Pop Mart expects 350% profit spike as fan frenzy lifts sales

Chinese toymaker Pop Mart is expecting at least a 350% increase in net profit and an over 200% jump in revenue for the first half of 2025, the company announced Tuesday.

The 15-year-old Chinese designer toy company has catapulted into the global spotlight, with shoppers lining up for hours to snag its signature Labubu doll — a pointy-eared, mischievous figure with a toothy grin that’s become a collector’s obsession and has been seen dangling from celebrities’ handbags.

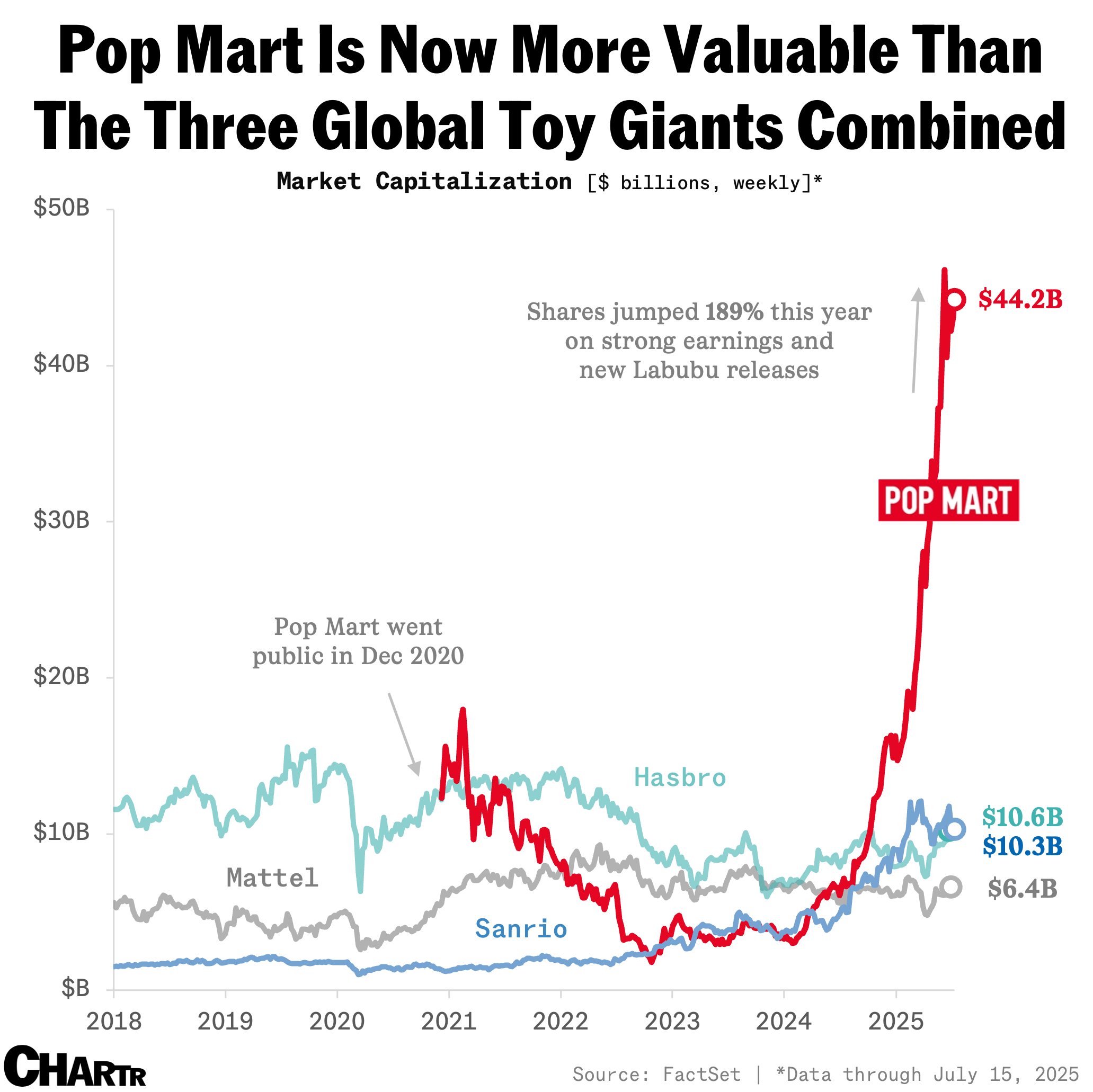

Since its rocky post-IPO debut in 2020, the company has staged a sharp turnaround, with shares rising nearly 600% over the past 12 months. That’s left Pop Mart with a market cap north of $44 billion, more than the combined value of Sanrio, Hasbro, and Mattel — the toy giants behind Hello Kitty, Transformers, and Barbie, respectively.

The company attributed its massive bottom-line growth not only to rising brand recognition but also to “constant product costs optimization” and “strengthened expense control,” according to Tuesday’s statement.

Go Deeper: Pop Mart is now worth more than the makers of Barbie, Hello Kitty, and Transformers — combined

Since its rocky post-IPO debut in 2020, the company has staged a sharp turnaround, with shares rising nearly 600% over the past 12 months. That’s left Pop Mart with a market cap north of $44 billion, more than the combined value of Sanrio, Hasbro, and Mattel — the toy giants behind Hello Kitty, Transformers, and Barbie, respectively.

The company attributed its massive bottom-line growth not only to rising brand recognition but also to “constant product costs optimization” and “strengthened expense control,” according to Tuesday’s statement.

Go Deeper: Pop Mart is now worth more than the makers of Barbie, Hello Kitty, and Transformers — combined