Another day, another “financial advisor” scandal

A financial advisor made millions from allocating clients' nonprofit funding in high-fee variable annuities

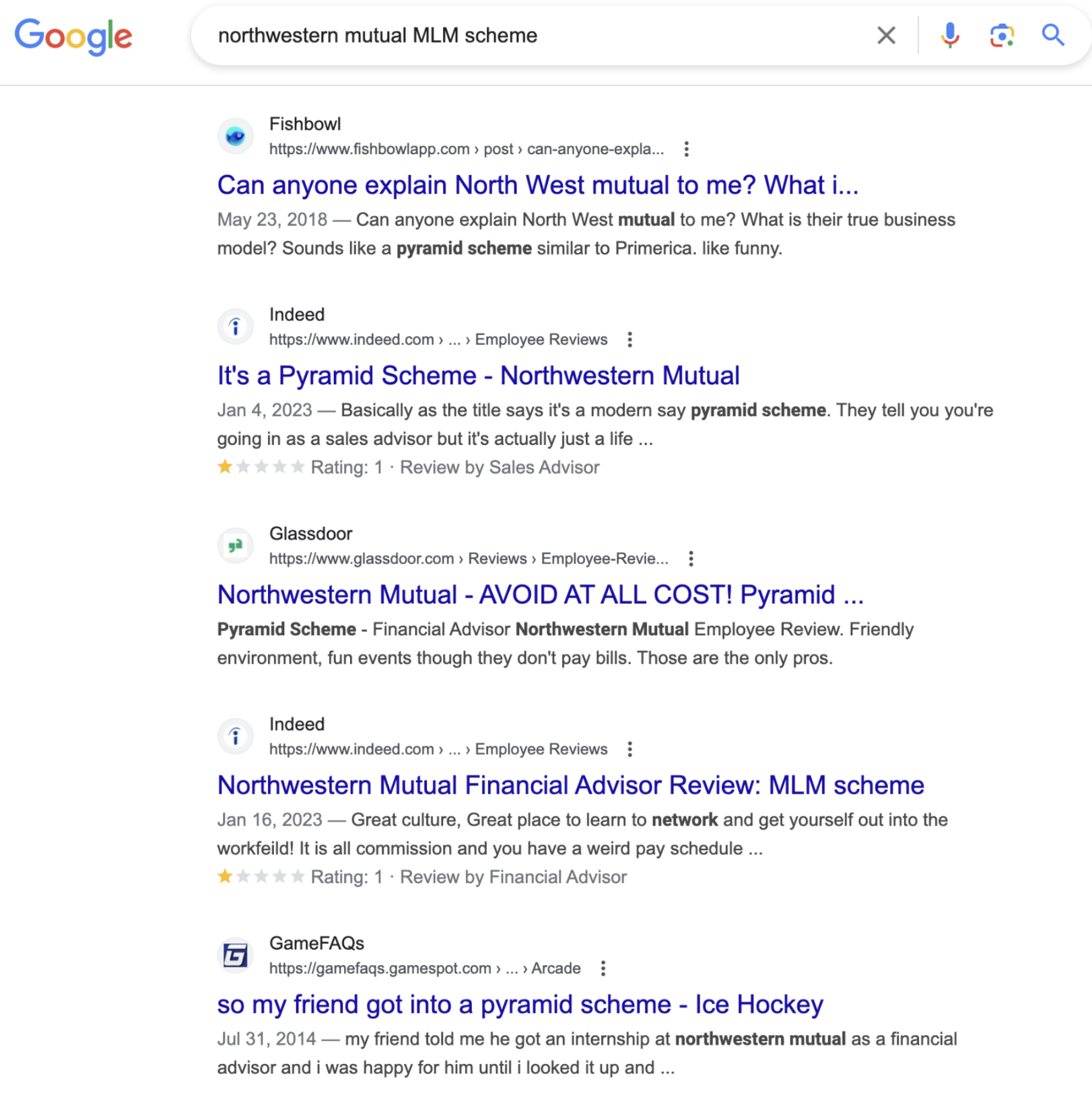

One of the bigger stereotypes in finance is the idea that many “financial services organizations” that offer life insurance and annuities are really just multi-level marketing schemes that pay their representatives lucrative commissions for investing client money in high-fee products. Don’t believe me? Google “Northwestern Mutual MLM Scheme.”

However, this stereotype has an element of truth to it. Earlier this week, The Wall Street Journal’s Jason Zweig published a financial advisor horror story: after winning the Powerball lottery, the Rosenau family created a nonprofit to fund research for Krabbe Disease, in honor of their daughter who had died from the condition. Unfortunately, it appears that they were taken for a ride by their advisor:

The Rosenaus promptly used $26.4 million of their winnings to fund a nonprofit, now known as the Rosenau Family Research Foundation. Its mission is to seek treatments for, and support the families of, children with Krabbe disease. Having almost no investment experience themselves, the couple hired John Priebe, a local financial adviser and insurance agent, to manage the family’s and the foundation’s money. Priebe worked for Principal Securities…

Last month, an arbitration panel run by the Financial Industry Regulatory Authority instructed Principal Securities to pay $7.3 million in compensatory damages to the Rosenau foundation.

According to evidence submitted at the arbitration hearings, Priebe started by buying $18.9 million of variable annuities for the foundation, earning an estimated $1.2 million in commissions.

Those insurance assets generally have all the market risks of mutual funds—at vastly higher costs. Mutual funds, exchange-traded funds and other types of investments typically don’t carry commissions and charge annual fees that can be 0.1% or less. Instead, the variable annuities picked by Priebe charged the foundation annual fees of up to 2% or more and carried commissions that could exceed 6%.

By the end of 2011, Priebe had allocated almost 93% of the nonprofit’s total assets to variable annuities from Principal and several other issuers. In April 2017, Rosenau emailed Priebe, asking him for “a statement disclosing all fees, commissions, charges, transfer fees, etc. of any kind that will be charged for the purchase of any investment device you are planning on using.” Priebe emailed back, “There is no fee’s on this Product” [sic].

Meanwhile, Priebe had been repeatedly selling some of the variable annuities and buying others, earning fresh commissions along the way. All told, he had the foundation buy more than $47 million in variable annuities, according to evidence at the arbitration hearing, generating an estimated $3.3 million in commissions.

A variable annuity is a contract between you and an insurance company, where the company agrees to make periodic payments to you, and the value of the payments is contingent on the performance of the underlying assets the annuity is invested in. The investment options typically include stocks, bonds, and money market funds.

Variable annuities are also filled with fees, such as the following, per the SEC:

Mortality and expense risk charge: ~1.25% per year

Administrative fees: ~0.15% per year

Underlying fund expenses: dependent on fee structure of underlying mutual funds

Surrender charge: fee imposed on early withdrawal of capital, such as a 7% fee on capital withdrawn within the first year

Basically, a variable annuity charges clients 2% annual fees (in the case of the Rosenau family) for investing their assets in the same low-fee mutual funds and bonds that they (or a financial advisor) could have invested in directly. One of the only benefits of choosing a variable annuity over direct investing is its tax-deferred status, but that wasn’t even relevant here!

A foundation isn’t taxable, and it requires steady growth of its assets and ready liquidity to ensure it can meet its annual spending needs. So the limited advantages of variable annuities aren’t useful to a foundation, while their high costs and low liquidity are detrimental.

The “financial advisor” market is, unfortunately, plagued by perverse incentives where advisors stand to make a lot of money through commissions for investing client assets in high-fee vehicles. Couple that with the fact that many clients don’t really understand what they’re investing in, and you have an environment that has made it way too easy to lose millions to fees:

I estimate the foundation could have earned $12 million to $25 million more between 2011 and 2017, when it finally pulled its money away from Priebe and Principal, if it had invested instead in a simple balanced index fund with 60% in stocks and 40% in bonds.

Should we wonder why financial advisors get a bad rap?