Options markets signal “optimism peaks” for Magnificent 7 stocks

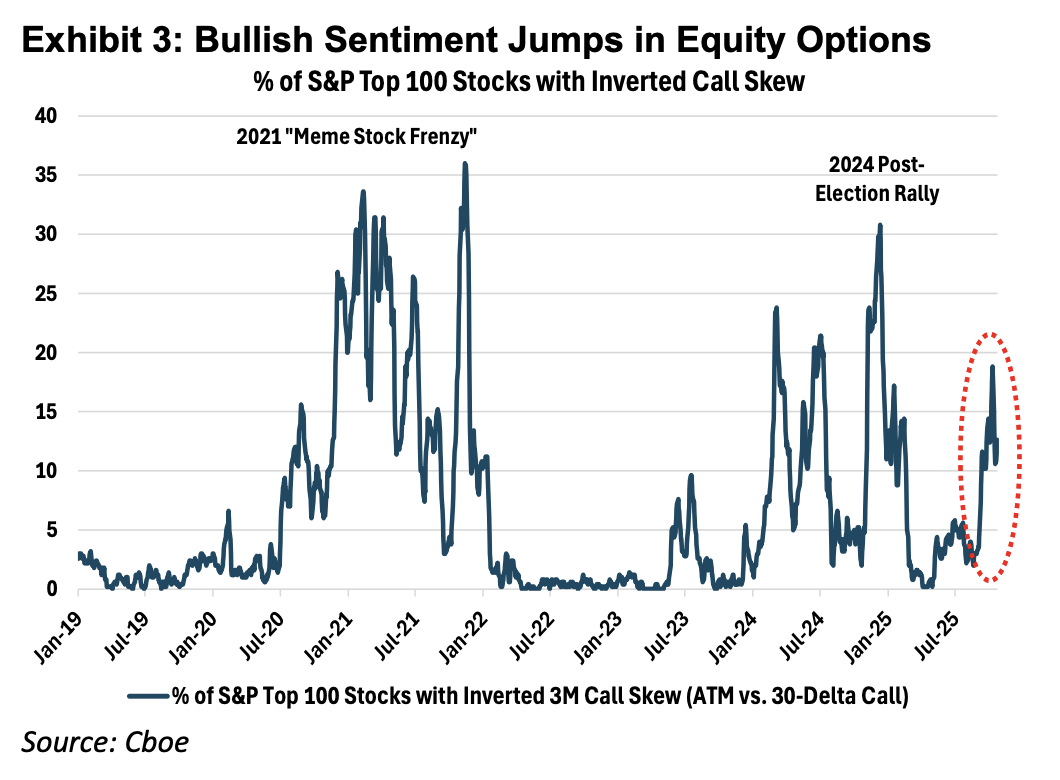

“The number of stocks in the S&P top 100 trading with inverted call skew (a sign of extremely bullish sentiment where the OTM call trades at a higher volatility than the ATM call) has surged to a high of ~20% (vs. historical average of just 3%),” per Cboe.

Of all the many ways to measure investor sentiment — surveys, futures positioning, and more — one of my favorites might be through the answer to this question: how much are traders willing to pay for options that offer upside in stocks compared to those that protect against downside?

Cboe’s head of derivatives market intelligence, Mandy Xu, noted that about three weeks ago, skew in the S&P 500 spiked amid renewed market jitters over a fraying of America’s trade relationship with China. Skew, in this case, tracks the ratio between the implied volatility of puts versus calls, a proxy for the relative demand for bearish versus bullish options. Now, that’s completely flipped on its head, for the index in general and for its largest components in particular.

She wrote (emphasis added):

“The decline in skew over the past few weeks has been notable: SPX 1M skew (25-delta ratio) has fallen from the 99th percentile high three weeks ago to a 6th percentile low early last week, before steepening at the end of last week following the Fed meeting to now the 48th percentile. Longer-dated skew screens even cheaper, with SPX 6M skew now in the 16th percentile low. The flattening in index skew is consistent with the pickup in bullish sentiment we’ve observed in single stock options. The number of stocks in the S&P top 100 trading with inverted call skew (a sign of extremely bullish sentiment where the OTM call trades at a higher volatility than the ATM call) has surged to a high of ~20% (vs. historical average of just 3%). While the metric is not yet at the extremes we saw in 2021 or late last year, it certainly signals a high level of investor optimism going into year-end.”

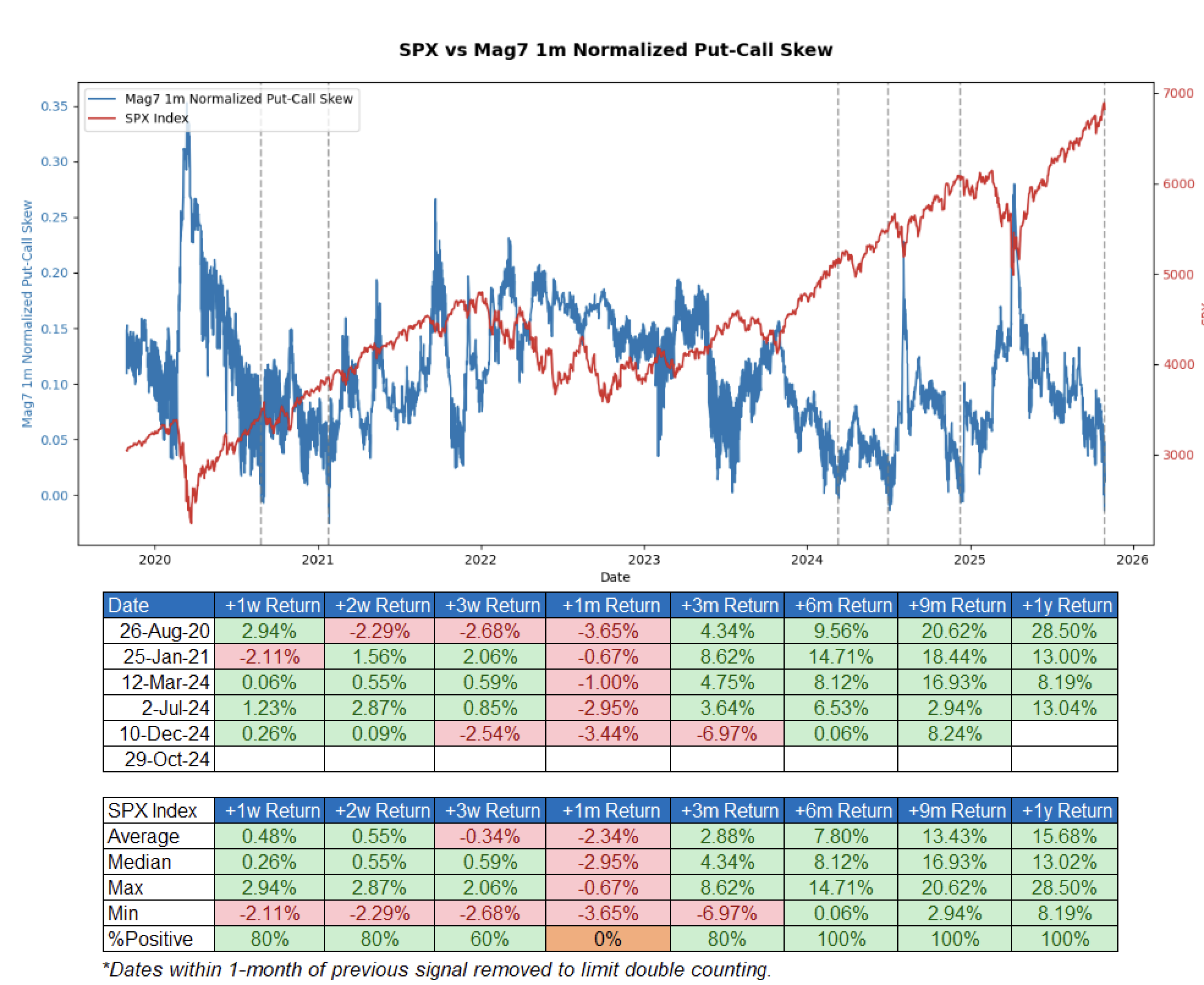

Zooming in on a similar measure, Goldman Sachs analyst Cullen Morgan shows that sentiment is particularly ebullient for the so-called Magnificent 7: the cohort of Nvidia, Apple, Microsoft, Amazon, Alphabet, Meta, and Tesla.

In an October 31 note, he wrote:

“Coming into earnings this week, put-call skew in the Mag7 complex inverted for the first time since December of last year (i.e. implied volatility of calls traded over puts). This phenomenon has only happened a handful of times. The move implies investors are overwhelmingly positioned for continued upside. Historically, such low skew readings have tended to coincide with short-term consolidation or reversals as optimism peaks.”