Legendary short seller James Chanos on the problem with Strategy’s business model

The noise has grown louder about Strategy being in trouble, but most experts think Strategy can weather the current bitcoin downturn, though one critic predicts this is “the beginning of the end.”

The proliferation of digital asset treasuries has been 2025’s crypto trademark event, a phenomenon pioneered by Strategy, the largest corporate bitcoin holder, with 650,000 bitcoin.

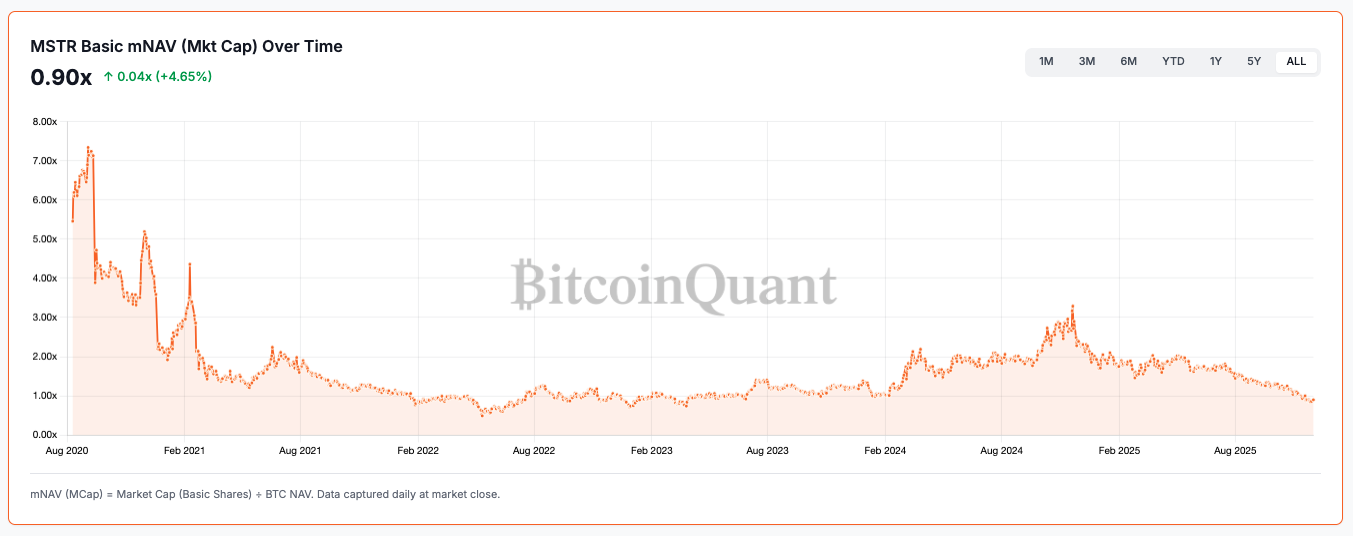

But cracks in the DAT business model have begun to surface, with several now trading below their crypto holdings, identified when a measure known as “mNAV” falls below 1. The metric mNAV, or market to net asset value, is a company’s market cap divided by the value of bitcoin it holds. It tells investors if the company is trading at a discount or a premium.

“In other words, it measures how much the market is valuing the company relative to the value of its bitcoin holdings,” per Bitcoin Treasuries.

The noise around Strategy being in trouble or even “doomed” has been growing louder, as its mNAV has compressed to levels reminiscent of 2022’s crypto winter. To put this in context, since the start of Strategy’s “Bitcoin Standard Era,” the historical high mNAV was 7.34x on September 3, 2020, while its historical low was 0.49x on May 12, 2022, according to data provided to Sherwood News by BitcoinQuant.

Some critics say the company is only a leveraged bitcoin bet, set to collapse along with bitcoin’s price. Shares of Strategy, which has never sold a single token since it began accumulating bitcoin in August 2020, are down 55% over the past year.

The underlying issues of Strategy’s strategy

Legendary short seller James Chanos, known for predicting Enron’s collapse, has called the entire DAT business model “silly.” Chanos, who unwound his “very profitable” short Strategy/long bitcoin trade in November, told Sherwood that it’s “not that complicated.”

“If you’re an investor, buy bitcoin directly, not through an intermediary. It’s silly. Our core thesis from the beginning — and it’s still our core thesis — is don’t pay more than $1 for something worth $1,” he said in a phone interview.

Chanos added that he never bought into the argument for issuing debt or preferreds to buy bitcoin, as “it doesn’t add value; it adds leverage.” As for why he closed the trade, Chanos said he wanted to leave “the last part of the compression to somebody else.”

The problem with Strategy’s business model is that Saylor raises outside capital when bitcoin is rising, but nobody wants to give him money when bitcoin is down, he said.

“The same thing happened in 2022: they didn’t buy much when bitcoin price collapsed,” he said.

Longtime bitcoin skeptic and Strategy doomsayer Peter Schiff goes a step further, calling the company “a fraud” that will “go bankrupt.”

When asked whether he agrees with Schiff, Chanos said he is “not that bearish.”

“Strategy is pretty transparent about what they’re doing. They have weekly disclosures, you can evaluate it, and I don’t see financial distress here. The software business breaks even, and they can always sell equities to make dividend payments on preferreds.”

What he questions, however, is why people are buying the securities.

“More power to Saylor to sell that stuff,” he said.

It’s not about levels, it’s about debt

On December 1, Strategy announced the creation of a $1.44 billion reserve “to support the payment of dividends on its preferred stock and interest on its outstanding indebtedness.”

Saylor said the move “marks the next step in our evolution” and will better position the company “to navigate short-term market volatility,” according to a press release.

In the accompanying December investor presentation, the company said its plan to fund the reserve includes issuing common equity if it trades above 1x mNAV and selling bitcoin or bitcoin derivatives if it trades below.

Many see the move as a way to assuage investors’ concerns around the maturity of its debt, which could become more problematic than the company’s mNAV level.

Tim Kotzman, founder of Bitcoin Treasuries Media, told Sherwood the reserve reduces near-term pressure on its balance sheet.

“Practically, it implies they don’t need to liquidate BTC to meet payments, reinforcing the idea that their bitcoin position remains long-term. It signals stability to rating agencies and shareholders while keeping their bitcoin stack intact,” he said.

Yet for Schiff, this new turn of events heralds “the beginning of the end” for Strategy, demonstrating that Saylor is “the biggest con man on Wall Street.”

Mark Palmer, an analyst at Benchmark, told Sherwood that calling Strategy doomed because of a single leg down in bitcoin’s price is like calling a 30-year mortgage insolvent because interest rates spiked for a quarter.

“Strategy is not levered to bitcoin’s price in the fragile way implied by its detractors, as its balance sheet was designed to absorb volatility across bitcoin price cycles,” he said.

The company has $8.2 billion in debt across six convertible bond issues.

“As such, its total annual interest expense is about $778 million, and its total debt as a percentage of its bitcoin holdings’ value of $57.6 billion is just 14%. These figures demonstrate just how resilient Strategy’s capital structure is, and the large amount of cushion it has against a decline in bitcoin’s price,” Palmer said.

Kotzman echoed the sentiment, saying that there isn’t a single bitcoin price that could force a liquidation, especially since the company repaid its only loan with explicit margin-call risk. The bigger risk, he said, would be a prolonged, deep decline in bitcoin that impairs the company’s ability to refinance upcoming debt.

“In that scenario, the company would likely raise equity before selling BTC,” he said.

Per Chanos, barring a complete collapse of bitcoin, there is not a specific level at which Saylor would be forced to sell bitcoin.

“But anything can happen. He’s changed his mind before,” he said.

Is there a “breaking point” in bitcoin’s price or mNAV for Strategy?

As for the company’s mNAV, dipping below 1 doesn’t mean Strategy is “doomed.”

CryptoQuant Head of Research Julio Moreno told Sherwood that it traded below 1x mNAV in the bear market of 2022, and the company wasn’t in financial danger. What it does mean, Moreno said, is that the company has less power to buy bitcoin by issuing MSTR shares, as it would be selling the shares at a discount to the value of its bitcoin holdings.

He also said the risk is more related to MSTR needing to pay about $700 million in dividends per year due to its preferred stock offerings.

Nic Puckrin, cofounder of Coin Bureau, told Sherwood, “Any panic is very much premature and unwarranted. Strategy is feeling the pain of the bitcoin sell-off, but it doesn’t change the fundamentals. It’s in a far more sound position than other bitcoin treasuries.”

Finally, another factor is the drop in sentiment — reflected in Strategy’s tumbling stock price, which could become a self-fulfilling prophecy, Puckrin said, adding, however, that structurally, the company can ride this roller coaster in relative comfort for a while.

“When bitcoin falters, everyone immediately turns on Saylor and calls the imminent demise of Strategy, but in reality, things aren’t quite so dire. Bitcoin hasn’t even fallen to Strategy’s average bitcoin purchase price yet, which is $74,400 — at which point it would be at an overall loss on its BTC purchases,” he said.

Sherwood News reached out to Strategy but hasn’t heard back at the time of publication.