Foundational issues

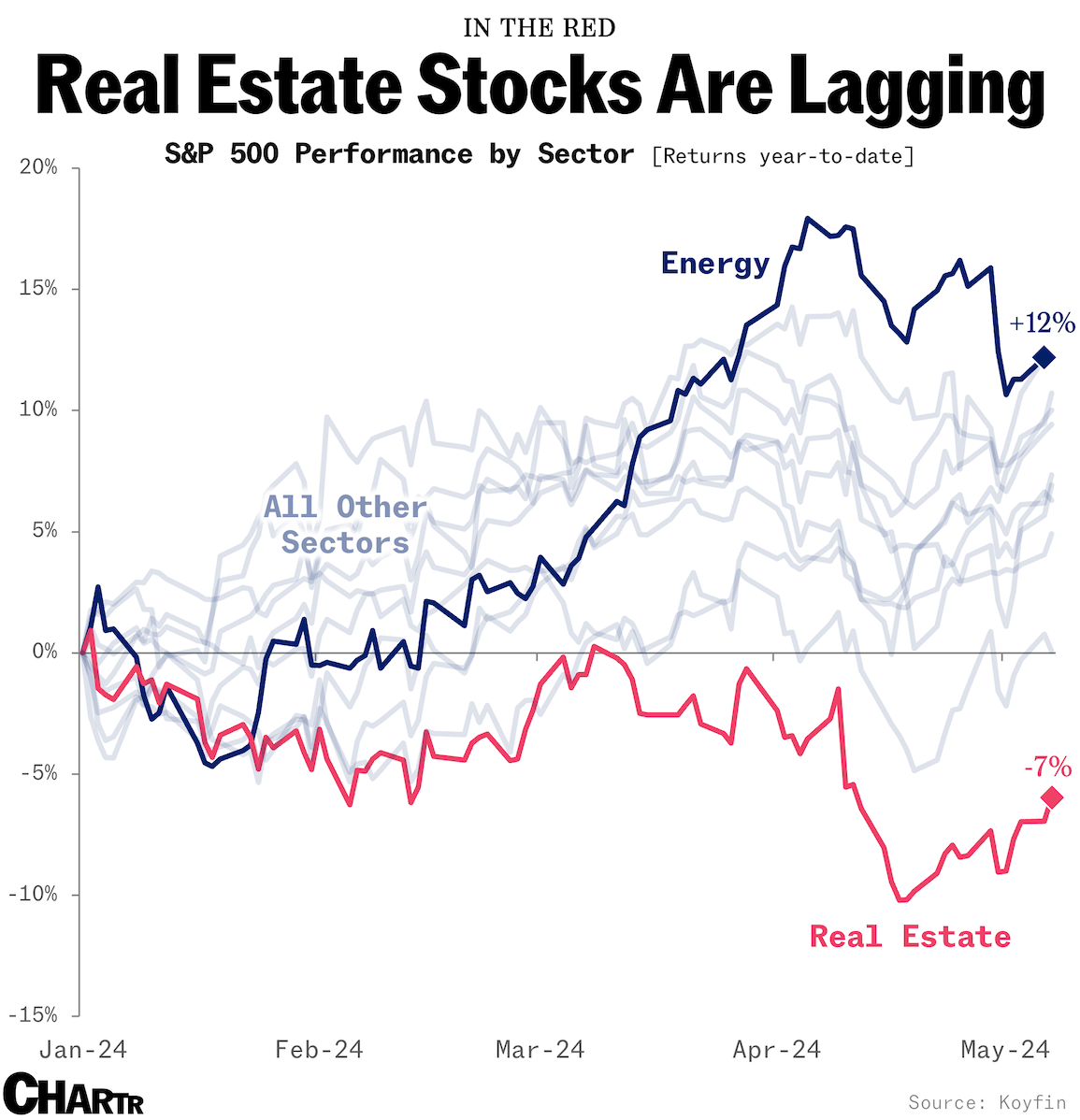

While the broader S&P 500 has soared to record highs this year, up some 9% at the latest count, one sector has remained in the red for most of 2024: real estate.

Indeed, the XLRE, an ETF designed to track the real estate segment of the S&P 500, is down 7% in 2024. That makes it the worst performing of any S&P 500 sector — an undesirable title which it also holds over 3-year, 5-year, and 10-year lookback periods.

So, what’s going on with real estate?

Some analysts would argue that it’s all about rates. Real estate has historically been a comfortable, safe place to park your money and earn a yield from rent-producing assets like offices, retail space, or residential properties. When rates rise — as they have done over the last 24 months — other opportunities to invest and earn a good return crop up, making real estate look less attractive.

That is certainly part of the puzzle. Another is arguably more structural: in the post-pandemic world, we might simply have too much office and retail space, which many REITs (Real Estate Investment Trusts) and real estate stocks own a lot of… usually with borrowed money.

Indeed, as of the first quarter, office vacancy rates have hit a 40-year high, just shy of 20%, according to Moody’s Analytics. As demand stagnates and leases come up for renewal, commercial real estate is being sold at significant discounts, with some buildings that have been empty for years selling for pennies on the dollar in New York, San Francisco, St. Louis, and elsewhere.

The flip side: The one part of real estate that’s booming? Demand for space for AI data centers, which jumped 26% last year.