Nvidia is still the Bo Jackson of stocks

Palantir brags about its score on the “Rule of 40” — but NVDA just put up 69% revenue growth on huge margins. That’s a Bo-level double threat.

There’s only one professional athlete that’s been named an All-Star in two major North American sports.

His name is Bo Jackson, and in a remarkable injury-shortened career, he swung, ran, threw, and slid his way into the coveted All-Star rosters of the MLB and NFL. In the world of investing, Nvidia continues to pull off an almost equally impressive feat.

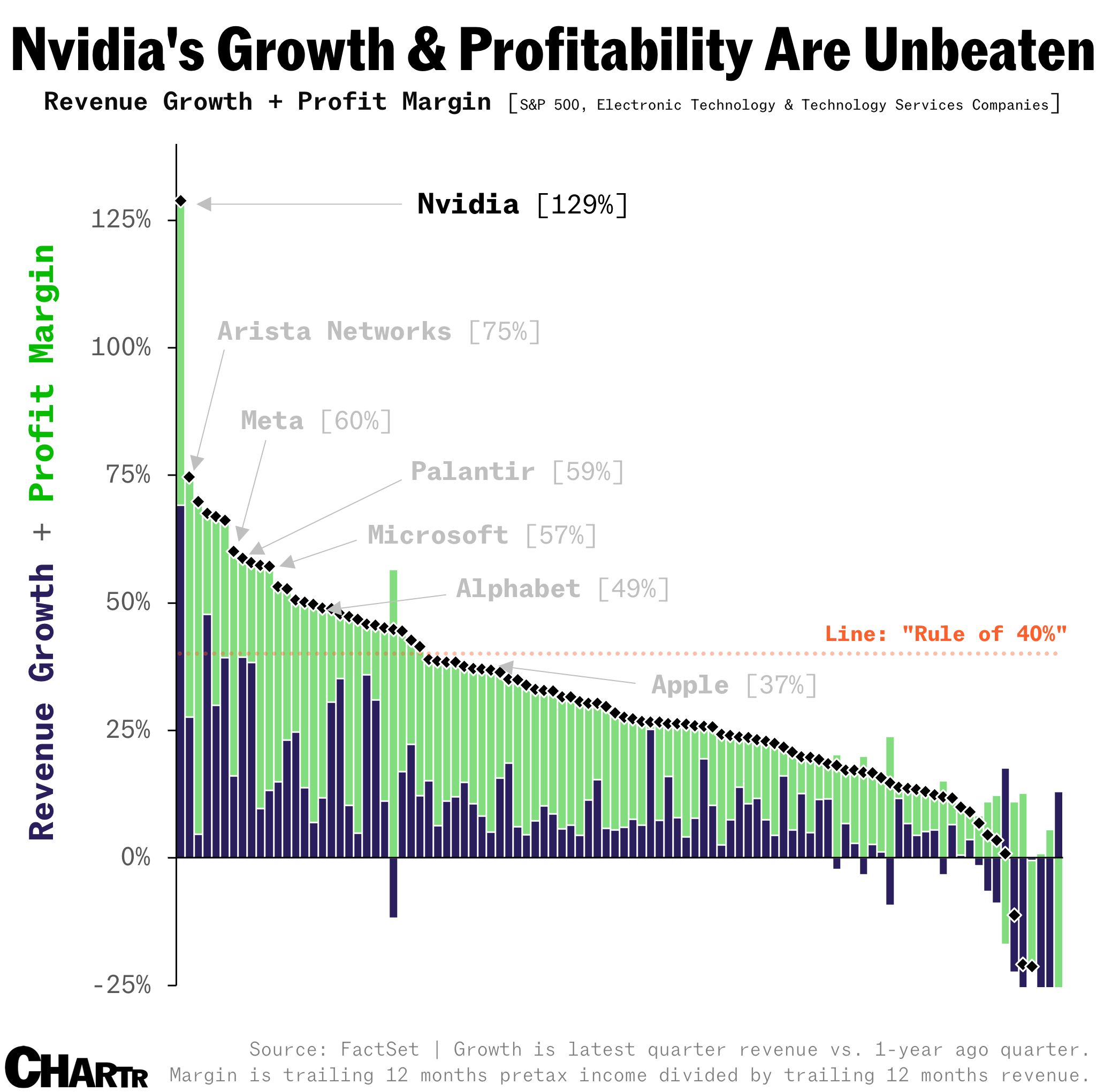

The Rule of 40

When I first failed to resist the pull of the stock market sports analogy last year, noting that Nvidia’s profitable growth was starting to feel very Bo-like, it seemed hard to imagine Nvidia would continue to advance at a similarly blistering pace. But, amid the DeepSeek panic, margin blips, export restrictions in one of its largest markets, and supply chain bottlenecks, Nvidia continues to deliver that rarest of combinations: growth and profitability.

In its Q1 results yesterday, Nvidia posted a strong revenue beat, with sales coming in at $44.1 billion, up 69% year on year. Over the last four quarters, Nvidia’s net profit margin (pretax) has been 60%. That’s a Jackson-level dual threat that’s entirely unparalleled in large-cap stocks in the public market today, and it goes a long way toward explaining why, even at an eye-watering $3.3 trillion valuation, investors have been bidding up Nvidia’s stock on Thursday.

We can get some helpful context on just how good that is from the “Rule of 40” — a helpful heuristic typically applied to fast-growing startups by venture capital investors that posits that a company’s growth rate plus its margin should equal at least 40%. To be considered “healthy,” you need to be growing fast, solidly profitable, or some decent combination of the two.

Nvidia’s score over the last 12 months would be 69% + 60% = 129%. Compared to its tech peers in the S&P 500 index, most of which unsurprisingly don’t meet that very high bar, that is unrivaled. Meta’s is a solid 60%, but that’s still less than half of Jensen Huang’s company. Apple, one of the more mature members of the Magnificent 7, scored 37%, made up of 5% growth and a 32% margin.

Palantir is a particularly interesting company, with its executive team routinely embracing the Rule of 40 as a yardstick. Indeed, the company’s latest quarterly results start with this opening sentence:

“Our Rule of 40 score increased to 83% in the last quarter, once again breaking the metric.”

That particular calculation, however, uses Palantir’s “adjusted operating margin,” and it’s no surprise, of course, that margins tend to be bigger when you “adjust” some costs out of them. Per my calculations, which use the plain old bottom line pretax, Palantir’s score is more like 59% — still very healthy, but not quite as lights out as CEO Alex Karp would perhaps like.

Bo knows

My argument last year, which I’ll drop as an addendum at the end of this piece, was that adding the two numbers together isn’t the best way to screen for stocks that are exceptional at delivering both our desired qualities. Multiplying is better.

On that metric, which we’re calling the Bo Jackson Index, Nvidia continues to lead not only its tech peers, but the entire S&P 500. Out of the companies in the index with positive growth and margins, the average score is 223. Nvidia’s is over 4,000.

That’s a bit like the heaviest player in the NFL also being one of the fastest... and having a rock-solid throwing arm.

Other stocks that score highly on this metric are Diamondback Energy; TKO Group, which owns both the UFC and WWE; and network hardware company Arista Networks.

Of course, this index shouldn’t be used as a guide on what stocks to buy — merely as a screening tool to potentially find pockets of growth. Companies delivering on this high of a level tend to be very richly valued. The secret sauce of investing is knowing whether they can keep the performance coming in the future, and for that, you need more than just a big spreadsheet.

Appendix 1: Multiplying vs. adding

Simply adding two numbers together, while a really helpful rule of thumb that we can calculate quickly, somewhat distorts our search for companies that are exceptional on both growth and margins. In other words, a company can have one glaring weakness, but make up for it by the other metric.

Another drawback of simple addition is that, statistically speaking, the variance of revenue growth is generally wider than the variance in margins, and the average margin is roughly double that of sales growth.

Hence the addition formula tends to “over-reward” growth for really high-growth companies, but also “over-rewards” margins in general.

To fix that, we can multiply the numbers together instead of adding them. Let’s consider an example of two companies. One is growing at 35% a year with a 5% margin, so it meets the Rule of 40 (just). The other is growing just a tiny bit slower, but at double the margin! Under the addition rule, they score the same. By multiplying, Sweets Inc. scores much higher.

Appendix 2: Methodology

Bo Jackson Index: Revenue growth multiplied by net profit margin. Example: a company with 20% revenue growth and a 10% profit margin would score 200 on the BJI.

Revenue Growth: This is calculated as the latest quarterly revenue, relative to revenue from four quarters ago, per FactSet.

Net Profit Margin: This is calculated as pretax income over the last four quarters divided by revenue over the last four quarters.

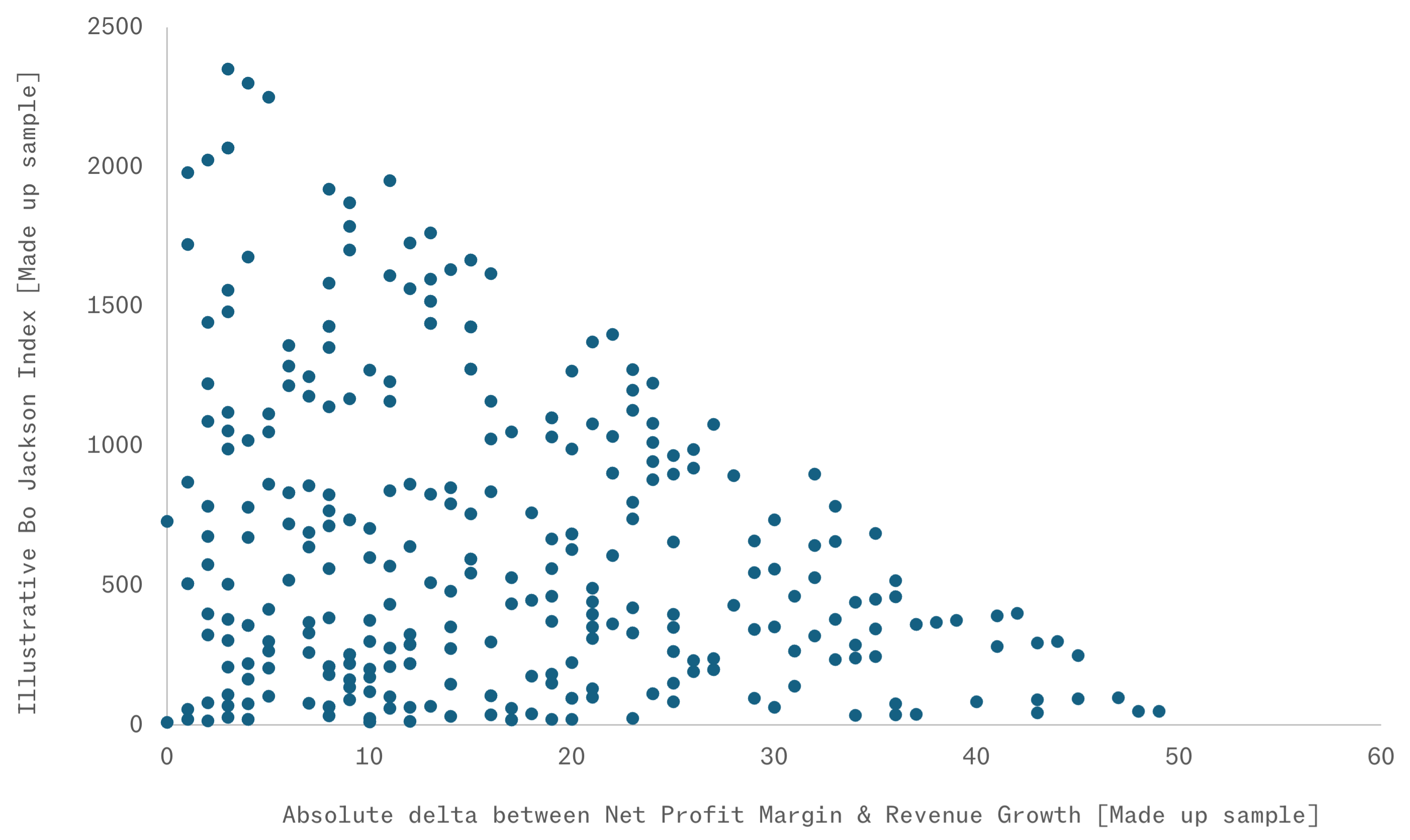

The Bo Jackson Index is just one metric, and far from perfect in assessing whether a company is growing sustainably and profitably. It is strongly correlated with the simpler Rule of 40, but it is mathematically harder to score highly on the BJI with a large gap between growth and margins. This scatter below plots a completely made-up sample of 300 “stocks” with random growth rates [0-50%] and margins [0-50%] to illustrate.

Thank you to Sherwood Media’s Nicholas Hirons for his help on the Bo Jackson Index.