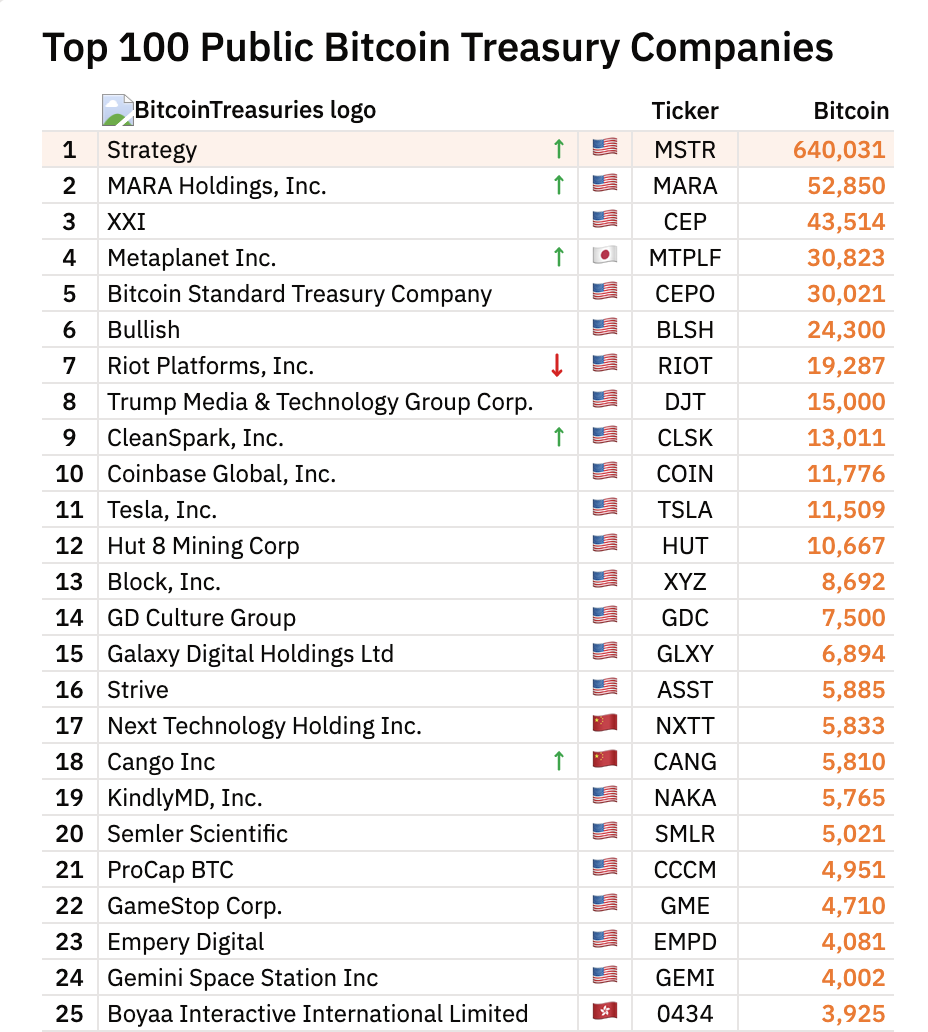

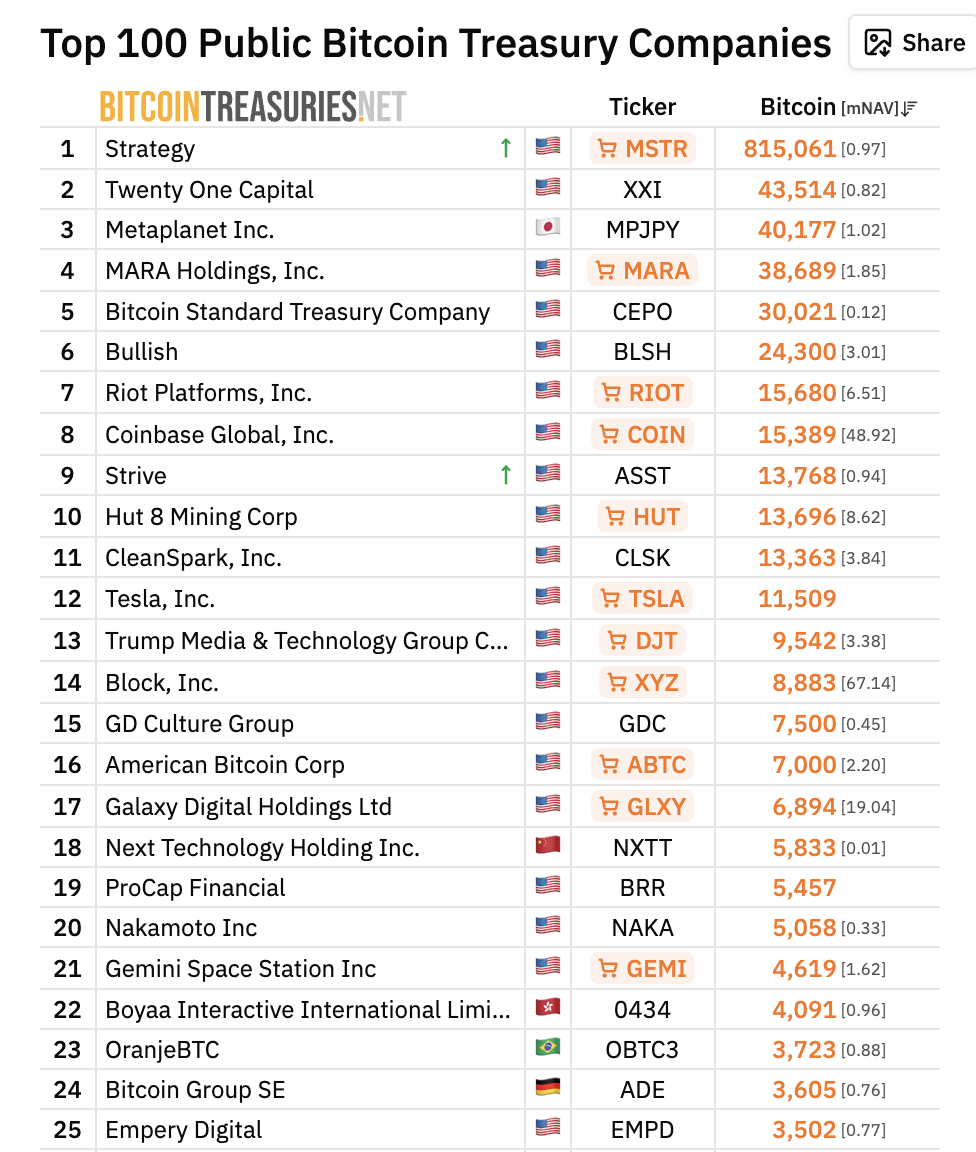

Strategy overtakes BlackRock in bitcoin holdings as digital treasury landscape weakens

With its latest acquisition of 34,164 bitcoin, Strategy now holds 815,061 bitcoin — about 4% of the total bitcoin supply.

The landscape of digital asset treasury (DAT) companies has changed almost as rapidly as its explosive ascent last year, and cracks have begun to show in this ecosystem, with many participants on life support.

As bitcoin’s price tumbled, some DATs have sold off their bitcoin holdings to prop up their operations, trading at discounts relative to their mNAV (which is a company’s market cap divided by the value of its crypto asset holdings) and sliding down the bitcoin stockpile leaderboard along the way.

One thing hasn’t changed, however: Strategy remains the leader of the pack. And today, the largest corporate bitcoin holder overtook BlackRock’s iShares Bitcoin Trust in holdings.

With its latest acquisition of 34,164 bitcoin, Strategy now holds 815,061 bitcoin, about 4% of the total bitcoin supply. In contrast, IBIT, the most successful bitcoin ETF, with $64.63 billion in assets under management, holds 802,823 bitcoin.

This marks the company’s third-largest acquisition since it started accumulating bitcoin in August 2020, and the largest since November 2024. It’s on track to reach 1 million bitcoin by November, according to Bitcoin Treasuries.

Daniel Bara, director of the Olympus Association, told Sherwood News that while this is a leaderboard milestone, “I would not call it a watershed in any structural sense.”

“Strategy overtaking IBIT is a function of its equity issuance outpacing IBIT’s inflows, and both can reverse. IBIT had over $8 billion in net inflows in Q1 even as BTC fell roughly 20% over the quarter, so the demand for ETF exposure is intact,” he said.

Last week, bitcoin ETFs recorded $996.38 million in inflows, their largest weekly inflow since the week of January 15, per SoSoValue, underscoring renewed institutional interest.

For its latest bitcoin acquisitions, Strategy used proceeds from its STRC and STRK stock offerings (launched in July 2025 and January 2026, respectively), enabling the company to maintain its acquisition pace despite bitcoin’s tumble.

But as Ishmael Asad, a research analyst at Bitwise, noted, STRC’s growth has been sudden and increases dependence on bitcoin price appreciation over shorter time horizons as the company’s dividend obligation expands.

“As Strategy and other DATs continue accumulating, this could become a growing risk if the market does not see meaningful appreciation any time soon,” Asad said.

Strategy’s mammoth stash also brings another issue to the forefront: its concentration of holdings.

“Michael Saylor now has the power to affect the price of BTC simply by pausing purchases. Unlike ETFs, which are passive vehicles, MSTR and other DATs are active buyers of bitcoin. This makes them far more influential in setting marginal demand,” Nic Puckrin, cofounder of Coin Bureau, told Sherwood.

DATs the problem?

On a broader level, the fragility of the DAT model is becoming increasingly apparent, and as firms stop HODLing, it could put further pressure on bitcoin.

In March, Nakamoto — which has failed to rise above $1 a share since getting a delisting warning in December — sold 284 bitcoin for $20 million, at $70,422, a 40% cut from its $118,171 average cost. The company is hoping a reverse stock split will boost its stock, which is down 30% year to date.

MARA Holdings, which was once the second-largest bitcoin holder, announced last month that it sold 15,133 bitcoin as it pivots (like many miners) to AI, dropping it to fourth place.

Other DATs that have recently sold some of their bitcoin holdings include Empery Digital and Exodus Movement, while Genius Group sold all of its bitcoin.

Here’s how things have shifted since bitcoin hit its all-time high last October:

“There is absolutely a risk of contagion from bitcoin DATs like Nakamoto selling their holdings. With many entering the space at the top of the market in 2025, the longer bitcoin stays around current levels, the more pain they will feel. Corporate selling is one of the largest risks to bitcoin’s price this year,” Puckrin said, adding that if geopolitical conditions continue to weigh on risk assets and bitcoin, other DATs could start losing conviction in BTC, and at that point, it can quickly become a liquidation cascade scenario.

On the other hand, Puckrin said, the timing of new entrants into the market, such as Adam Back’s Bitcoin Treasury Standard Company (BSTR), set to go public via a SPAC with Cantor soon, is far better than many other DATs, given where bitcoin’s price is right now.

“But the corporate treasury strategy is still a risky one and must be structured as well as MSTR to remain afloat throughout the downturn,” he added.

What’s next for DATs?

While it remains to be seen if DATs’ bitcoin off-loading could significantly affect the asset’s price, the DAT model is not sustainable long-term for many, Wave Digital Assets’ head of international portfolio management, Rajiv Sawhney, said.

“Simply put, many of the DATs did not have viable business models or generate recurring revenue in a differentiated way. We’ll likely see a significant contraction, from hundreds of players today to a much smaller group,” Sawhney said, adding that this dynamic opens up a huge opportunity for M&A and consolidation in the space.

“The stronger players will be able to acquire bitcoin cheaply through equity acquisitions,” Sawhney said.

Olympus’ Bara also said that beyond looming consolidation, “because the math forces it,” exits are most likely among smaller DATs without continuous access to capital markets.

“New entrants like BSTR prove that capital still wants exposure to this category, but BSTR and Twenty One are launching with the same accumulation playbook, distributed through the same Cantor SPAC pipeline,” he said.

Finally, some experts, such as Beau Turner, CEO and cofounder of Abundant Mines, told Sherwood that many of the DATs that came on the scene to mimic Strategy were “just a trend.”

“Outside of Strategy and Metaplanet and Strive Inc., I see very few examples of truly robust business models. The companies with unique positioning and moats will find themselves surviving and thriving in the long run. The companies building a DAT because it seems like a good trend to participate in will, over the long run, be left in the dust,” Turner said.