How some US companies are turning a potential tariff hangover into an even bigger profit party

By preparing for the worst, these management teams no longer have to hope for the best.

By preparing for the worst, some of America’s leading companies no longer have to hope for the best.

Sam Rines, macro strategist at WisdomTree and the brains behind its GeoAlpha Opportunities Fund, has a brilliant thesis that helps explain one of the thornier questions in markets: how have stocks done so well, and earnings estimates held up so much, despite a big rise in tariff rates (albeit in many cases not as bad as what was floated on April 2)?

One could be pithy and just say “AI,” but that would be incomplete.

Rines is one of my favorite strategists for the way he scours micro information from companies to inform macro, top-down views about the economy and financial markets, and his work in unpacking how management teams are adapting to tariffs of an unknown size and scope is a great example of just this.

Here’s an excerpt from his recent note:

“Then there are the companies with ‘too much tariff’ priced in. And those are the ones to watch. Again, there is a particular cadence to the companies —

- Guided for the worst of all possible worlds. (the reverse Leibniz guide)

- Found out it was not quite that bad after various tariff announcements and internal adjustments.

- Are now guiding some of the impact back to the bottom line. (emerged from the Dark Night of Earnings)”

One thing that blue-chip companies are very good at is overcoming shocks. I mean, look at the chart:

(It helps that the ones that aren’t get expunged from the index and replaced by firms that are!)

When you tell management teams that they’re about to have a 500-pound cross to bear, they’ll prepare. And when that turns out to be 350 pounds, they’ll be able to run a sub-three-hour marathon carrying it.

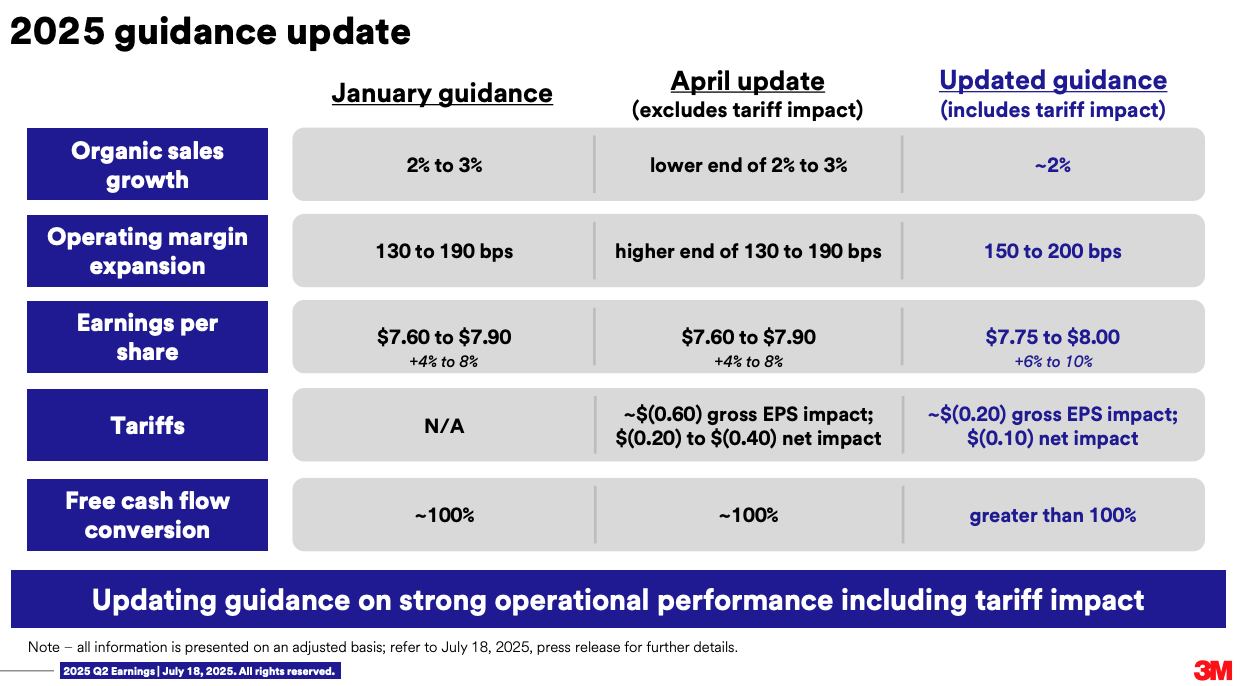

Rines highlights a few examples of this phenomenon during this earnings season. The best one, without a doubt, is 3M.

“Guiding down the tariff impact from $0.20 to $0.40 of net impact to $0.10 might sound trivial,” he wrote. “But the interaction of expecting a larger impact and preparing for it led 3M to guide earnings higher than their pre-tariff (January) expectation.”

Now, does this hold as a general rule? That’s a little tough to disentangle (and the answer is probably not). S&P 500 2025 earnings-per-share estimates are well below where they started the year. There is a tendency for calendar-year earnings to be revised lower within the year, though. So I’m not prepared to say (nor is Rines!) that tariffs are outright positive for earnings. But based on his work, I am fairly confident in concluding that tariffs provided a kick in the rear end that catalyzed some executive teams to make decisions that are boosting the profitability of their businesses.

Rines highlights Procter & Gamble, Deere & Co., and Kimberly-Clark as some of the stocks to watch to observe how widespread this dynamic may be.

“There are plenty of companies with a tariff overhang. For some, that hangover will be warranted. But others will emerge on the other side with better outcomes,” he concluded. “It may be surprising to see who the winners are at the end of earnings season. With tariff impacts being mitigated and pricing plans to come, this earnings season could be surprisingly positive.”

(Somehow, we got through this piece without referencing the apocryphal and not quite correct quote from JFK about how the Chinese word for crisis is composed of “danger” and “opportunity.”)