaries just need to provide a justification), and your discount rate jumped to 5.5%, your PBO would fall to $79.8B, now matching your assets, and you’re essentially covered. Great! Nothing really changed, but the numbers look better now. This is an excellent feat of financial engineering.

(For context, most state and local pensions do use discount rates ~200+ bps higher than the risk-free rate(s) associated with the timing of their expected outflows PBO, meaning that they are probably already understating their true liabilities).

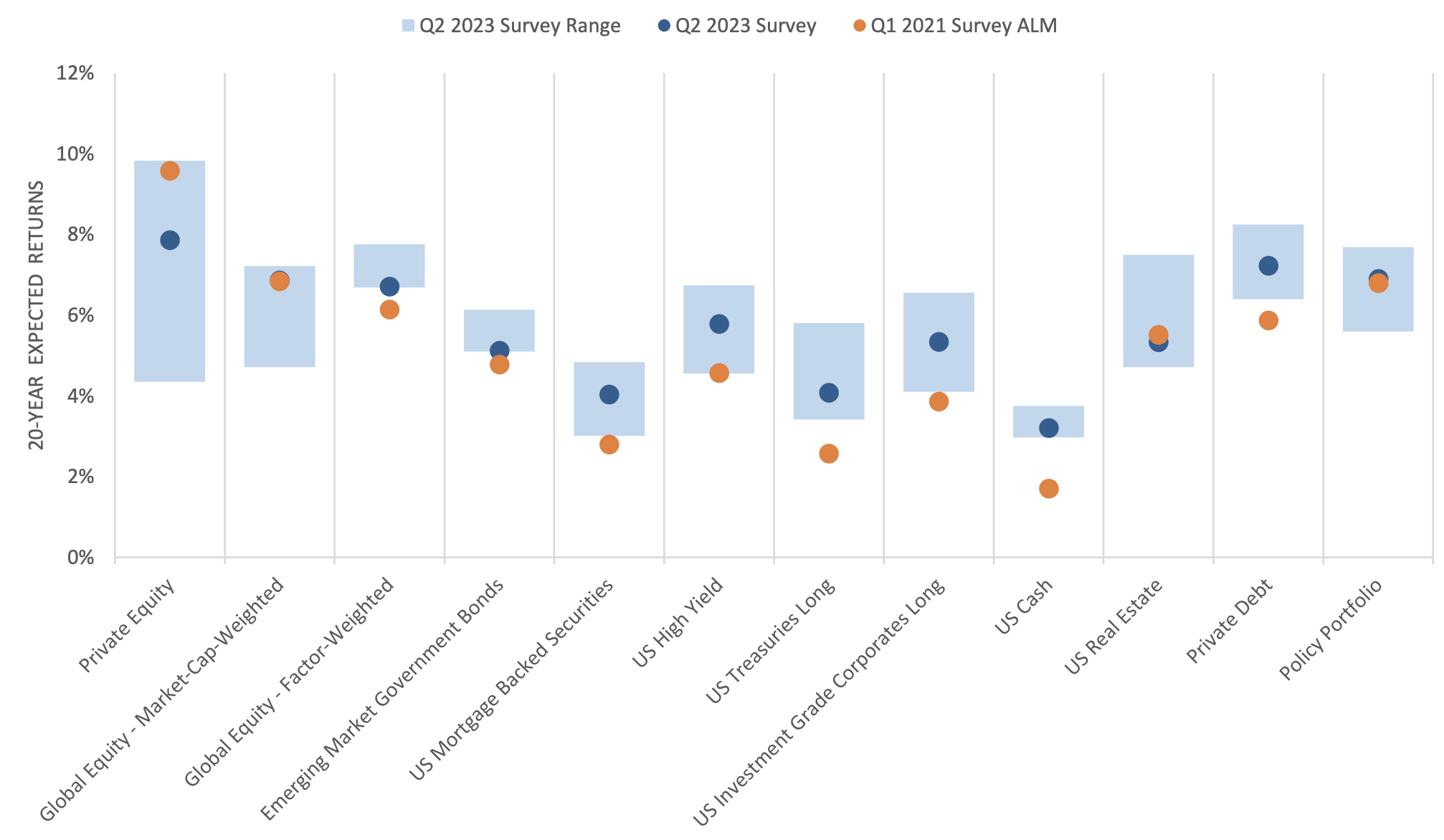

Option 2 is that you could increase your exposure to assets with higher expected returns. From Bloomberg:

The board of the California Public Employees’ Retirement System voted to boost the target allocation for private equity to 17% of its portfolio, up from 13%. It also approved increasing private credit to 8% from 5%. Based on current values, that works out to about $34 billion aimed for private equity and credit, while Calpers plans to pare its exposure to publicly traded stocks and bonds.

The shift reflects confidence that Calpers can ferret out attractive investments even as the fund significantly downgraded the expected 20-year returns from private equity in its latest market survey, citing increased financing costs. The $490 billion pension fund adopted the new asset mix following a mid-cycle review based on updated market assumptions.

For context, Calpers currently boasts a meager 72% funded ratio, and after surveying 15 institutional consultants and asset managers, they believe that private equity will outperform other asset classes, and they are investing their portfolio accordingly.

Source: Calpers

My question is this: is private equity actually a good investment moving forward?

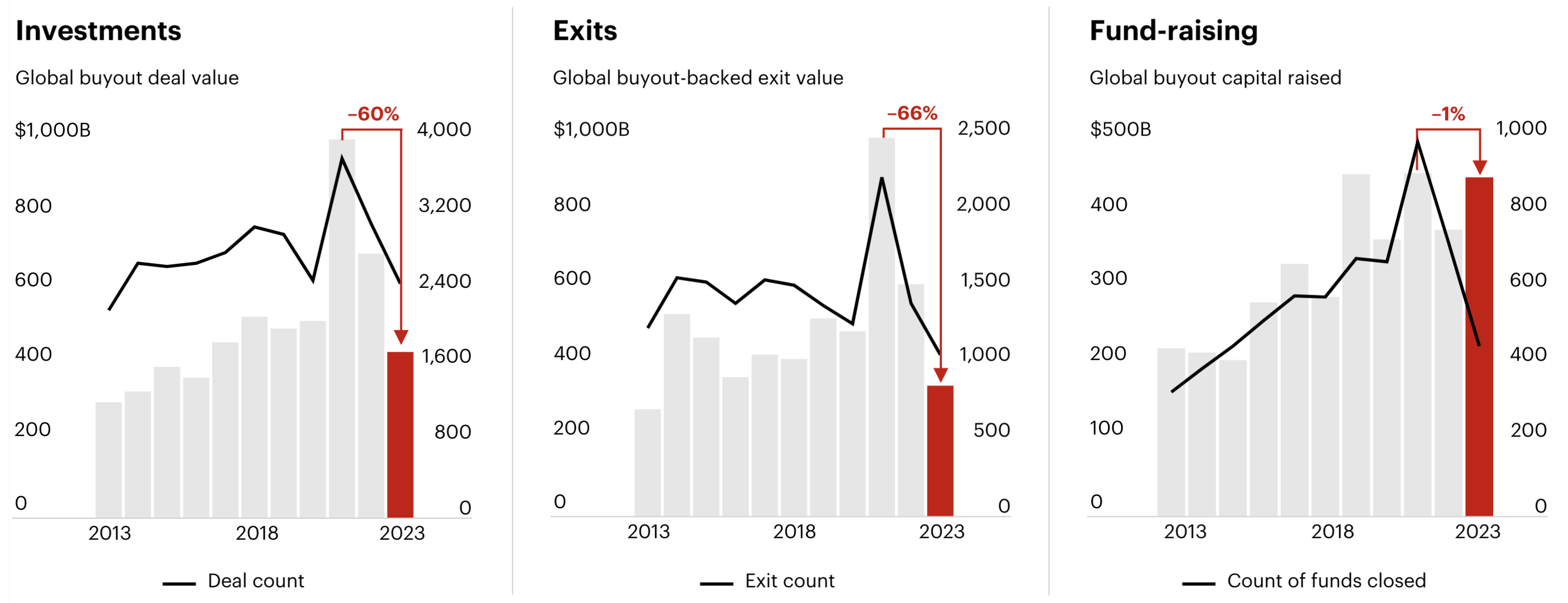

Bain & Company noted in their 2024 Private Equity Outlook that while global fundraising is only down 1% from its peak in 2021, global exits have fallen by 66%. Private equity investors (such as Calpers!) are investing more money than they are receiving through contributions, as there is a backlog of PE companies looking for exits.

In the absence of IPOs and acquisitions, some PE firms have turned to raising new funds, called continuation funds, to buy their own holdings, which, of course, isn’t really an exit. It’s just a firm slapping a new label on the holding company responsible for an investment, which resets the clock on management fees (typically, PE firms make more in management fees in the first 4-6 years of a fund’s life) and, more importantly, allows the firm to capture its carried interest profits from the “transaction.” This is an incredible feat of financial engineering.

So, yes, private equity has outperformed public equities over the last 20 years, but those returns aren’t 1:1 comparisons. The public market determines stock prices. If a stock is undervalued, investors typically bid the price up. If it’s overvalued, investors typically sell it down. Private markets, on the other hand, are inherently illiquid, and PE valuations are quite subjective. Firms use one of three methods: discounted cash flows (DCFs), public peer comparables, and precedent transactions, to determine values. Historically, these valuations were kept in check by exit valuations, but if you can just sell your holdings to yourself at a price you determine, well, that seems problematic.

So Calpers, with its 72% funded ratio assuming an already aggressive discount rate of 6.8%, now wants to reallocate tens of billions of dollars to a private equity sector struggling to sell portfolio companies and distribute capital to investors. This feels like a recipe for disaster, no?