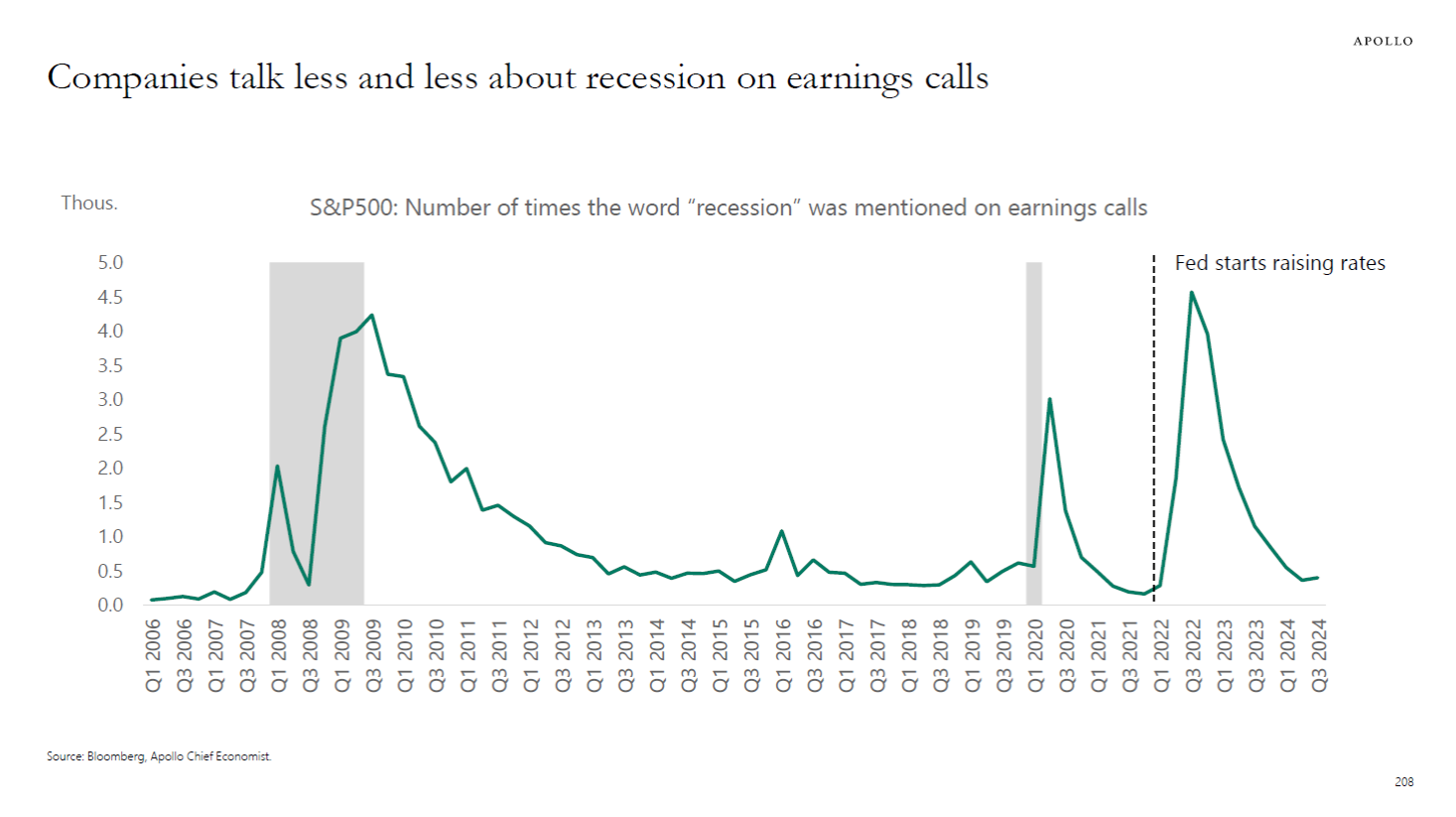

Recession talk is in recession

When companies are worried that economic trouble is brewing – or that the doom times are upon us – their leaders generally let you know.

JPMorgan CEO Jamie Dimon, for instance, famously warned of an incoming “economic hurricane” in mid-2022.

But what’s striking right now is how little companies are referencing the r-word even amid slowing growth and a rising unemployment rate.

“The media is full of anecdotes from earnings calls about the economy supposedly slowing down,” said Torsten Slok, chief economist at Apollo Global Management. “But the reality is that firms on earnings calls talk less and less about recession, see chart below.”

That matches investors’ attitudes, as a soft landing is increasingly the consensus view.

“In fact, we have never had a recession at the current low level of recession talk,” he added.

The sample size, it must be noted, gives a little something to be desired on that last claim: We’re working with just two examples, the housing bust (something which some economists and traders warned was brewing for years) and COVID, which is the textbook definition of an unexpected economic shock.

Economists, it seems, are just CEOs with a lag. They pin the odds of a US economy slipping into a recession over the next year at 30%. That’s roughly double the baseline probability for a recession, judging by their frequency since WWII.

Economists, it seems, are just CEOs with a lag. They pin the odds of a US economy slipping into a recession over the next year at 30%. That’s roughly double the baseline probability for a recession, judging by their frequency since WWII.