The New York Times didn’t get as much of a “Trump bump” as investors wanted

Last time around, newspapers got a big boost from nonstop Trump coverage.

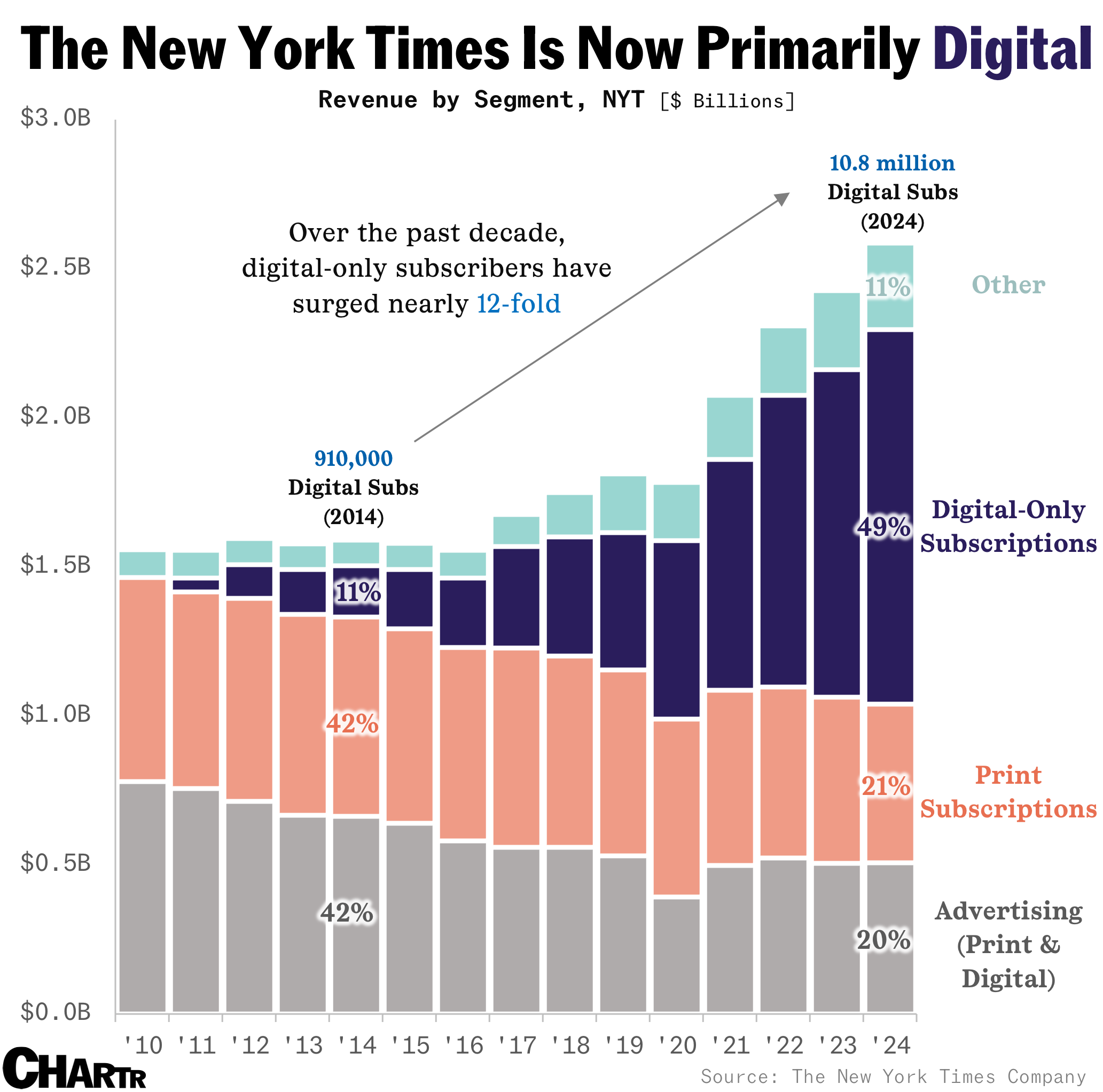

On Wednesday, The New York Times Company reported that it had gained another 350,000 digital-only subscribers in the last quarter. That pushed the NYT’s total subscriber count to more than 11.4 million, maintaining its crown as the world’s largest news company to have successfully pivoted away from its print media roots. Indeed, just 21% of the company’s revenue came from print subscriptions last year, half the proportion from just a decade ago, as the newspaper’s push into games, cooking, and product recommendations has broadened its appeal. As one Sherwood writer summarized last year: “The New York Times is a games company with a newspaper side hustle.” The company also hiked its dividend by 38%.

(Hard) Times

On the surface, that sounds... good? Except that investors in The New York Times have become accustomed to quarter after quarter of strong digital growth and the company’s guidance for the coming year left traders unimpressed, with NYT shares falling a whopping 12% in Wednesday trading as investors digested the disappointing forecasts.

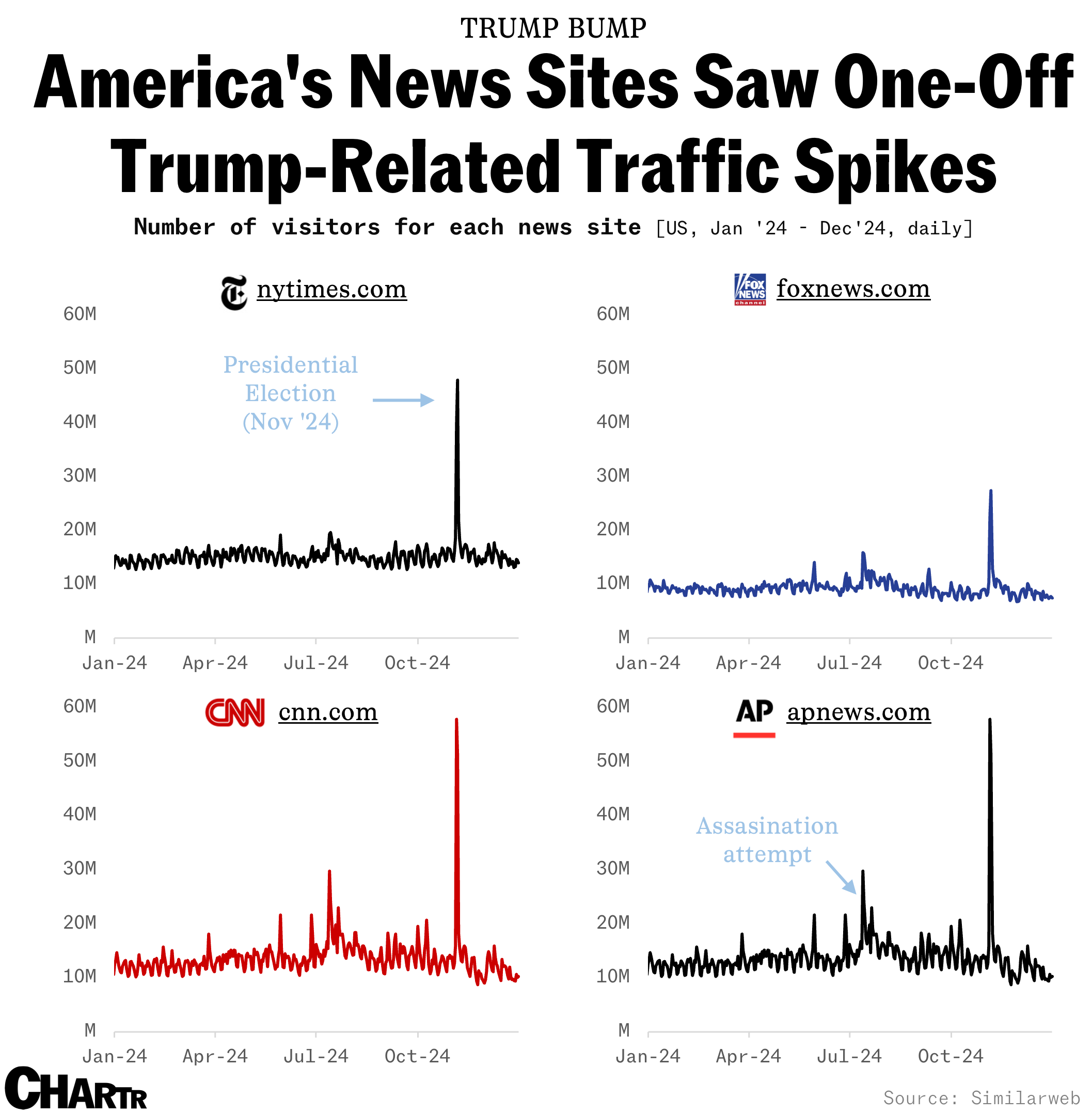

Of particular note was that the Q4 “Trump bump” didn’t materialize as much as NYT execs might have hoped.

In 2016, following Donald Trump’s remarkable ascension to the White House, the news media industry enjoyed bumper traffic and heightened interest in politics as President Trump enacted his MAGA agenda. Many expected that phenomenon to happen again. And, in terms of pure traffic, it briefly did: data from Similarweb reveals a sharp spikes in daily visitors to some of the nation’s most popular news sites around the election.

So far, however, the election has yet to translate into a sustained news media boom. Editors and execs have only enjoyed a truncated “Trump bump,” as it were.

In defense of The New York Times, the company itself ran an article on the subject in the wake of the election, pouring some cold water on the expectation that Trump 2024 would be like Trump 2016: “News fatigue and changing consumption habits could sap some of that enthusiasm over time, several news media experts said.”