DOWNWARD DOG

Lululemon

The brand helped create an entire genre of activewear... but now its competition is catching up

Sales are slowing, competition is rising, and LULU is one of the worst performing stocks in America this year

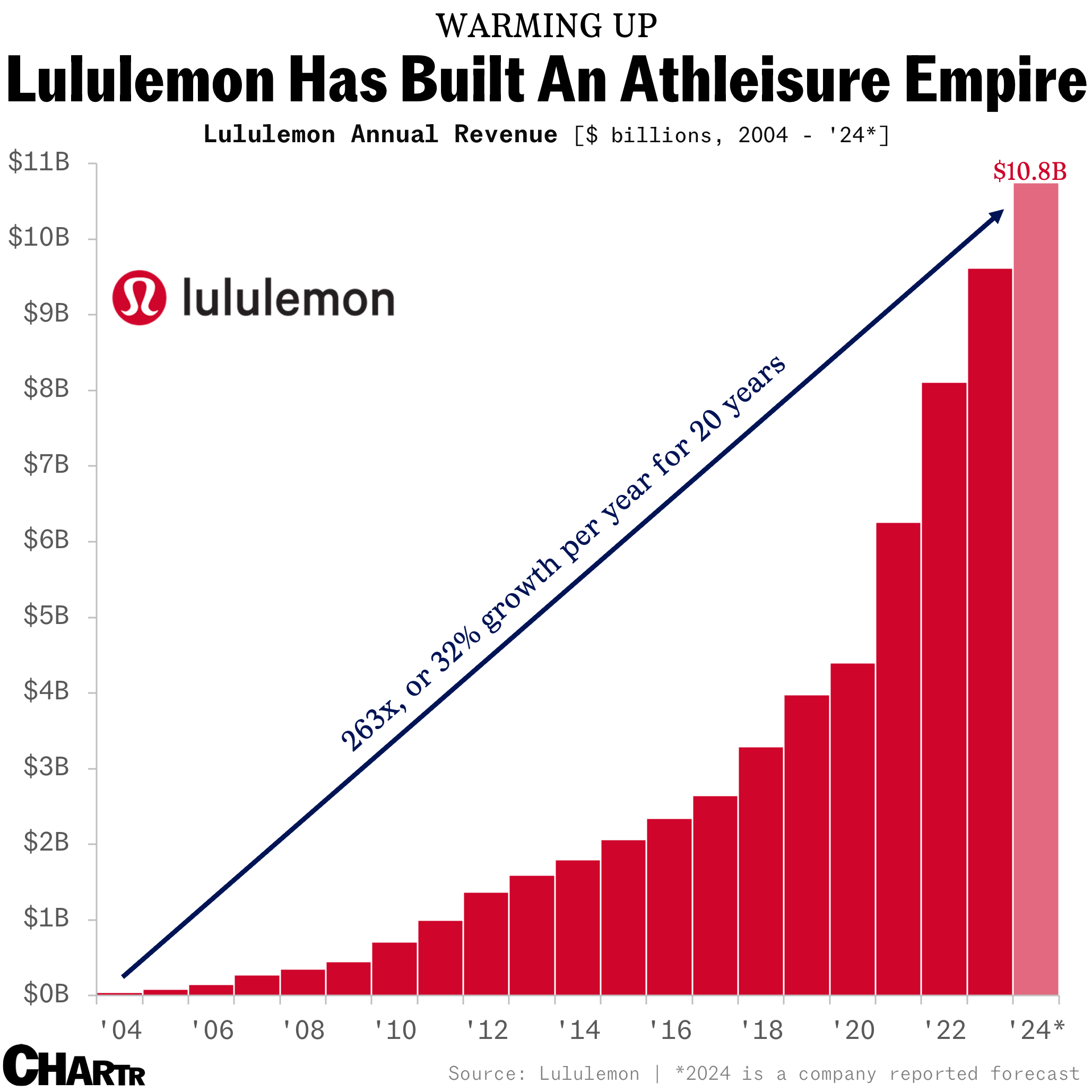

For some time, it seemed that buzzy athleisure brand Lululemon, which launched in 1998 as a small retailer selling yoga wear in a studio in Vancouver, was unstoppable. Through the intervening decades it’s flexed successes almost non-stop, from opening its first standalone store in 2000, to going public in 2007, to reaching $1B in annual revenue in 2011… before growing sales more than 5x in the following decade and announcing partnerships with the biggest names in the workout world like Barry’s and Peloton.

For anyone who’s visited a gym, yoga studio, or an office where employees value a comfort-yet-corp-friendly fit in their working lives, Lululemon has become almost impossible to avoid. But, after years of expansion, the company might finally be running out of new people to sell ~$100 pairs of yoga pants to.

Feeling the squeeze

In its most recent quarter, Lululemon’s sales growth tempered to just +10%. Since 2004 it had averaged more than 30%. Lululemon investors aren’t accustomed to that kind of cooldown, and it has weighed on the stock, which was the worst performing in the entire S&P 500 in the last week of May. At the time of writing it’s down nearly 40% for the year (currently making it the 3rd worst performer in the S&P 500) — so, why is LULU suddenly struggling?

The company’s results last week had some positives, but investors can’t seem to look past two things:

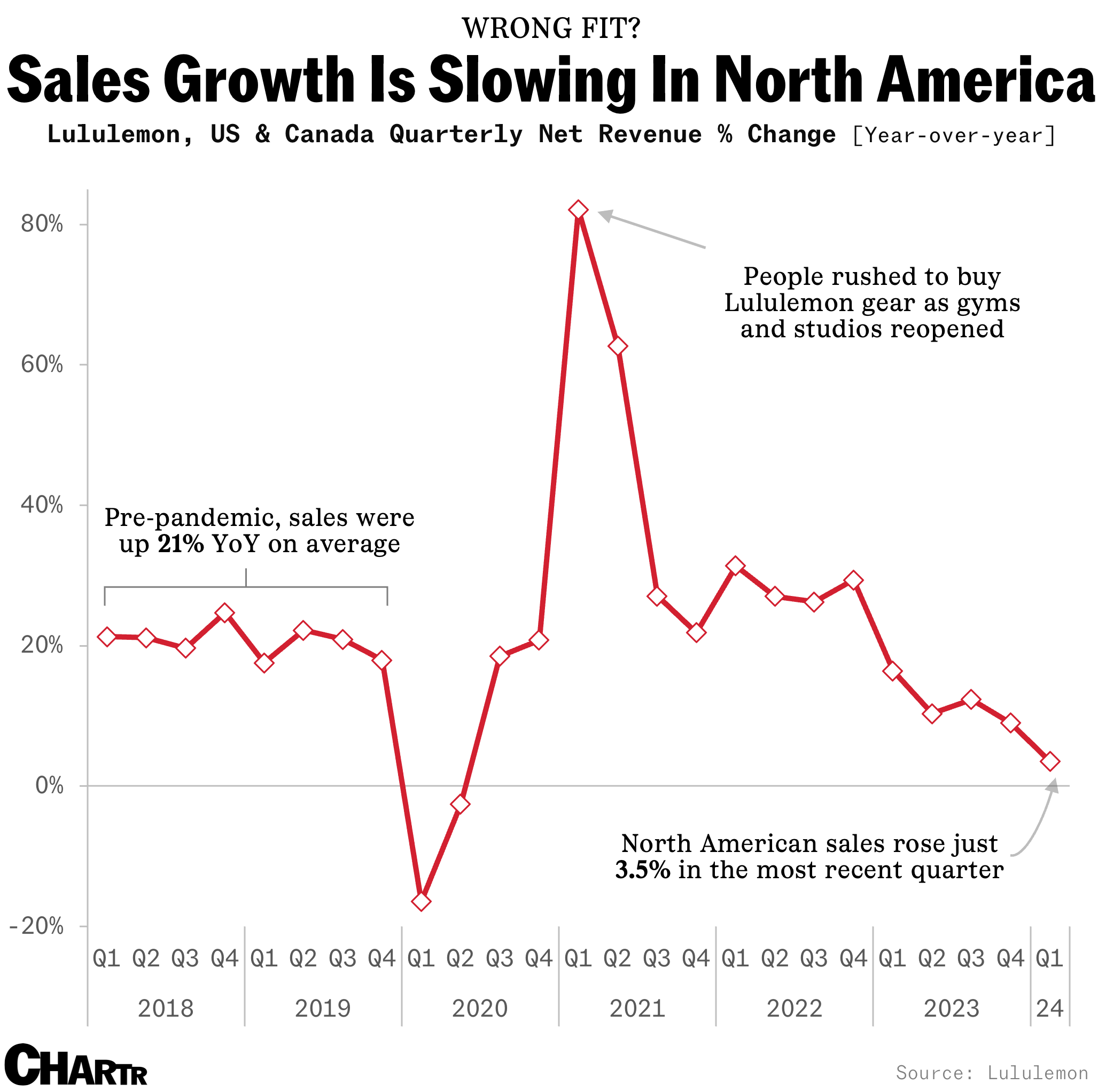

A serious slowdown in North America, the company’s biggest market (~80% of sales).

The departure of its Chief Product Officer who has been credited with driving product innovation since 2018.

Pre-pandemic LULU sales in the US & Canada were growing at a healthy clip of about 20% a year, as all of your fittest friends waxed loud and lyrical about the brand’s super comfortable leggings or surprisingly durable windbreakers. The pandemic turned the world upside down — which was bad (store and gym closures), then good (athleisure boom) for Lululemon — but since the world has gotten back to “normal” in the last couple of years, sales have been slowing, with North American revenue up less than 4% in the first quarter of 2024.

Lululemon said that it simply hasn't been stocking enough colors and sizes to cater to their youngest consumers as a major factor for recent sales figures. However, even 16 months ago analysts were wondering if there might be a more fundamental problem: that the Lululemon brand could now be saturated and at risk of “leading early adopters to new emerging brands”, per BMO Capital markets analyst Simeon Siegel.

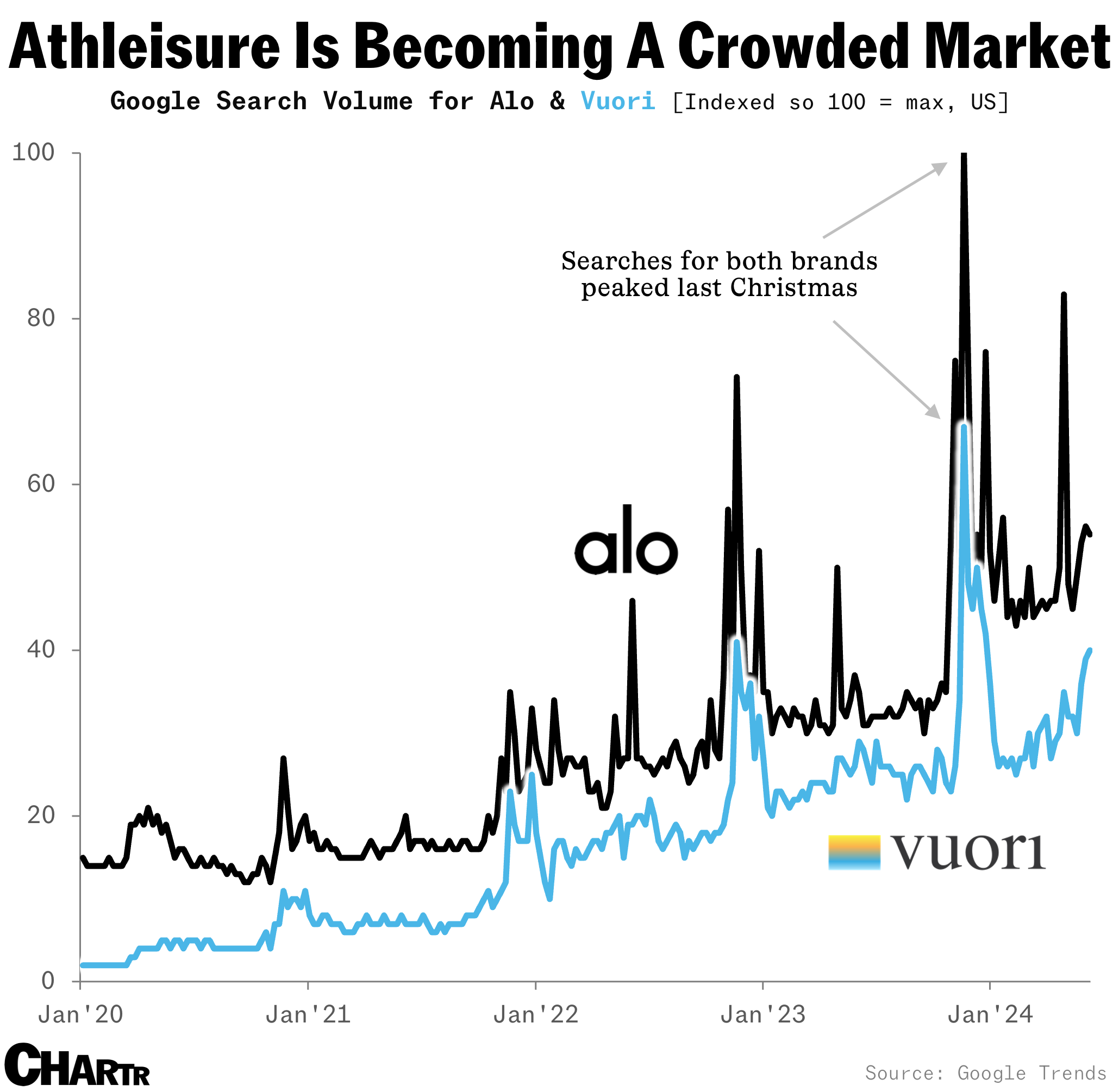

And if you want premium workout wear these days there are plenty of companies who’d like to meet you, as Lululemon’s impressive profitability has attracted competition — as Jeff Bezos once said: “your margin is my opportunity”. Two bougie activewear specialists in particular who are starting to threaten LULU’s rule are Alo Yoga and the more male-focused Vuori.

The 2 brands do look a lot like Lululemon, and not just in the wardrobe department: they too boast high quality cuts with high price tags to match; they too are sported on the streets by taste-makers and celebrities; and they too share a versatile appeal that spans a broad age spectrum. In addition, the companies, much like Lululemon before them, are both beginning to create a lot of online buzz, with Google searches for each brand peaking last December.

What’s more, Alo and Vuori are increasingly encroaching on Lululemon turf physically. Indeed, Bernstein analysis published by the Wall Street Journal found that a genuinely baffling 90% of Vuori stores operate within 0.5 miles of a LULU branch, while 84% of Alo’s shops are the same. Staggeringly, per the same data, if you’re in a Vuori store, you’re never more than a maximum of 5 miles away from a Lululemon.

Store wars

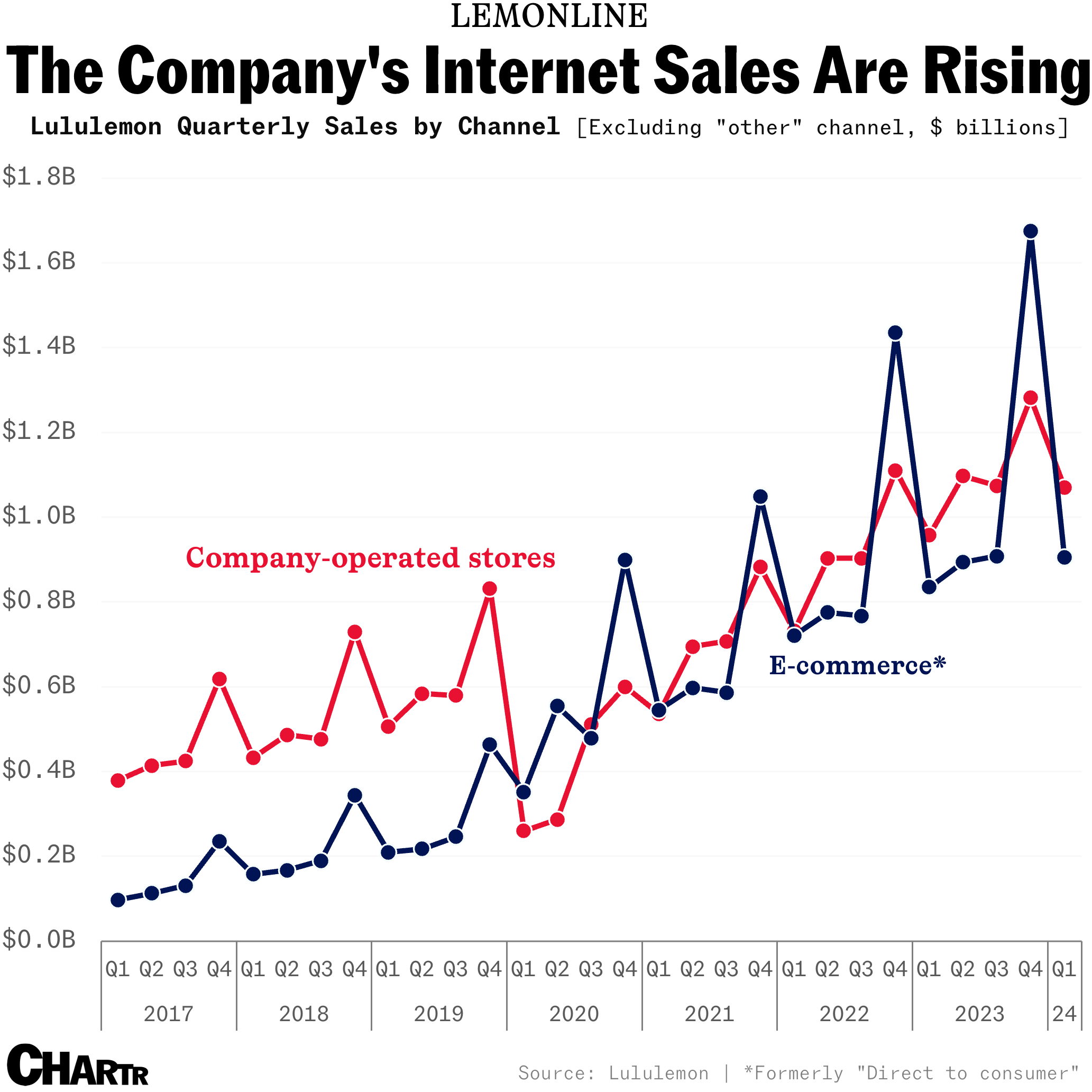

The good news for Lululemon, though, is that they aren’t nearly as reliant on their physical storefronts as they have been in the past: the company, which operates 700+ stores around the world, has built a thriving e-commerce presence to boot.

Of course, active apparel has always been a competitive industry, and Lululemon was essentially up against long-standing titans in the scene like Nike and Adidas from day 1. The company managed to carve out a niche in the industry, with a Retail Dive piece on LULU arguing that the brand didn’t just change activewear, but transformed apparel more generally by “introducing retail to athleisure”. Now, the plucky upstart has become the old hand fending off the young challengers.