By one measure, stocks haven't looked this bad in decades

Earnings are important, but they aren't everything in the stock market.

Are stocks too expensive? The answer is... it depends.

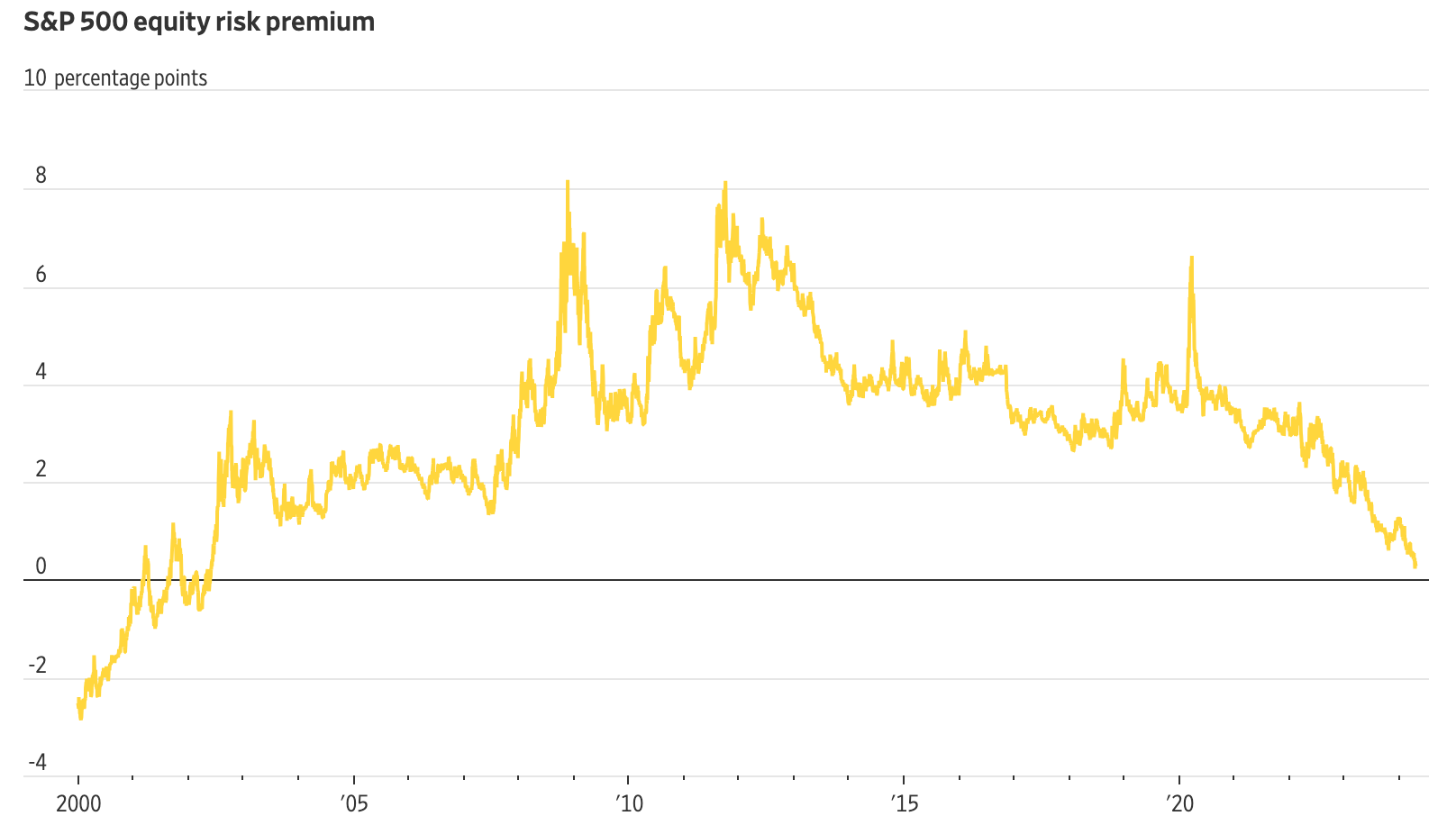

In finance, we use the term "equity risk premium" (ERP) to measure the difference between expected returns from stocks, which are risky assets, and Treasury securities, which are risk-free, to see how much investors are being compensated for taking on additional risk. Typically, the equity side of this equation is the earnings yield, or expected earnings divided by price, of the S&P 500.

Currently, the S&P's expected 2024 earnings yield is 4.2%, while its expected 2025 yield is 4.8%, per Y Charts. Meanwhile, 10-year Treasuries are paying approximately 4.6%.

Yesterday, the Wall Street Journal reported that, as higher interest rates have pushed Treasury yields up, the S&P 500's equity risk premium (using forward earnings estimates) touched its lowest level in 20 years.

This doesn't seem great for stocks! Why invest in equities when you can earn almost the same amount of yield as you would by investing in risk-free Treasuries?

Well, one reason is that the S&P 500's earnings don't necessarily dictate its returns.

Going back to 1960, the average current earnings yield was 6.5%, while the average forward earnings yield was 7.0%. Over that same period, the S&P 500 still averaged 8.6% annual returns.

In layman's terms, the S&P 500 tends to outperform its earnings yield from year to year.

Yes, as interest rates stay higher, Treasuries become more attractive investments. That being said, stocks aren't necessarily doomed just because the ERP has narrowed.