Here’s how much the new China export curbs will hit Nvidia’s earnings, according to Bank of America

Bank of America analysts have made their first crack at quantifying how big a headwind Nvidia’s inability to export its H20 semiconductors to China will be for the chip designer.

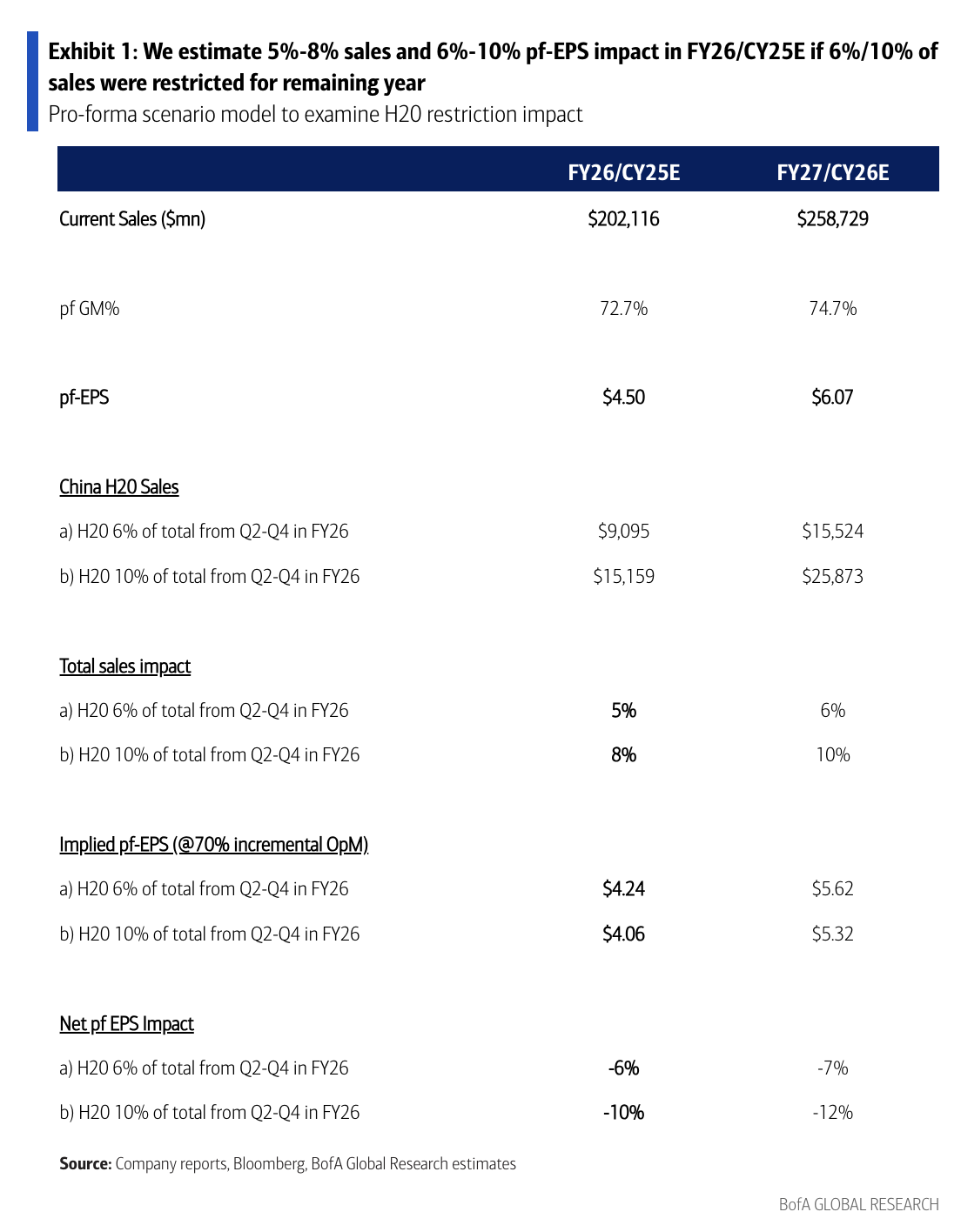

“Ignoring any positive offsets (stronger Blackwell sales), we estimate a 5%-8% sales and 6% to 10% EPS impact under two scenarios of H20 at 6% or 10% of fiscal year 2026/calendar year 2025 estimated sales,” analyst Vivek Arya wrote.

That being said, Arya wants you to remember the positive offsets, citing “positive comments re AI chips demand from OpenAI, Google, and Amazon coupled with stronger ASP of next-gen NVDA GB300 Blackwell Ultra.”

A better-than-expected showing for Nvidia’s Blackwell ramp could help offset not only the negatives from these new restrictions, but also higher costs of manufacturing in the US that are poised to weigh on margins — which has been a sore spot for the company as of late.

Arya maintained his “buy” rating and $160 price target on the stock.

“One could also argue the immediate stock decline would be unwelcome but perhaps reduce the overhang that has existed on the stock since late last year when the Biden administration increased AI chip controls,” he wrote. “We believe AI remains the fastest growing secular growth opportunity in semis, and view stock volatility as an enhanced buying opportunity for NVDA.”