The economics of $15 salads are improving, but Sweetgreen is still in the red

Sweetgreen narrowed its losses, raised its guidance, and sold a lot of steak salads in Q2

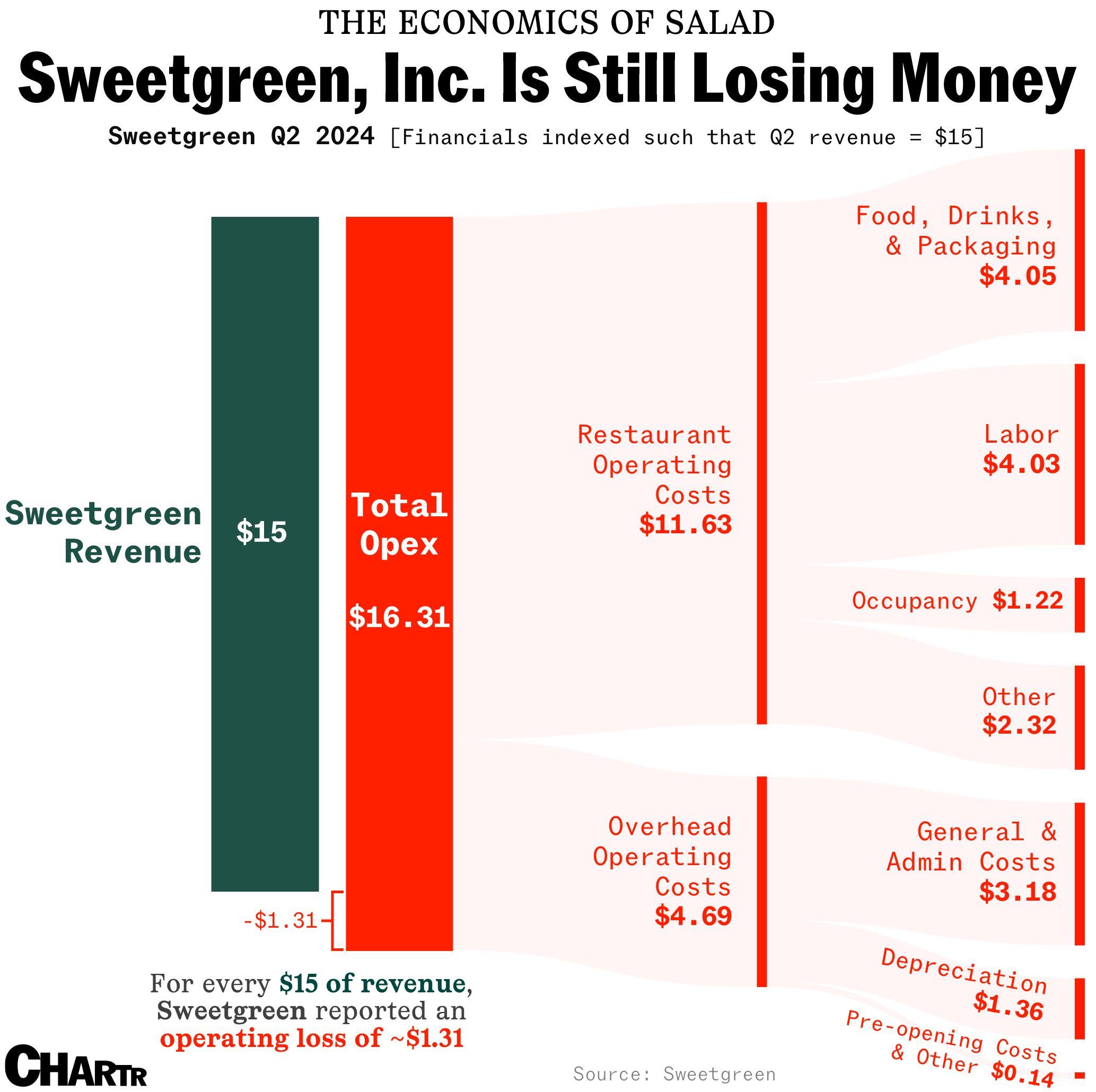

Sweetgreen reported nearly $185 million in Q2 sales of salads like the “Chicken Pesto Parm”, the “Shroomami”, and the “Kale Caesar”. But, as in the previous quarter, despite selling salads for $15, $16, or even $18... Sweetgreen is still not profitable.

We’ve indexed Sweetgreen’s earnings to $15 — roughly the price of a typical salad at the chain (although there’s a strong argument that $16 or $17 might be more appropriate) — to understand the latest in salad economics.

When we did this exercise in Q1, Sweetgreen was losing $2.56 for every $15 of revenue. Now, it’s losing just $1.31 for every $15 of sales.

The company’s core restaurant operations are, once again, nicely in the green with “restaurant-level” profit margins of some 22%, boosted in part by new menu items featuring lots of caramelized steak. But, once you account for all of the other overheads, the depreciation of its assets, some “pre-opening” and other costs (worth about 14 cents in our example), Sweetgreen is still in the red.

Romaine-ing calm

With a valuation of more than $3 billion, investors clearly expect the company to continue opening stores (it opened a net of 4 more in the latest quarter), growing sales, and expanding its margins. And a big part of the plan is automation, with robots able to dispense, mix, and serve salads at select locations — an innovation Sweetgreen calls the “Infinite Kitchen” (an unhelpful name because what exactly is “infinite” is unclear... the amount of salad, the amount of kitchen... or something else?).

On a call with analysts yesterday, Sweetgreen’s CEO said they expect that “more than 50% of new units would include Infinite Kitchen next year”. At Naperville, an Infinite Kitchen restaurant that just crossed its one-year anniversary, the restaurant level margin was more than 31%, considerably higher than the company’s average.