The remarkable rise of the Honeycrisp and Cosmic Crisp apples

When it comes to apples, America cannot get enough of the crunch factor.

America is a land of diversity where people, cultures, and inspirations clash to create a melting pot of different ideas. But ask a room full of people what their favorite apple is and these days you might get a lot of the same answer: Honeycrisp.

The apple of our eyes

Unfortunately, as reported by The Wall Street Journal earlier this week, farming them is something of a nightmare. Honeycrisps are easily bruised, often grow too densely for their own good, have to be hand-clipped from trees due to their thin skin, and can be afflicted by diseases that blotch the fruit. They are, as one farmer put it, a “diva.”

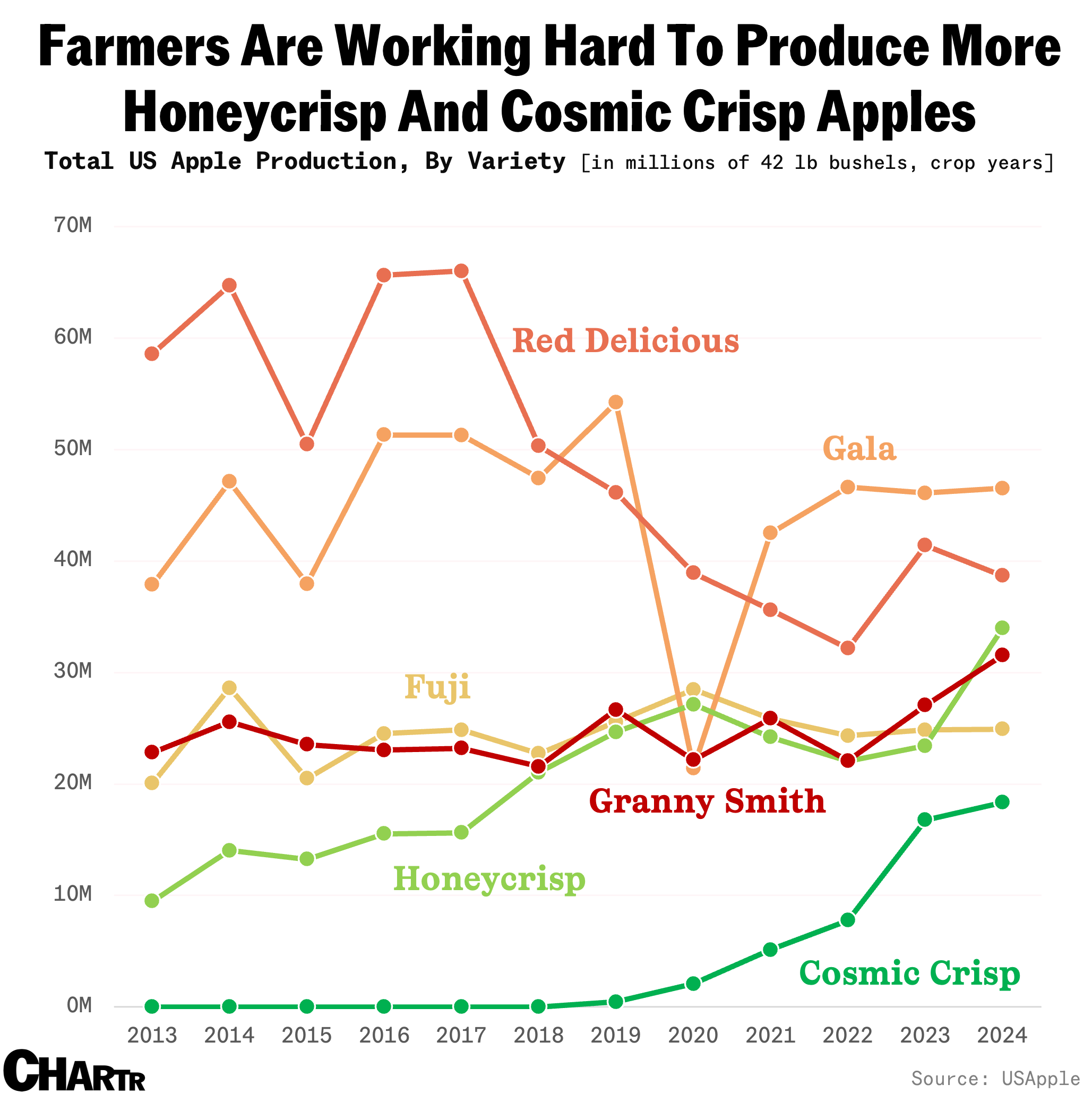

They’re also valuable, however, dubbed “moneycrisps” by some. And, along with the Cosmic Crisp and Pink Lady, they’re soaring up the apple production league tables toward icons like Gala and Red Delicious, which have seen production drop over time.

Per data from USApple, the core of the apple-eating market is increasingly the three varieties that make a mouth-watering crunch — Cosmic Crisp, Pink Lady, and Honeycrisp — production volumes of which have jumped 3,391%, 63%, and 17% in the last five years, respectively.

Remarkably, a study published all the way back in 2013 essentially predicted this boom, finding that when consumers assessed apples based on their appearance, they looked for size and color. When evaluating taste they wanted sweetness and crispness. And they’re willing to pay: per retail price data tracked by USApple, Honeycrisp was the most expensive apple in 2023-24, at $1.88, compared to Gala at $1.49 and Red Delicious apples at $1.26.

But, with production expenses for fruit farms rising across the board, up 49% over the last decade, even producers of the “moneycrisp” have been feeling the pressure in the industry’s bottom line — and the new, crunchier, and crispier varieties also tend to have more volatile prices.