Megacaps have dragged markets into the red this year, but a majority of the S&P 500 is still in the green

52% of the S&P 500 has made gains in 2025. So far.

Markets have turned red this week, with America’s flagship index, the SPDR S&P 500 Trust, shedding the last of its postelection gains as traders rushed to the exits on “Tariff Tuesday,” compounding Monday’s 1.8% fall.

As companies and investors continue to digest President Donald Trump’s trade policy and the retaliatory measures it has inspired, investors are simultaneously reevaluating the AI trade on the fly. Yesterday afternoon’s price action suggested they aren’t giving up on it just yet.

Middle market

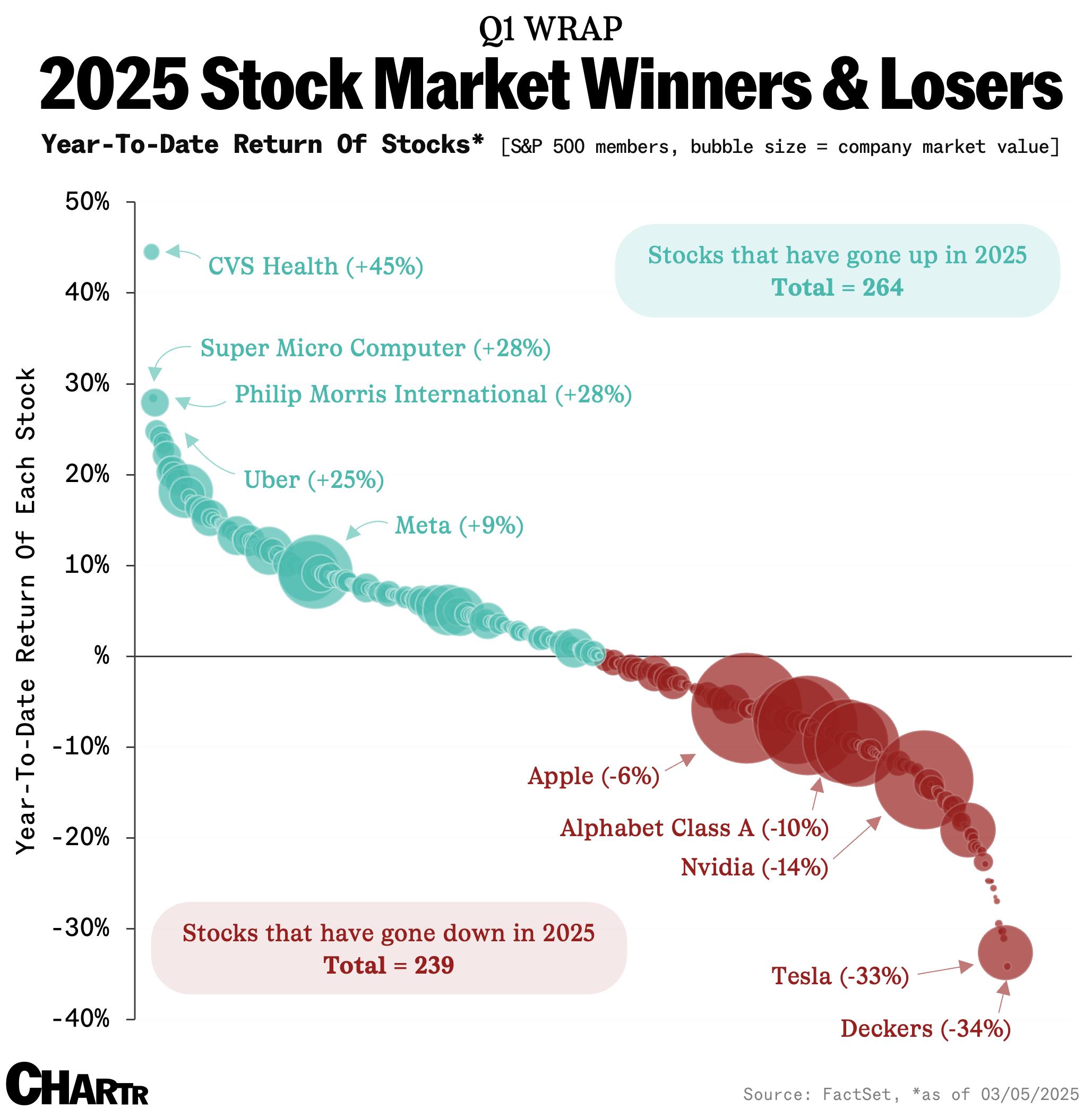

As we take stock on Wednesday morning, it’s worth zooming out and noting that 264 of the S&P 500’s constituents, or a little over 52% of the index, are actually still up in 2025. Indeed, if you woke up this morning after being asleep since New Year’s Eve, you’d have a hard time guessing that we’ve already had the “DeepSeek freak,” uncertainty over rising geopolitical tensions, and tariffs hitting the headlines this year, with the median S&P 500 stock up 0.7% in 2025.

The star of the S&P 500 Class of Q1 so far is CVS Health, which has jumped 45% since the start of the year, closely followed by Philip Morris International and Super Micro, which is doing the absolute bare minimum to remain on the market. Uber also joins the all-star lineup, ahead of Meta, which is the best of the Big Tech stocks, evading the pain of peers Amazon (-7%), Nvidia (-14%), and Tesla (-33%), which are all down. But the one company that’s down deepest in the trenches is UGG and Hoka shoe company Deckers, which never recovered from getting stomped after its underwhelming Q3 update.

So, not everything is down this year... but if you are nervous about a sustained market drop, it might be helpful to know which stocks are most, and least, sensitive to a market crash. Here’s a handy list of each, based on the last three years of data.