Financial markets and the US economy are in a tug-of-war between two paradoxes

Jevons Paradox is your reigning bull case. After July payrolls underwhelmed, enter the Paradox of Thrift.

Let’s not overcomplicate matters. The strong performance of US stocks this year is really down to two things:

1) President Donald Trump didn’t completely blow up global commerce with tariffs.

2) Jevons Paradox — the idea that as technological advances make something (in this case chips!) more efficient, you’ll still end up using more rather than less — soundly trounced DeepSeek’s seeming “Moneyball” approach to AI development.

Jevons Paradox in the current setup doesn’t mean you just buy more chips. It means you buy more servers to house those chips. And you’re going to want to buy circuits and fiber-optic cables to connect everything together, not to mention cooling equipment to make sure all your high-powered tech doesn’t run too hot. And that’s all going to be put in a data center you have to build, which will need immense amounts of power to run.

All that means that there’s currently an entire trickle-down ecosystem of profits built off of US megacap tech companies’ devotion to Jevons Paradox. Tax changes have made it materially easier for companies to keep pursuing this spending binge. And the market, by and large, is rewarding it. Why should that change?

At its core, this represents the bull case for US stocks. Don’t believe me? Well, since the February 19 pre-tariff peak for the SPDR S&P 500 ETF, total returns can be completely attributed to just three stocks: Nvidia, Microsoft, and Broadcom.

The Paradox of Thrift, however, encapsulates the bear case. It’s the idea that we can’t all tighten our belts at the same time. My spending is your income; when too many people either try to spend less (or people lose their incomes because companies decide they need to spend less!), overall economic activity goes down. With US nonfarm payroll growth coming in at just 73,000 in July, below expectations for 104,000, as the unemployment rate edged higher, worries about downside risk to the labor market are likely to assume more prominence.

Just look at some of the companies doing the most spending, as well as the single largest beneficiary: Alphabet, Amazon, Meta, Microsoft, and Nvidia, a quintet Peachtree Creek Investments’ Conor Sen dubbed the “AI 5.”

Unless Nvidia boosted payrolls by 13,505 (roughly equivalent to all the jobs the chipmaker has added since early 2022), employment in this cohort will be down quarter on quarter.

Of course, in aggregate, megacap tech companies are boosting their outlays to such an extent that it far outstrips any potential reduction in labor costs. And “reduction in labor costs” is certainly not a phrase we can associate with Mark Zuckerberg these days.

Amazon CEO Andy Jassy said that “in the next few years,” he expects that applying generative AI and agents “will reduce our total corporate workforce.”

For some companies, the future is now. Crowdstrike, Duolingo, IBM, and Salesforce have either cut jobs due to AI or said they’re hiring less than they otherwise would have. And in the background, we can’t forget about the many companies that aggressively pursued cost reductions ahead of potential worst-case scenarios for tariffs (which offers higher profitability in the near term for some!), but down the road, again, I refer you to the Paradox of Thrift.

The big problem is not that AI is going to imminently take your job. It’s merely that the marginal dollar is more likely to go to these capital expenditures than spending on labor at a time when consumption — the fruits of one’s labor income — is looking shakier.

Economic shifts happen on the margins. As the AI economy runs red-hot, other key parts (notably housing) are deep in the dumps. It’s the trouble with averages: if your head and torso are in the oven while your feet are in the freezer, in aggregate, everything seems normal, even if what you’re experiencing is two different extremes. Such is the case of the US economy.

Consumers aren’t spending less, but the growth in their spending has decelerated substantially. Nominal consumption has expanded by just 1.4% year to date through June, the slowest six-month growth since August 2020.

The good news is that income growth is increasing at nearly twice that rate; the mixed news is that much of that is down to transfer payments rather than labor market strength. Further complicating attempts to untangle how the US consumer is really doing are changes to immigration policy that signal supply, not just demand, is helping explain some of the softening.

These two paradoxes — Jevons and Thrift — are diametrically opposed to one another. One involves spending a lot; one involves spending less. It’s quite rare to see signs of both coexisting at the same time.

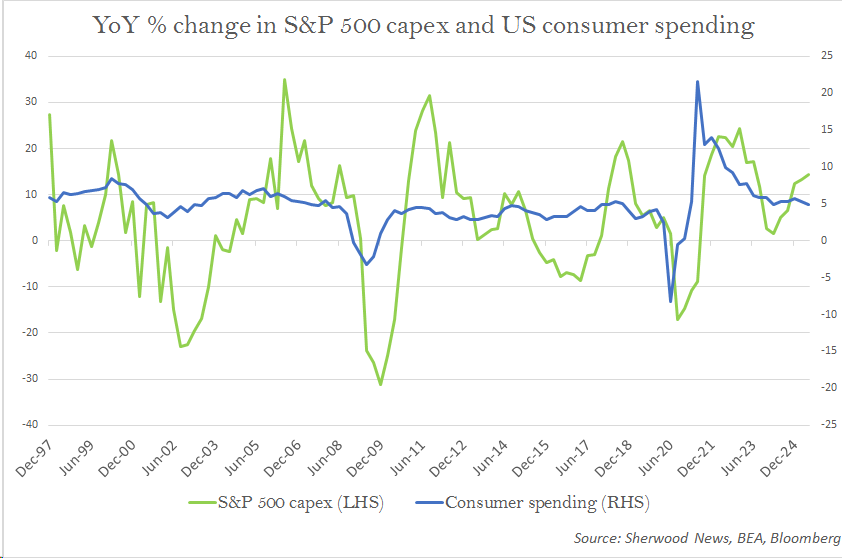

And you barely have to squint to do so. We’re in a prolonged period of decelerating growth in consumer spending accompanied by accelerating growth in S&P 500 capex:

Capital expenditures, at the S&P 500 level, are often a lagged response to dynamics that incentivize more production, which usually means accelerating consumer spending or a big spike in key commodity prices. During this boom, those factors have either not been present, or, given the low weight of energy and material companies in the benchmark US stock index, not pertinent.

In the end, all revenue generation is a function of end-user demand. We usually tend to call that end-user “the consumer.”

We’re currently running an experiment on how much business investment in what is being billed as a labor-saving (and in many cases, labor-replacing) technology can be divorced from the consumer.

It’s difficult to imagine a world where the consumer ultimately doesn’t win out. So either the net impact of all this investment — not to mention the wealth effect from stock market gains — will be to persistently boost incomes and spending, or the consumer will win by losing and dragging everything else down with them: lower spending weighing on ad revenues, tighter credit conditions crimping demand from the hyperscalers’ customers, and so on.

Or something completely novel will happen!