Retailers’ profits will get clobbered by more than 30% by tariffs, says Morgan Stanley

Analysts at Morgan Stanley crunched the numbers and it turns out tariffs are really, really bad for US retailers.

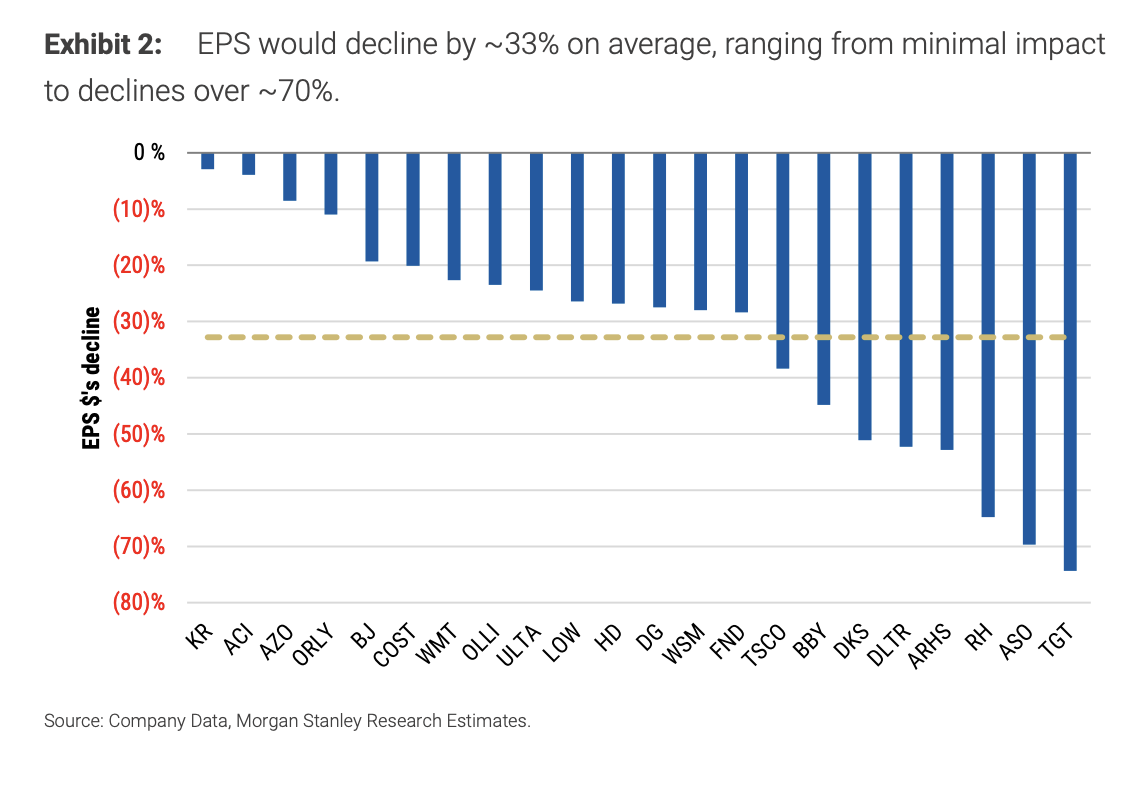

Acknowledging that “a wide range of outcomes is possible,” the analysts found that recently enacted tariffs would increase prices by 1% and decrease volumes by 3%. This assumes a 145% tariff on China and a 10% tariff on everyone else besides Canada and Mexico.

On average, earnings per share would decline by 33%, with some companies more exposed than others, the analysts wrote.

Among the most exposed companies are Target, Academy, and Restoration Hardware. (If you don’t believe them, I’d point you to the Restoration Hardware CEO’s reaction on an earnings call when seeing the impact of President Trump’s April 2 tariff announcement had on his stock in real time.) The least exposed are grocery stores like Kroger and Albertsons.