Q1 earnings season is déjà vu all over again for a market that has swapped tariffs for war

Glass half full: stock prices catch up to earnings estimates as geopolitical risk fades. Glass half empty: geopolitical and recession risks rise from here, or investors keep shrugging off better-than-expected tech earnings.

After reeling from a shock delivered by the White House, US stocks are rebounding vigorously heading into Q1 earnings season.

If you’re having déjà vu, that’s because the setup for April 2026 is strikingly similar to what was transpiring about a year ago.

The glass-half-full view would suggest that earnings season offers a fantastic opportunity for stock prices to catch up to profit estimates as geopolitical risk continues to fade. More pessimistic soothsayers might presume that a return of kinetic conflict in the Middle East could boost recession risks and steal the spotlight from corporate results, or that traders will simply keep shrugging off better-than-expected tech earnings.

While the reporting period a year ago may have been all about how companies were planning for the tariffs that pushed the S&P 500 to the brink of a bear market, it turned out that those results poured jet fuel on a market recovery spurred by President Trump reducing the severity of his restrictive trade policies.

Trump slashed reciprocal tariffs on April 9, two days before JPMorgan’s results unofficially kicked off earnings season. The ensuing big bottom-line beats showed that Corporate America was in a much better starting position than previously thought to grapple with the levies on cross-border commerce.

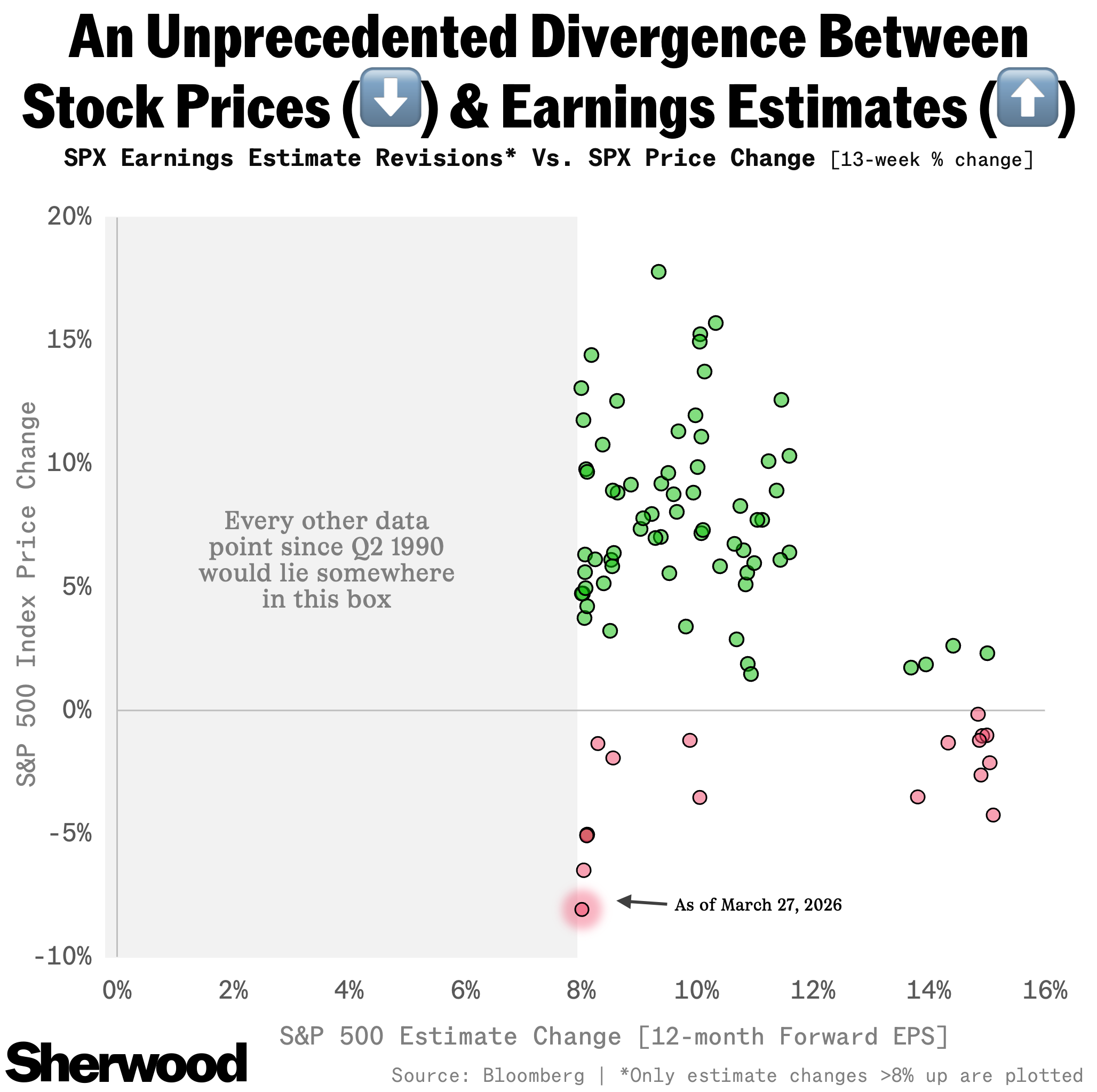

A repeat of that outcome would see the recent unprecedented divergence between stock prices (falling) and earnings estimates (rising) reconciled by corporate results that inspire the former to catch up with the latter.

But that of course assumes the two-week ceasefire between the US and Iran will lead to a longer-lasting agreement, and that the damage already done to global energy markets won’t materially weigh on economic activity going forward. While tariff rate hikes can be quickly reversed, damage to energy infrastructure can’t be undone via executive orders.

A bigger distinction between April 2025 and 2026 lies in what’s expected from Corporate America — and how little that’s mattered to traders lately.

Last year, S&P 500 12-month forward earnings estimates had started to roll over as analysts began to incorporate their views on how tariffs would weigh on profitability.

By contrast, FactSet Senior Earnings Analyst John Butters notes that the share of S&P 500 companies issuing positive earnings-per-share guidance this quarter is the highest since Q3 2021, when the economic reopening from the pandemic was kicking into an even higher gear.

Zooming out to 12-month forward earnings revisions, there are two standout sectors that have seen profit estimates soar since the end of 2025: energy and tech.

You can’t blame LPL Financial Chief Equity Strategist Jeffrey Buchbinder and Chief Technical Strategist Adam Turnquist for prefacing their Q1 earnings outlook by quipping, “At the risk of writing about something that markets may not care much about right now...”

The Mideast war that’s dominated investor discourse is the cause of this brighter outlook for energy companies’ bottom lines. The relative performance of the Energy Select Sector SPDR Fund versus the SPDR S&P 500 ETF typically tracks whatever crude oil futures have been doing. So if the energy sector’s relative performance and earnings outlook is getting sharply better from here, it’s probably a bad-news story for markets about further disruption to global energy supplies.

And traders’ “that don’t impress me much” attitude toward tech profits also predates US strikes against Iran. Despite tech companies handily besting profit expectations last reporting period, their stocks tended to fall thereafter.

While much of this is down to structural pessimism over AI tools usurping established software companies, semiconductor stocks weren’t immune from this trend either.

The medium-term outlook for return on AI investments, which will both govern the longevity of the boom for chip companies and also inform how quickly most hyperscalers can get back to generating ever-growing billions in free cash flow, has resulted in a much more cautious stance and pick-your-spots approach for the theme in 2026 versus 2025. The positive reaction to Amazon’s commitment to “investing to be the meaningful leader” in AI on Thursday is more the exception than the rule..

But with Goldman Sachs spotlighting attractive valuations in tech when judged against relative profit growth, perhaps another quarter of better-than-expected earnings will prompt investors to shift their focus away from long-term displacement and near-term cash flow stresses.