Americans are spending less on what matters to them most: their pets

A new report from the Bank of America Institute makes heads and tails of everything pets.

The fine folks at Bank of America Institute commissioned a study on the one issue that unites the country: pet ownership.

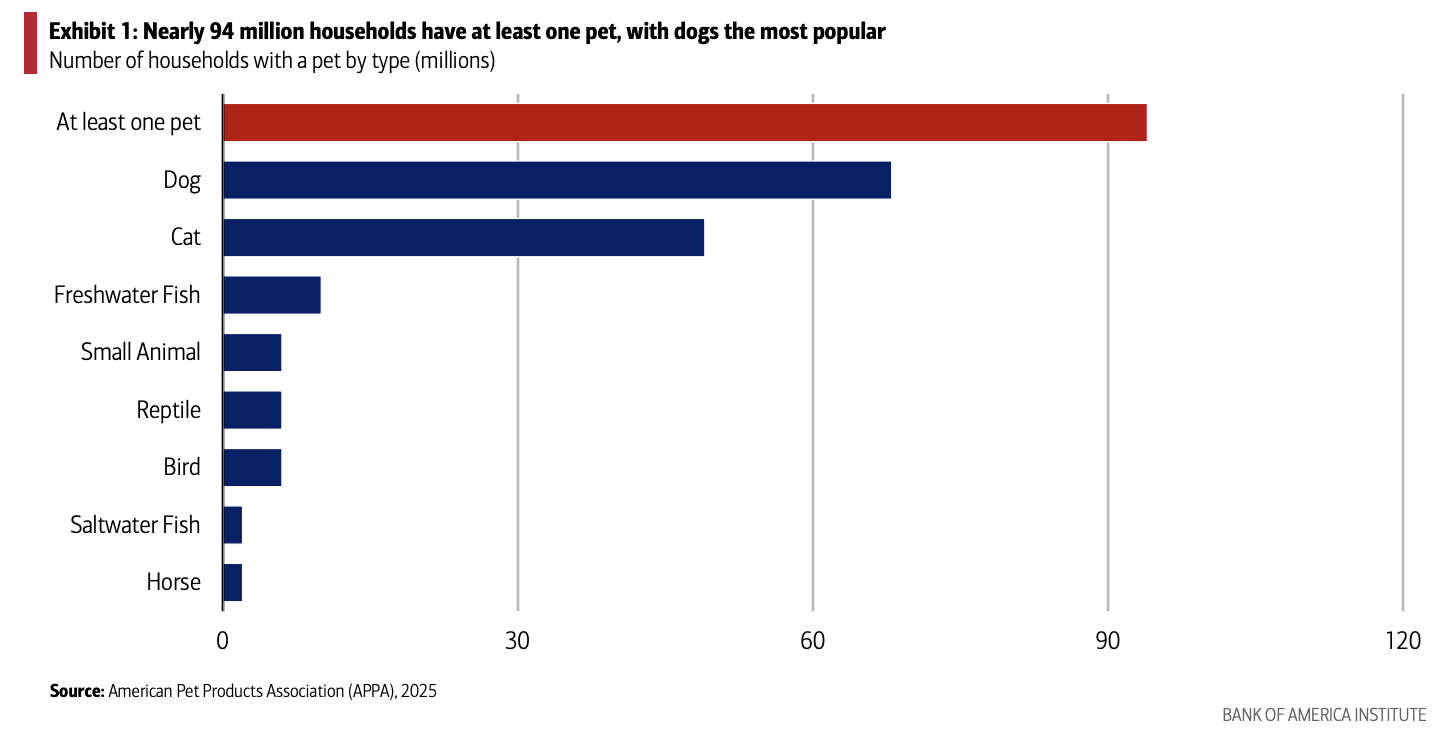

“The US is a nation of pet lovers. In fact, nearly 94 million households own at least one pet, according to the American Pet Products Association (APPA),” senior economist David Tinsley wrote. “Dogs are in the lead, but cats are on their tail.”

The report has too many fun facts to choose just one pick of the litter, so here are a few:

Millennials, many of whom have opted for fluffy friends in lieu of squalling infants, make up the biggest share of pet-owning households.

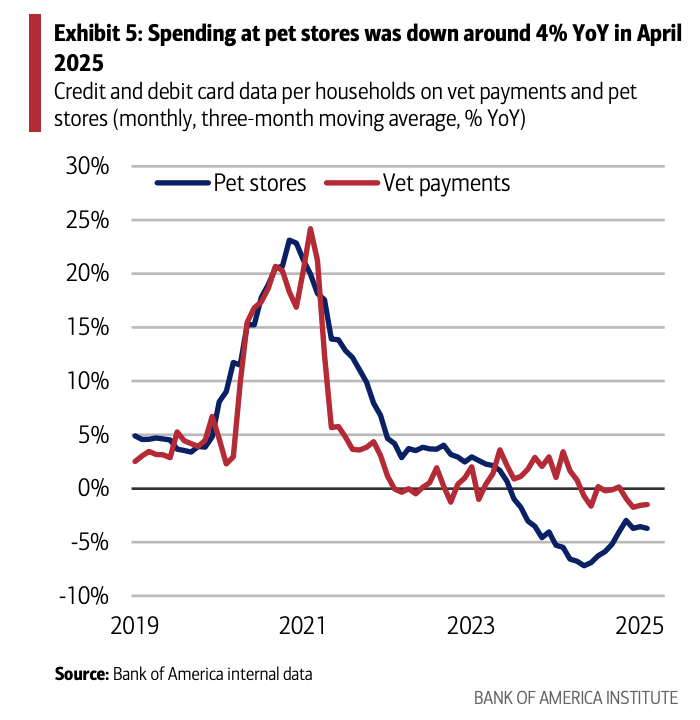

If your pet is asking you for more treats and fewer vet visits, that has nothing to do with their self-interest (pet’s note: true!). They might just be looking out for your finances: pet services inflation is running a little above 4% year on year as of April, while pet food and treat prices are flat (author’s note: praise be!).

Paging Chewy: Bank of America’s card data shows that spending at pet stores is down roughly 4% in April versus a year prior (pet’s note: what the hell?!). Lower-income millennial households appear to be fueling this pullback, per Tinsley, who wrote that “some households may be ‘trading down’ in terms of the pet foods they are buying.”

You can check out the full report here.