President Trump is weighing the merits of a 50-year mortgage — what would that mean for homebuyers?

The math is clear: you might pay a little less per month, but you won’t make a serious dent in your debt for years.

The typical first-time homebuyer in the United States is 40 years old — the highest on record.

That’s a problem, and it’s one that President Trump believes could be alleviated with a 50-year mortgage.

Lately, Trump has become enamored by the idea of a 50-year mortgage, with the commander in chief taking to social media over the weekend to promote the concept, before jumping on Fox News yesterday, describing the plan: “All it means is you pay less per month. You pay it over a longer period of time. It’s not like a big factor. It might help a little bit.”

That is a pretty good description of the benefits — slightly smaller payments for a longer period of time — and it could certainly help some younger people get onto the property ladder and begin building equity in their home. But some napkin math reveals just how long that could take.

Home economics

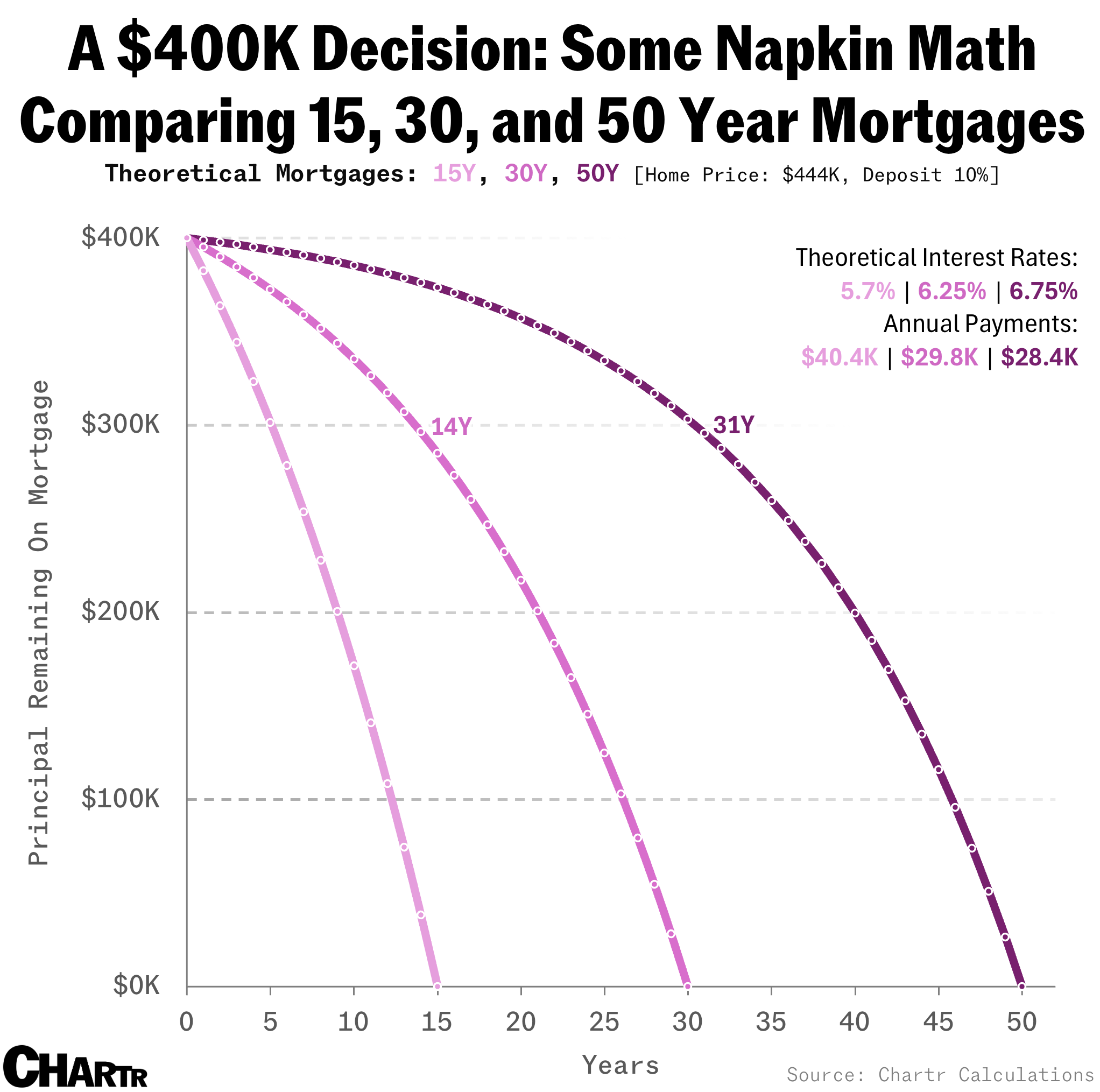

Let’s consider someone buying a home for $444,444, with a 10% deposit, leaving them borrowing a conveniently round $400,000. In this scenario, at current rates — about 6.25% for a 30-year fixed mortgage — it would take the individual about 14 years before they pay off the first $100,000 of the principal of the loan. The second $100,000 comes quicker, and the third and fourth even faster still, as the interest accrued each year on the outstanding debt falls.

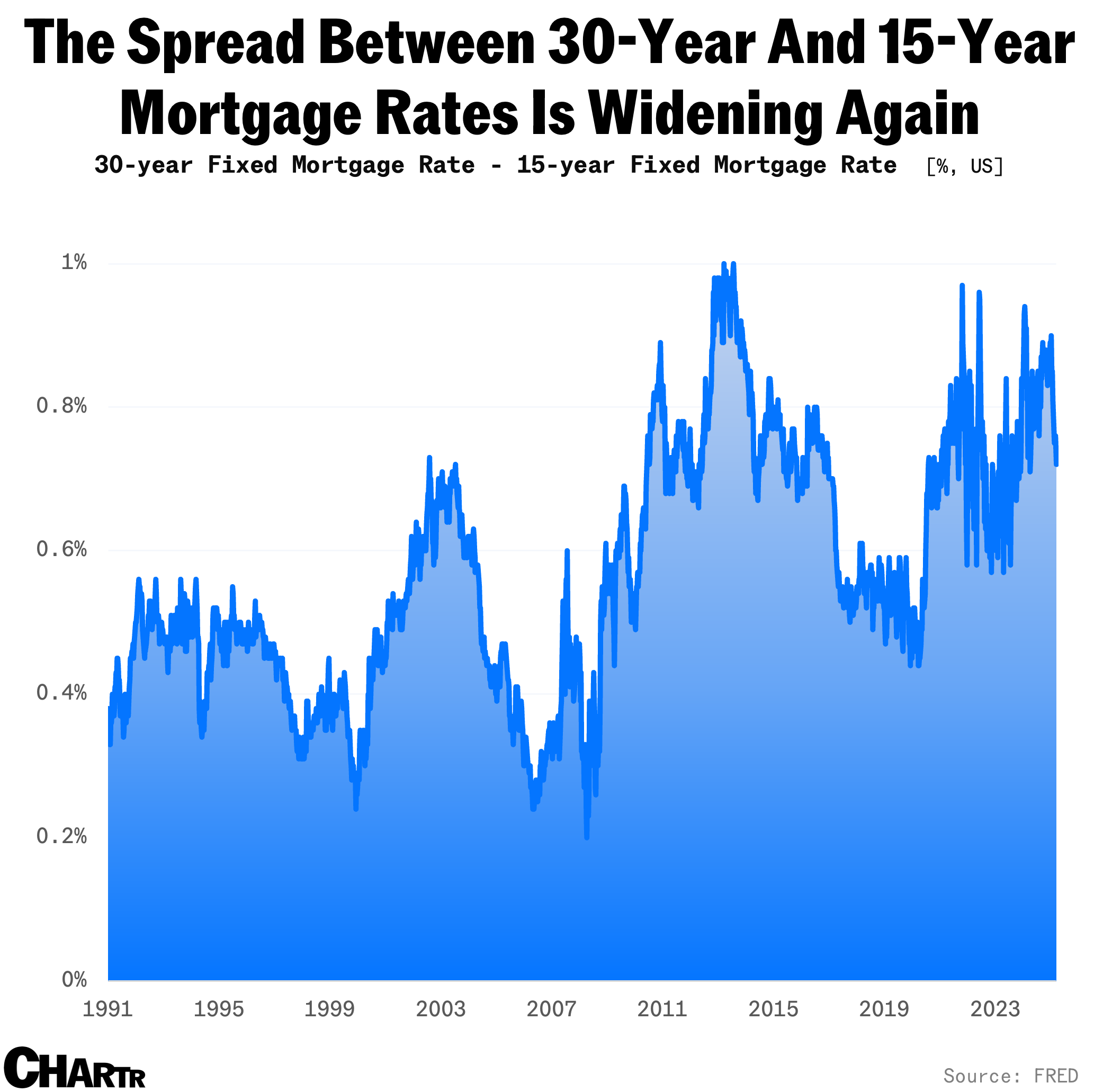

Now, let’s consider a theoretical 50-year mortgage and assume a very slightly higher interest rate, we’ll say 0.5% higher, as banks typically charge more interest for a longer loan — increasingly so, in fact, as data from Freddie Mac via FRED reveals.

With that shift in interest rate, we can see just how dramatically the math changes. Now it takes a whopping 31 years before the first $100,000 is paid off, with the bulk of the payments in the first decade just servicing the interest on the debt.

Better put, “extending a mortgage from 30 years to 50 years could double the (dollar) amount of interest paid by the homebuyer on a median-priced home over the life of the loan and significantly slow equity accumulation," per John Lovallo from UBS Securities.