Adobe’s CFO is buying the dip — again

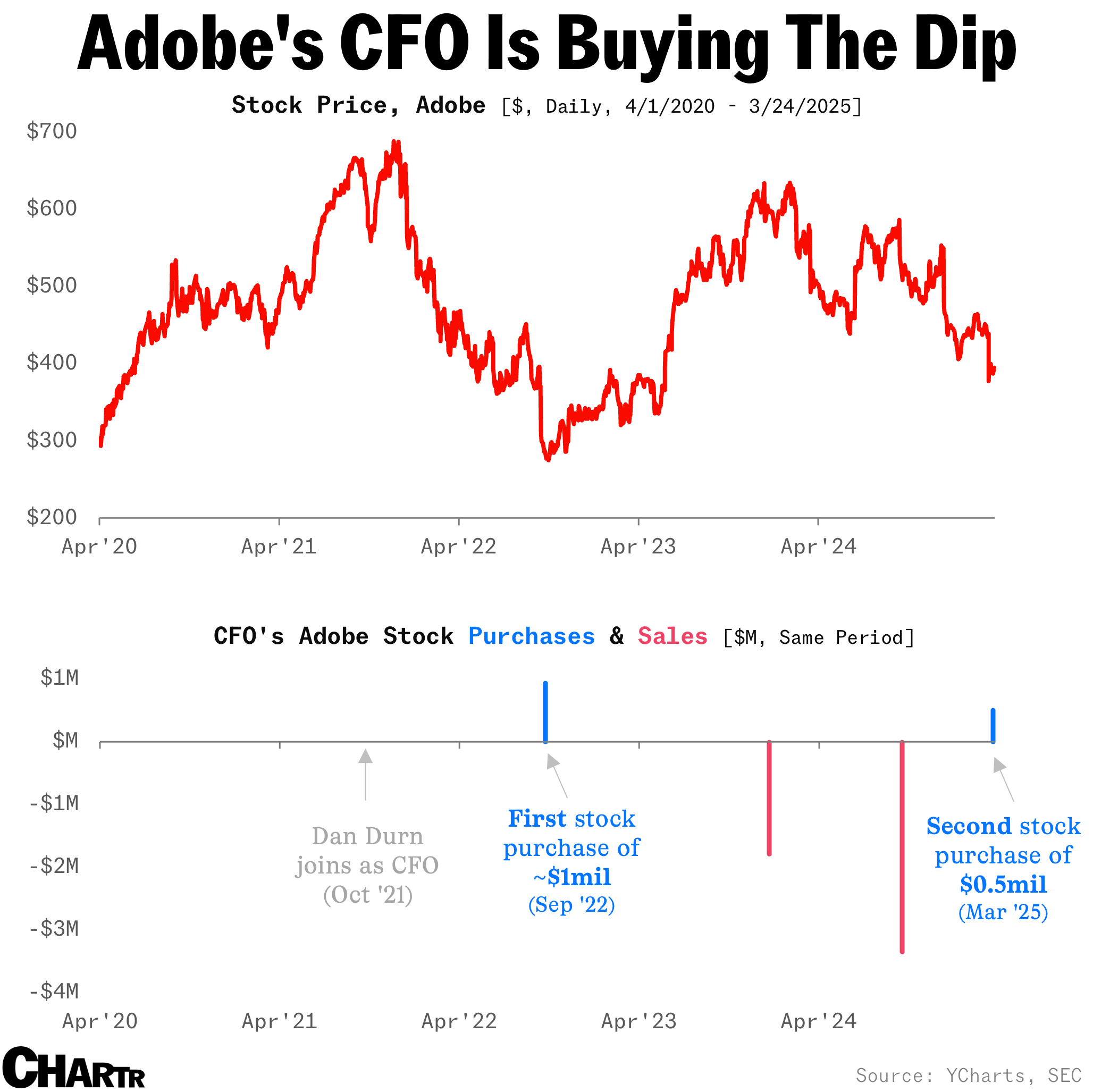

Durn’s first buy came in September 2022, just as Adobe’s stock was dropping sharply.

Adobe’s stock has been on a rough ride, with its shares shedding more than 20% over the past year.

The company’s leadership is currently focused on building out its AI-powered offerings, while trying to convince Wall Street that its AI initiatives, in particular its focus on agentic AI, will pay off in the long run for the $174 billion Photoshop giant. And its chief financier is putting his money where his mouth is: according to an SEC filing last week, Adobe CFO Dan Durn just dropped over half a million dollars to scoop up Adobe stock — only the second time he’s made an open-market purchase since joining the company in October 2021.

Buy the dip

Durn’s first buy came in September 2022, just as Adobe’s stock was tanking. Shares had cratered ~60% from its pandemic highs, spooked in part by a $20 billion plan to acquire Figma that some investors felt was overpriced. Per the SEC filings, Durn bought $936,358 worth of Adobe stock on September 22, an investment which appreciated nicely over the coming 12 months: shares soared nearly 80% in 2023 after Adobe launched its generative-AI tool Firefly and abandoned the Figma deal in December, owing to regulatory concerns.

Now, Adobe’s back under pressure. Earlier this month, the company’s lackluster Q2 revenue guidance triggered a ~14% drop in a single day, pushing shares toward another major low — and Durn bought it… again.

In a recent Reuters interview, Durn said Adobe expects to double its AI-driven recurring revenue over the next three quarters. Meanwhile, Bank of America analysts reiterated their “buy” rating last week, citing stronger monetization potential from “a broadening set of AI features” rolling out this year.

Durn’s not the only Adobe insider reloading: Director David Ricks (who is Eli Lilly’s CEO) also bought the dip back in 2022 and jumped back in this January, buying ~$1 million worth of Adobe shares on January 28.