Bitcoin faces not only short-term risks but a lack of catalysts for a turnaround

Bitcoin continues to plunge, hitting lows not seen since October 2024.

Bitcoin is having a rough start to the new year, falling below $67,000 early Thursday morning, its lowest level since October 2024.

It’s down 23% over the past week and ~46% from its October 6 all-time high. The post-election euphoria has faded, much-awaited crypto regulation is stalling, and the “Trump bump” is no more. Bitcoin’s historic first-quarter average return stands at 46.41%. But so far in 2026, it’s down more than 20%, CoinGlass data shows. And on Wednesday, Stifel analysts said the trend would suggest "a potential low of $38,000," according to a note.

A new CryptoQuant report shows that on-chain indicators confirm a bear market regime, one worse than in 2022, with institutional demand reversing, spot demand remaining weak, and liquidity conditions tightening.

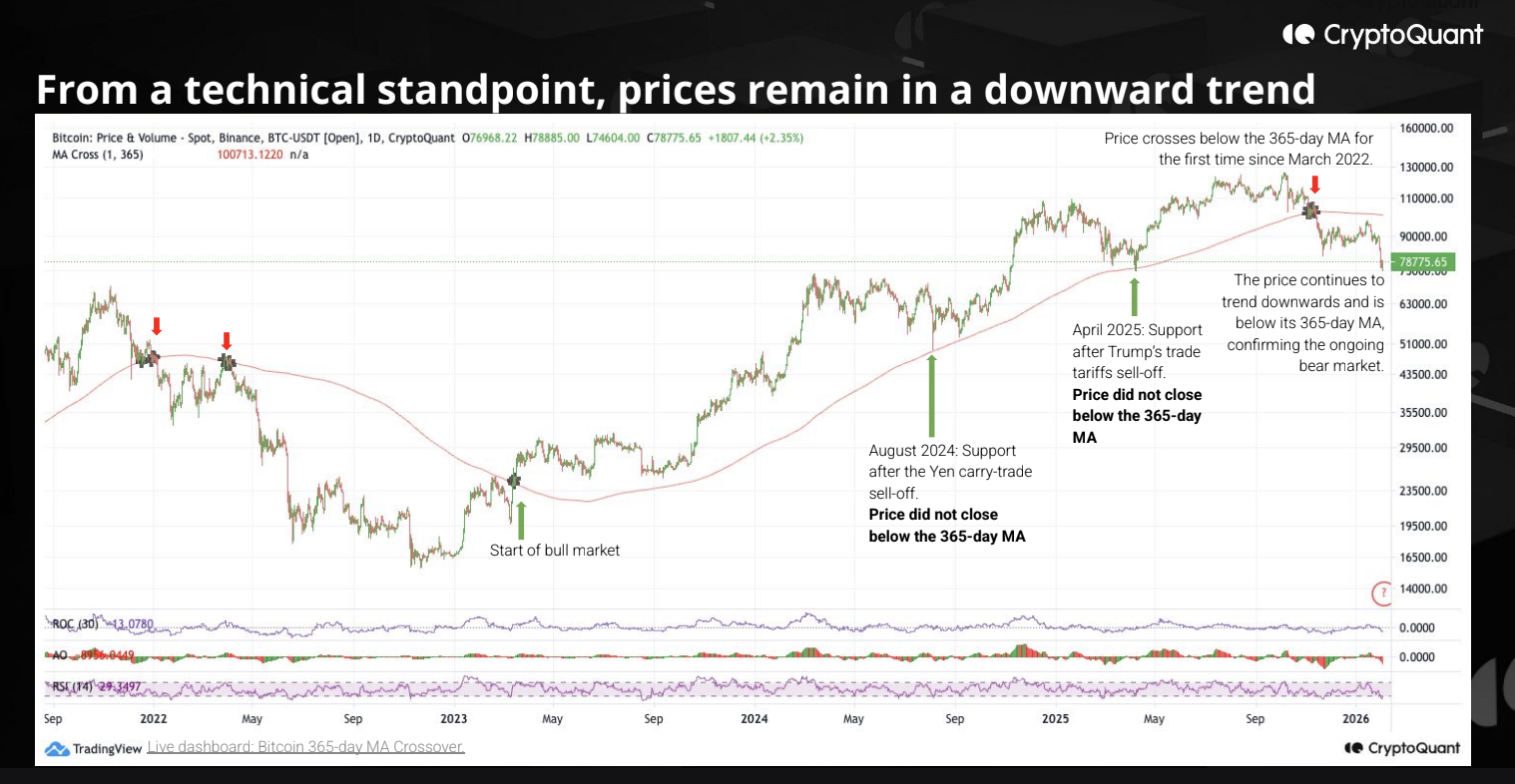

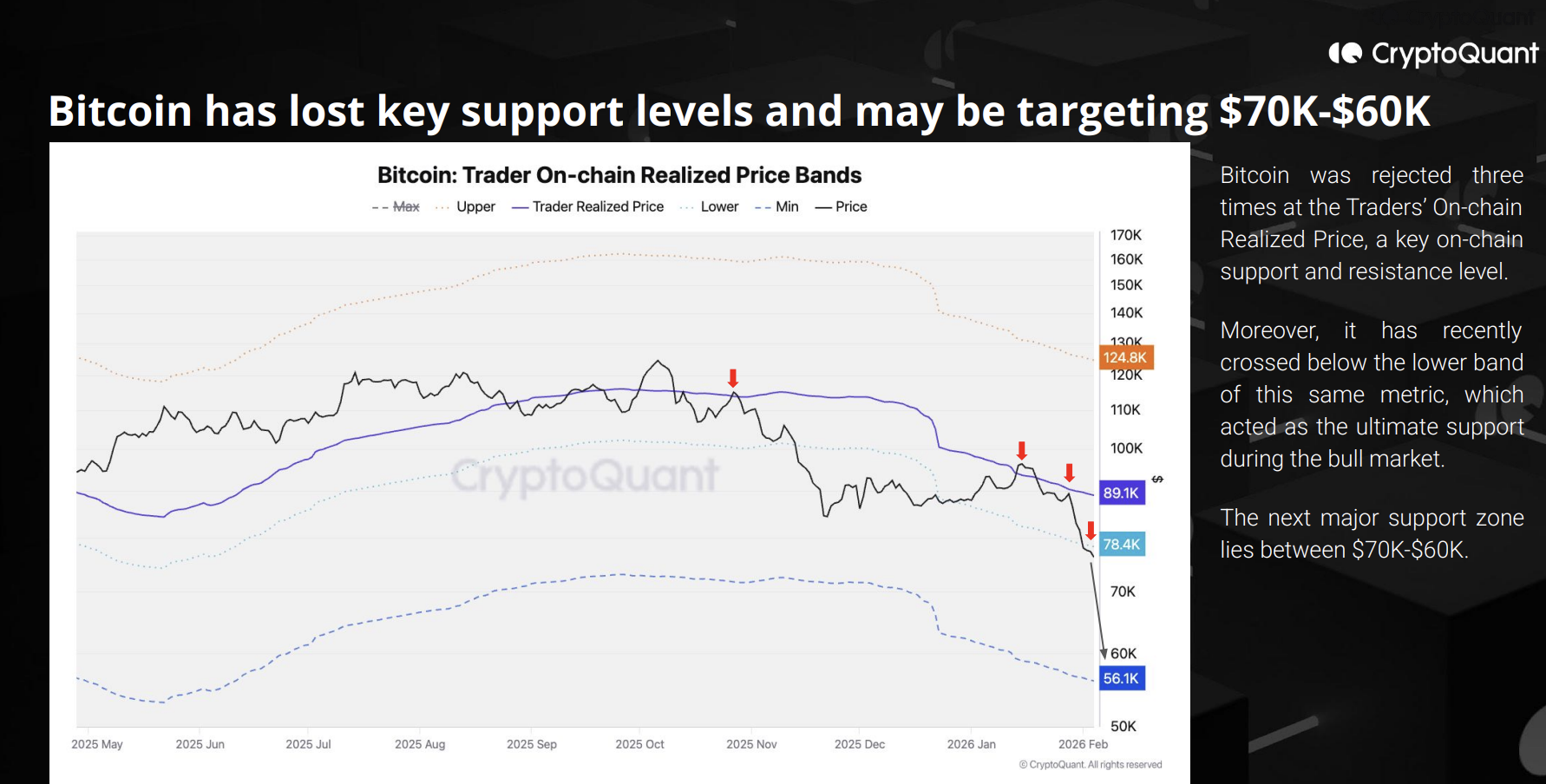

“Bitcoin has broken below its 365-day moving average for the first time since March 2022 and has declined 23% in the 83 days since the breakdown — worse than the early 2022 bear phase. The loss of key on-chain support levels suggests potential downside toward the $70K–$60K range,” the analysts wrote in the report.

A February 4 Glassnode report, “Bears in Control,” notes that “spot BTC volumes remain structurally weak, with the 30D average still depressed despite BTC rolling over from $98K to $72K. This reflects a demand vacuum, where sell-side pressure isn’t being met by sustained absorption.”

Nic Puckrin, cofounder of Coin Bureau, told Sherwood News that bitcoin is in “full capitulation mode,” as it slides below the psychological barrier of $70,000.

He said that this is no longer a short-term correction, but rather a transition from distribution to reset — and these typically take months, not weeks.

“At this point, if bitcoin fails to defend the $70,000 threshold, it could be heading for its bear market low around $55,700-$58,200,” Puckrin said.

The asset is facing several headwinds, at least in the short term. In addition to the geopolitical and macro risks, “old” (relatively speaking; bitcoin is only 17) bullish catalysts and narratives no longer seem to hold.

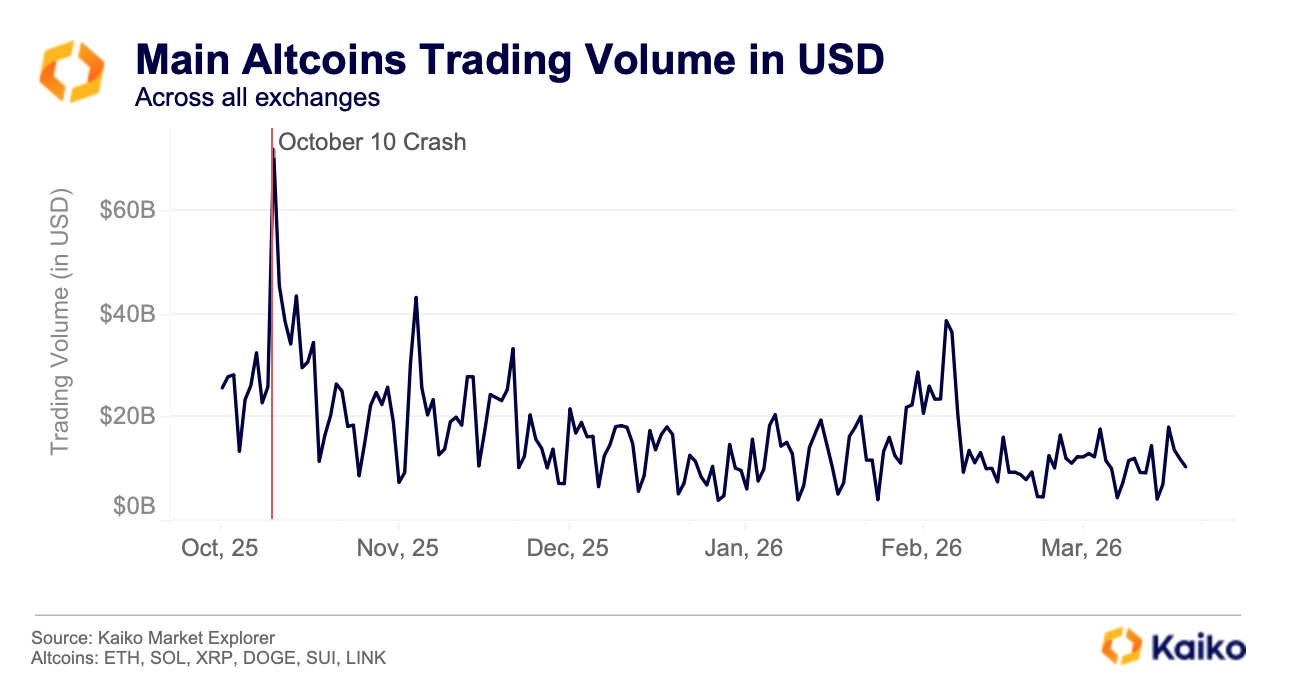

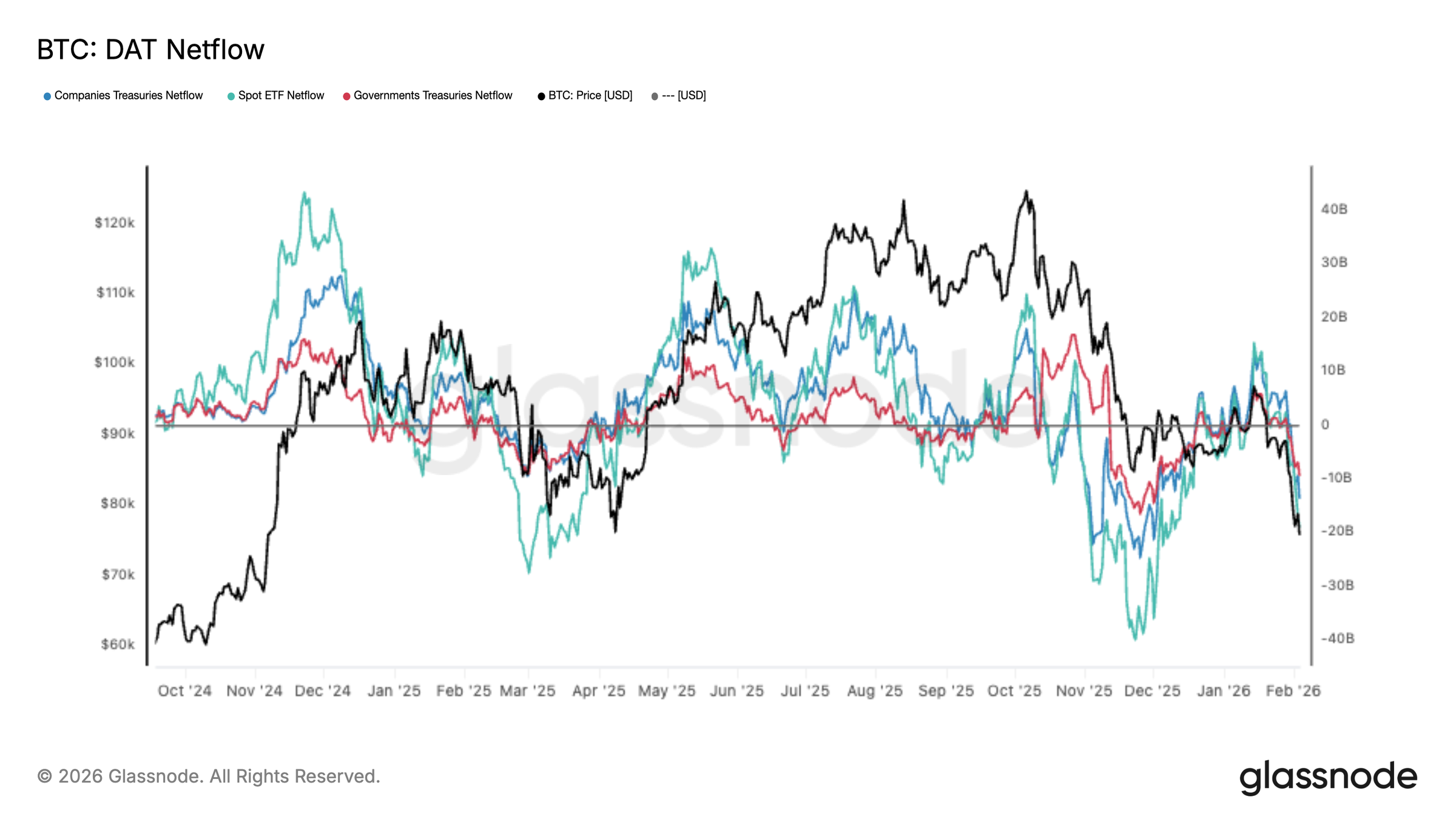

The explosion of digital asset treasuries adds a new risk to the equation. Many are under pressure and might be forced to sell their bitcoin holdings. The October 10 massive $19.1 billion liquidation event is still weighing on bitcoin.

An emerging risk is the lack of fresh catalysts for a sustained bitcoin rally to revive the asset.

Macro and geopolitical risks

David Siemer, CEO of Wave Digital Assets, told Sherwood that in the short term, risks include equity markets near all-time highs, price-to-earnings ratios remaining elevated, and signs of an economic slowdown in the US and globally, including weakening labor markets.

“In the face of a potential AI bubble, if the NASDAQ dropped 15% over the next year, BTC would probably drop 30%,” Siemer said. “It’s probably going to take 3 to 6 months before we see any turnaround. Things always happen fast in crypto, but there are relatively few near-term catalysts that would allow bitcoin to decouple from broader risk sentiment.”

There could also be more trade tariffs or geopolitical escalations, which could further dampen risk appetite and put more pressure on bitcoin.

From digital gold to the four-year cycle to the debasement trade, these bitcoin drivers haven’t held up so far this year — case in point: the recent precious metals rally, which bitcoin failed to replicate.

Regulations, or lack thereof

Juan Leon, senior investment strategist at Bitwise, said that regulatory uncertainty over the CLARITY Act also plays a significant role, as it is critical to continued institutional adoption.

“It faced setbacks in January, and if negotiations drag on without progress, uncertainty will rise, and investor sentiment could become more skittish,” he said.

Citi analysts said in a February 4 note that while they view legislation as a potential catalyst for a change in sentiment, Senate negotiations have slowed.

In addition to helping investor sentiment, the regulatory backdrop could also be a key catalyst for ETF flows, which have been lackluster since the start of the year.

“If history is any guide... the election (Nov 24) and US Genius act passage (July 25) saw increased ETF inflows,” the analysts wrote.

The “Warsh effect”

President Trump’s nomination of Kevin Warsh as the next Fed chair has been a negative catalyst, according to several experts.

Aurelie Barthere, principal research analyst at Nansen, said that Warsh’s main ideological purpose is to restore the Fed to its minimum role of manipulating the duration of the average maturity of the Fed’s reserve assets through its balance sheet only during economic crises, rather than intervening in financial markets through a large balance sheet.

“Changing the Fed’s operating regime and reducing the balance sheet will not be straightforward (the Committee needs to be convinced), but I think markets are starting to price in a small probability of QT resumption. This is bearish crypto,” she said.

Digital asset treasuries, aka DATs

Last year was the year of DATs, a phenomenon Strategy pioneered that was then copied by many. The corporate pivot to bitcoin isn’t looking great right now: as of writing, every one of the major players are underwater (including Strategy). The top 100 public bitcoin treasuries hold 1.13 million bitcoin collectively, 713,502 of which are held by Strategy, Bitcoin Treasuries data shows.

Justin D’Anethan, head of research at Arctic Digital, told Sherwood that a major, under-discussed risk is the potential unwind of DATs.

“I’m not thinking Strategy specifically; I actually think it will be fine. I worry about smaller players with less history, conviction, and different structures,” he said.

D’Anethan said many hold large BTC stacks and have traded at discounts relative to mNAV, or market-adjusted net asset value. If those collapse further and they can’t raise fresh capital, forced selling of BTC could accelerate the downside.

Searching for any catalysts

At this point, to see a move higher, there would need to be a liquidity catalyst of some sort — either in the form of a monetary policy pivot or more meaningful institutional allocation, Coin Bureau’s Puckrin told Sherwood.

“What we will likely see, however, is a continuation of the trend we’ve witnessed over recent months, where bitcoin has been shifting from a high-beta venture asset to an institutional balance-sheet play, which means lower volatility but fewer short-term upswings,” he said.

“In the short term, a rally on lower volume would likely only set the stage for a further correction, with support sitting at the macro 50% level of $70,900,” Puckrin said.

Conversely, he added that there are many resistance levels to the upside if bitcoin moves higher, including $86,000, $92,000, and $103,000 if it were to break the $100,000 barrier again. “Though this is unlikely in the short term,” he said.

Vasily Shilov, CBDO at SwapSpace, said that over the next few months, bitcoin will remain largely “hostage to macro headlines,” and for BTC to move into a durable uptrend, the market would need something concrete.

“Not speculation, but clearer signs that the Fed is preparing to ease, a rebound in ETF inflows, and tangible progress around a US strategic bitcoin reserve,” Shilov said.

Shilov added that this time “feels different.”

“The macro backdrop is tighter, geopolitical risks are higher, and real spot buying is thinner — all signs that the market has shifted into a more defensive mode rather than a temporary slowdown,” he said.