Global investors are fleeing US stocks at a record pace

The “sell America” trade is going viral.

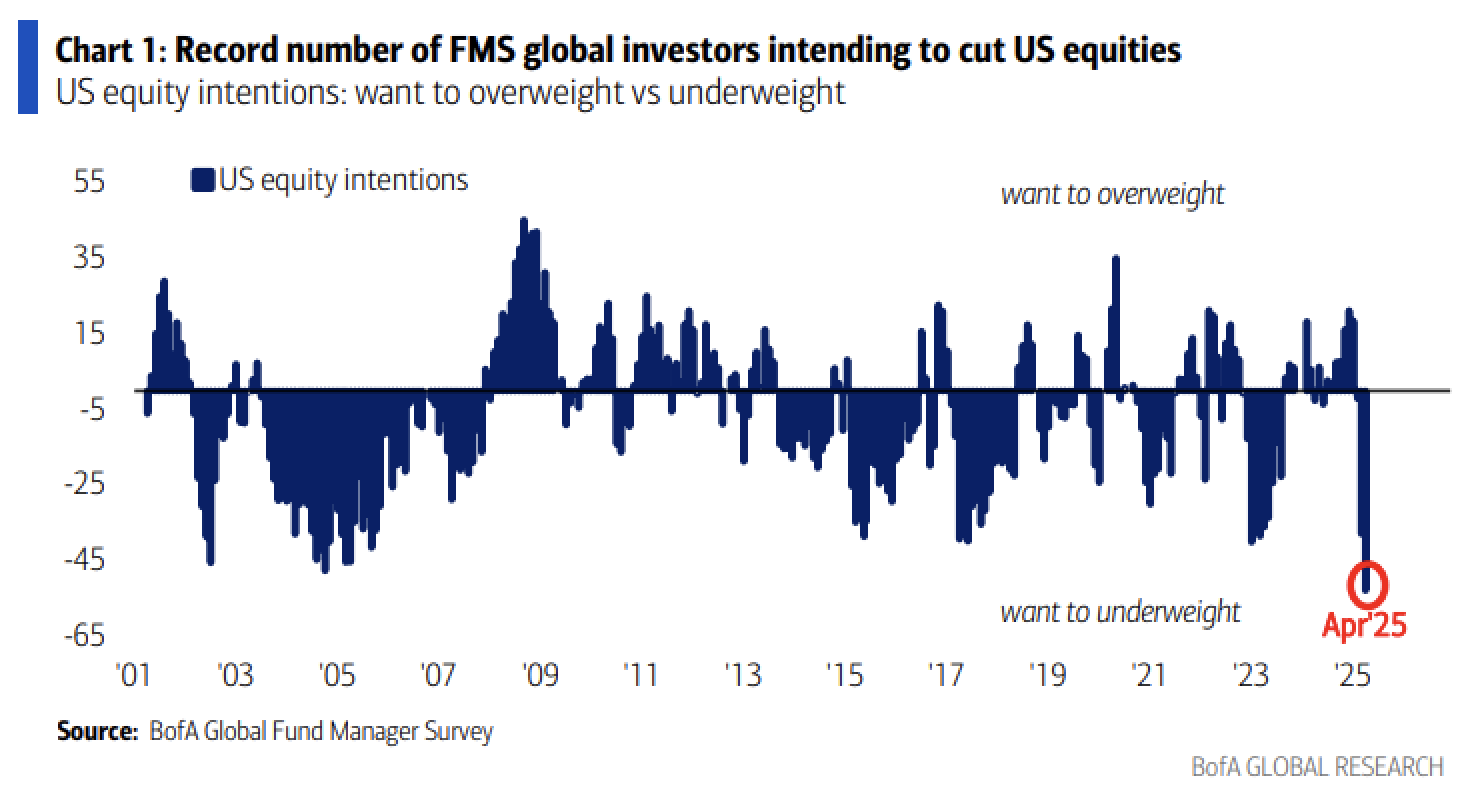

That’s the top takeaway from the April edition of Bank of America’s closely watched monthly fund manager survey, which shows that more than half of portfolio managers want to hold an underweight position in US stocks — a record. The exodus is underway in earnest, with the biggest two-month drop in portfolio managers who say they are overweight US stocks in survey history.

And 73% of respondents say the theme of “US exceptionalism” in financial markets has peaked.

A plain reading of the results suggests that portfolio managers are battening down the hatches, with tariffs poised to push inflation higher and growth lower.

Michael Hartnett, chief investment strategist at BofA Global Research, wrote that this was the fifth-most-bearish fund manager survey in the past 25 years, with the fourth-highest recession expectations (surpassed by March 2009, April 2020, and November 2022).

More signs of the changing times:

A record increase in bond allocations, with exposure to cash and defensive stock market sectors like utilities, healthcare, and staples also rising.

A net 28% say the US profit outlook is unfavorable, the lowest reading since November 2007.

Relative trust in policymakers has been exported from America to China. Investors are more confident in Chinese policymakers providing stimulus that boosts growth in the second half of the year than they are in US politicians passing tax cuts that juice growth.

The Magnificent 7 are no longer deemed the “most crowded trade” for the first time in over two years; that title has instead been ceded to gold, a shiny rock with no yield that tends to do better than other assets when pessimism is the only thing in a bull market. Though it’s deemed to be crowded, that’s for good reason according to portfolio managers: it was the top answer for the best-performing asset class of this year.

The survey period was April 4 to April 10. If we assume a somewhat equal distribution, this implies that more responses came when US stocks were in free fall than during this nascent bounce.

A plain reading of the results suggests that portfolio managers are battening down the hatches, with tariffs poised to push inflation higher and growth lower.

Michael Hartnett, chief investment strategist at BofA Global Research, wrote that this was the fifth-most-bearish fund manager survey in the past 25 years, with the fourth-highest recession expectations (surpassed by March 2009, April 2020, and November 2022).

More signs of the changing times:

A record increase in bond allocations, with exposure to cash and defensive stock market sectors like utilities, healthcare, and staples also rising.

A net 28% say the US profit outlook is unfavorable, the lowest reading since November 2007.

Relative trust in policymakers has been exported from America to China. Investors are more confident in Chinese policymakers providing stimulus that boosts growth in the second half of the year than they are in US politicians passing tax cuts that juice growth.

The Magnificent 7 are no longer deemed the “most crowded trade” for the first time in over two years; that title has instead been ceded to gold, a shiny rock with no yield that tends to do better than other assets when pessimism is the only thing in a bull market. Though it’s deemed to be crowded, that’s for good reason according to portfolio managers: it was the top answer for the best-performing asset class of this year.

The survey period was April 4 to April 10. If we assume a somewhat equal distribution, this implies that more responses came when US stocks were in free fall than during this nascent bounce.