Apple’s stock is behaving differently from the rest of BATMMAAN because its AI strategy is nowhere

Apple is so bad at AI that its stock is increasingly detached from the rest of Big Tech. Some days that’s a blessing; on others, it’s a curse.

Hey Siri: why is Apple’s stock behaving differently from the rest of Big Tech? Siri, of course, will have absolutely no clue — because Apple’s AI strategy is borderline nonexistent.

Even at the start of this year, people were asking the question, “Why is Apple so bad at AI?” Since then, as Google’s AI efforts have gone from strength to strength, ChatGPT has grown its weekly users to nearly 900 million, and Nvidia briefly crossed a $5 trillion market cap on blowout demand for its Blackwell and Hopper chips, Apple has released some underwhelming updates to its flagship Apple Intelligence product.

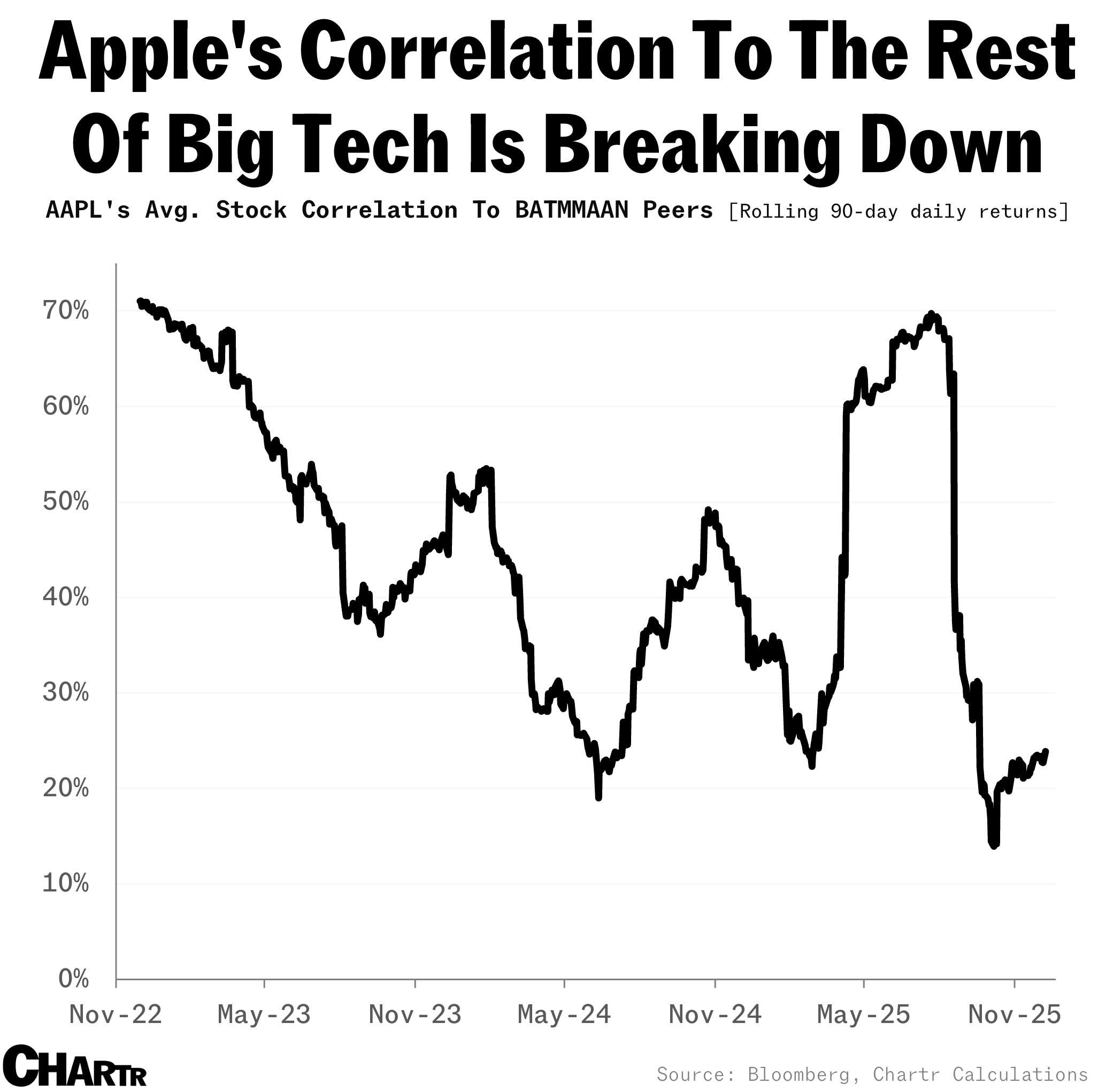

And its lack of AI progress is increasingly affecting how the stock is trading, as Apple becomes a sort of “anti-AI” vehicle for investors. Indeed, its correlation with the rest of the BATMMAAN group has dropped precipitously: when ChatGPT was released at the end of November 2022, Apple’s average pairwise correlation* to its Big Tech peers was 0.71 — recently it has dropped to as low as 0.2.

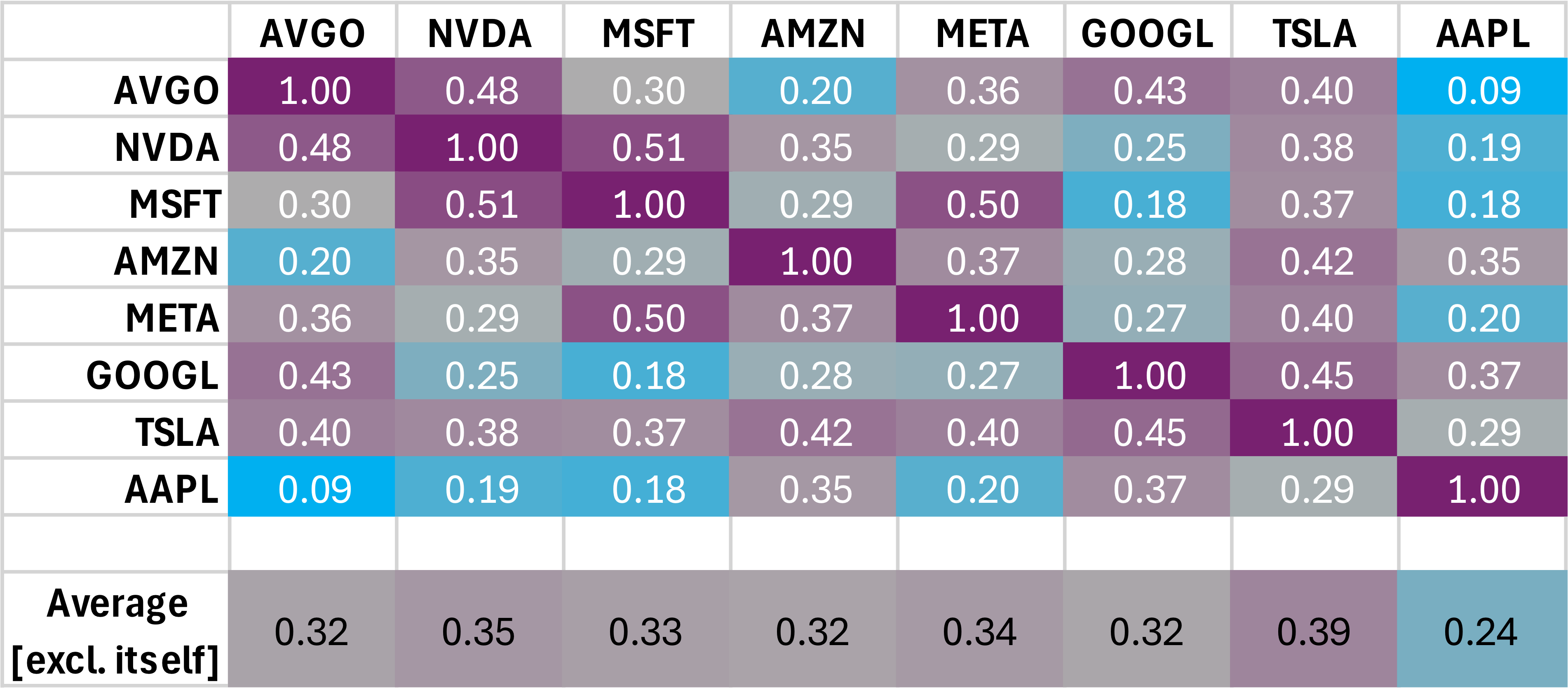

This is a pretty remarkable drop-off — and it’s been most pronounced in the stocks that are closest to the AI trade (notably Nvidia, Microsoft, and Broadcom). Apple and Microsoft used to trade nearly in tandem, with a correlation coefficient between the two north of 0.8. That has all but collapsed, with the last 90 trading sessions barely showing a positive correlation.

Of course, this detachment isn’t necessarily a bad thing. On days when the AI trade sputters — such as November 13, when tech stocks got slammed, with Nvidia and Broadcom dropping ~4% and Tesla shedding 6.6% — Apple provided some refuge for tech investors, dropping just 0.2%.

Apple is weirder than Tesla

Perhaps what’s most remarkable from mining the correlation stats is that Apple’s average correlation with the rest of its peer group is now the lowest of any BATMMAAN stock. People used to say that Tesla was the odd one out of the Big Tech giants — but the trading data suggests, fairly strongly, it’s Apple right now.

Last week, Apple retired its AI chief, potentially suggesting a renewed focus on the nascent technology under new leadership.

*Pearson correlations based on daily returns over 90-day rolling periods.