Corporate breakups and spinoffs are back on Wall Street — but are investors up for the ride?

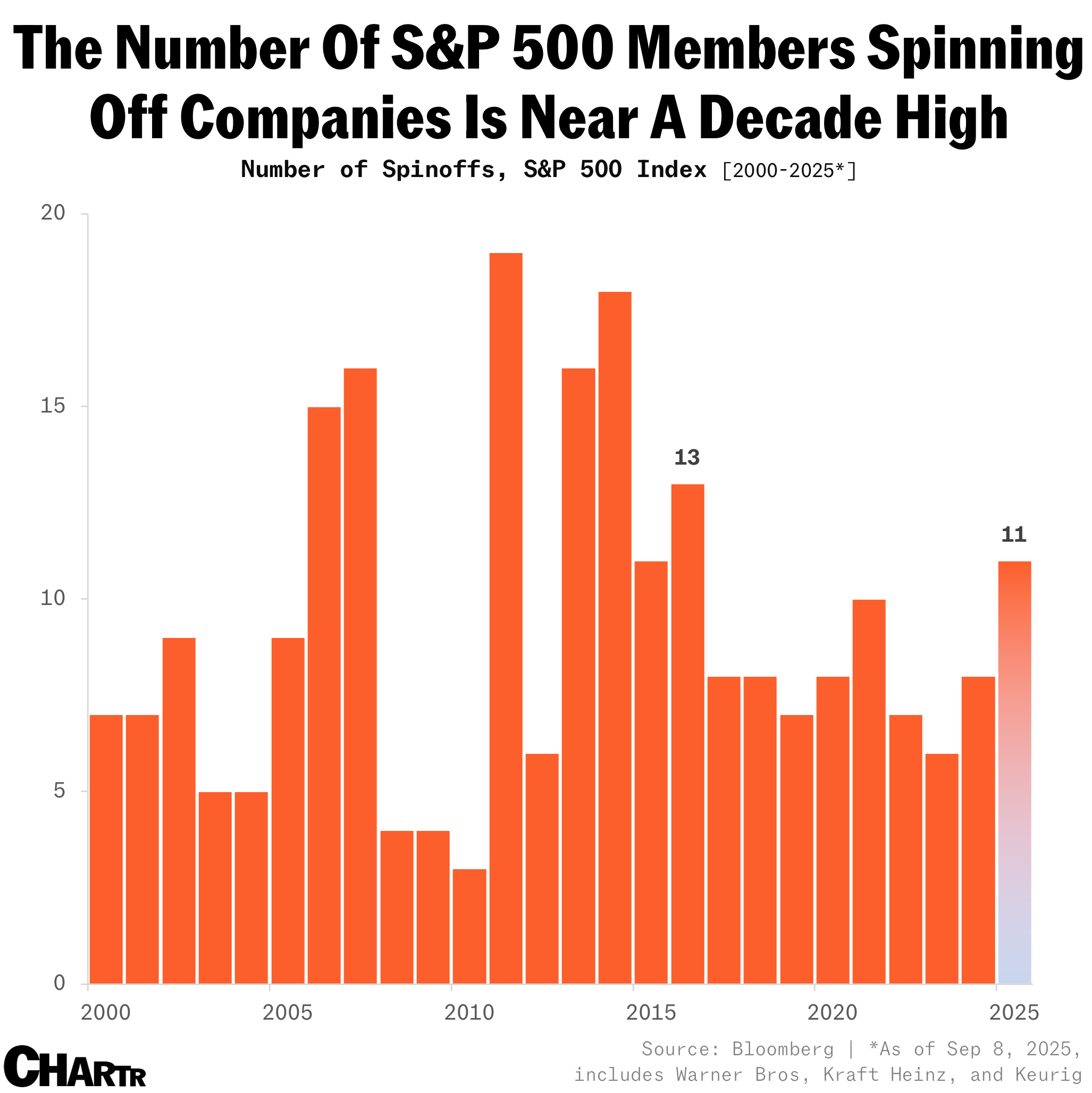

Spinoffs among S&P 500 companies are running at their fastest pace since 2016.

Bankers love to put companies together, pitching acquisitions all day long to corporate executives in the pursuit of scale, synergies, and seriously huge banking fees. But they also don’t mind doing the opposite. Indeed, Corporate America’s hottest new trend in dealmaking is breaking up.

Divide and conquer

So far this year, plenty of household names have opted to split themselves apart: industrial giant Honeywell is dividing into three, while Warner Bros. Discovery said in June it would separate its TV networks from streaming and studios. Keurig Dr Pepper plans to separate its soda and coffee businesses after completing its $18 billion acquisition of JDE Peet’s. And Kraft Heinz will spin off its grocery arm, shedding Kraft-branded staples like boxed mac and cheese and frozen meals.

What’s fueling this uncoupling, with some of them even undoing past megamergers? According to The Wall Street Journal, a big driver is activists pushing back against bloated empires. Their argument? Fast-growing divisions get dragged down by sluggish ones, and those much-hyped “synergies” from megamergers hardly show up.

Amid shareholders’ growing push for simplification, spinoffs have been growing in the US. As of early September, there have been 11 announced spinoffs from S&P 500 companies — the most since 2016.

But whether these corporate divorces actually pay off is another story. In the first 18 to 24 months following the split, companies spun off do tend to outperform the S&P 500 by ~10%, Trivariate Research found — but those early gains might not hold up over longer horizons.

Since its 2015 launch, the S&P US Spin-Off Index — which tracks S&P 500 companies worth over $1 billion spun off in the last four years — has lagged behind the main S&P 500 Index.

On the flip side, other research suggests the parent companies might fare better; a recent report from Ernst & Young and Goldman Sachs found that the share prices of parent companies tended to outperform their relevant indexes by 2.1% on the day of the announcement, and by “6% over the respective sector indexes for the period of two years post-close of transaction.” Cynically, though, the bankers pitching the corporate breakups usually don’t care much about what happens afterward — they make fees on the transaction either way.