Banks thrived with rising rates, but can't win with stable ones

Net interest income in focus for earnings season

Last Friday, JPMorgan’s stock fell more than 6% after the bank failed to raise guidance on its net interest income (NII), or the difference between what the bank makes from loans, mortgages, and other interest-bearing assets and what it pays out to depositors. It mirrored a surprising trend seen in Citi and Well Fargo’s earnings calls.

Why are banks struggling to capitalize on higher interest rates? Because deposit rates are climbing, and loan issuances are slowing.

When the Federal Reserve cut rates to near-0% in 2020, banks reduced the rates they charged borrowers as well as the rates they paid depositors, lowering both the inflows and outflows that factor into NII.

However, as the Fed raised rates in 2022, banks were able increase rates on their loans again, improving their NIIs. Intuition would suggest that with the Fed now signaling that interest rates will likely be higher for longer, banks will benefit by continuing to flex their pricing power. But the opposite has been true.

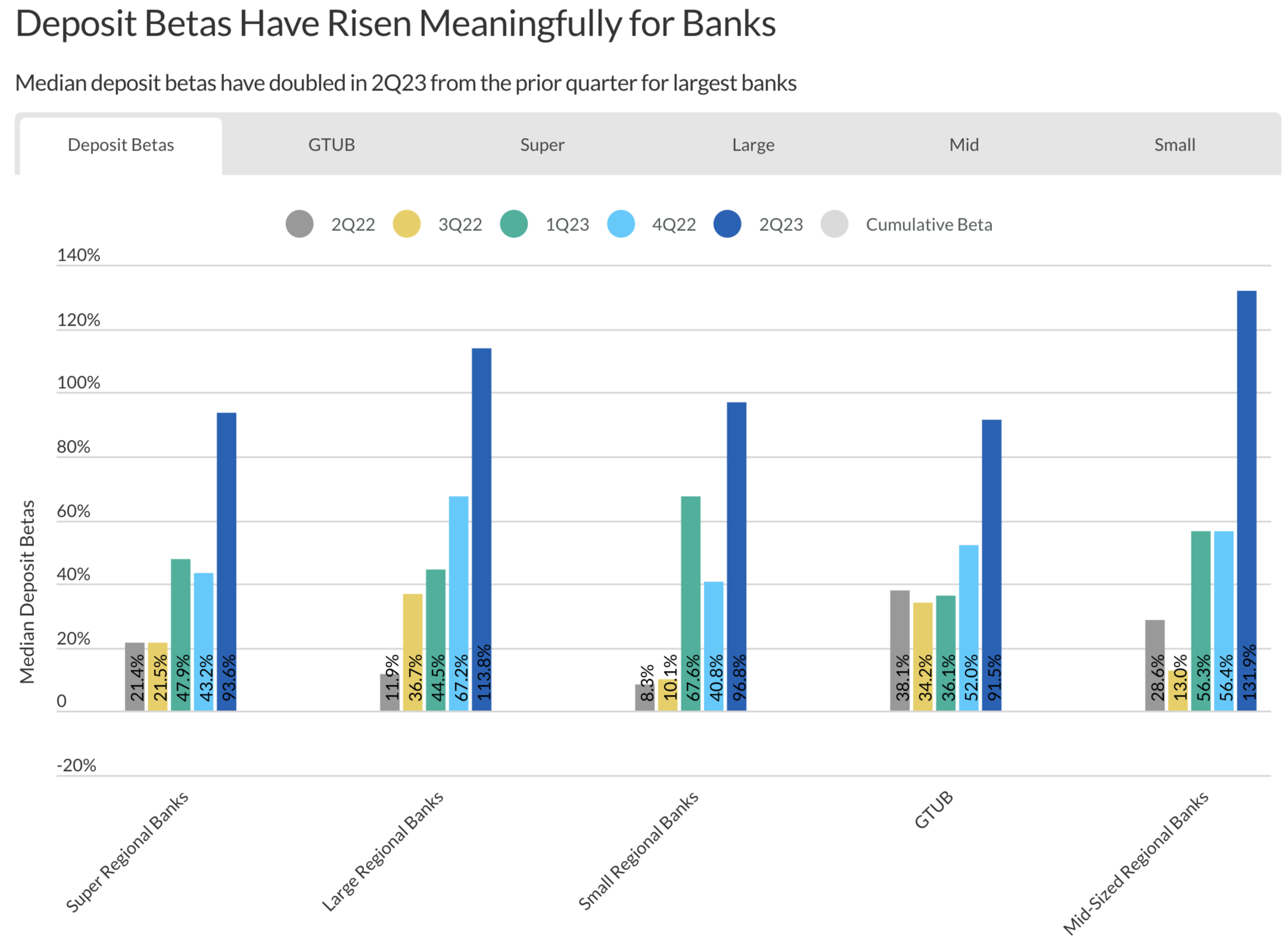

Banks use the term “deposit beta” to describe how much their deposit rates will change in response to changes in the fed funds rate, which is the Fed's target interest rate. If the Fed were to raise the fed funds rate by 50 basis points (bps), for example, and a bank were to increase how much they paid depositors by 25 bps, that bank’s deposit beta would be 50%.

As rates stabilized at higher levels, deposit betas have skyrocketed as banks have been forced to offer higher and higher yields on deposits to reduce outflows to money market funds, as well as to competing banks. According to ratings agency Fitch, deposit betas across all banks doubled in Q2 2023 from the prior quarter.

Debt issuance is also expected to decline in 2024, according to S&P Global. Banks charge higher interest rates on commercial loans, mortgages and other interest-bearing assets than they pay depositors, but loan demand has plateaued, further pressuring interest income.

Rising rates were a boon for banks, as they could raise rates on their loan products while deposit rates were low. However, stabilizing high interest rates have proved problematic, as competition is forcing banks to raise their deposit rates, and borrowers are more cautious about taking out new loans.